Waiting for a conventional 30-day close is the most effective way to lose a high-yield investment property in the current market. Strategic investors recognize that liquidity is a tool for speed, not just a safety net. Understanding exactly how do bridge loans work allows you to decouple the timing of an acquisition from the sale of an existing asset. This ensures you never miss a deal because your capital is tied up in equity.

You likely realize that traditional bank timelines don’t align with the pace of value-add real estate. This guide provides the technical breakdown you need to master bridge financing and secure properties quickly. We will detail the mechanics of interest-only structures and the transition to long-term leverage through products like DSCR loans. You will also find the latest data on 2026 interest rates, which currently range from 8% to 14.5% based on SOFR benchmarks. We also cover the impact of the March 2026 FinCEN reporting rules for entity-based purchases and how the 6.75% Prime Rate influences your cost of capital. This overview clarifies your exit strategy and helps you scale your portfolio with confidence.

Key Takeaways

- Understand the fundamental mechanics of how do bridge loans work to facilitate immediate property acquisitions before securing long-term debt.

- Learn how to utilize LTV and LTC ratios to maximize your leverage and deploy capital effectively across new projects.

- Evaluate the strategic trade-off between higher short-term interest rates and the profit potential of securing time-sensitive deals.

- Identify the critical steps for structuring a loan, including defining a clear exit strategy through sale or DSCR refinancing.

- Explore how specialized financing for $2 million+ loan amounts can help you scale your real estate portfolio without traditional bank delays.

What is a Bridge Loan and Why do Investors Use Them?

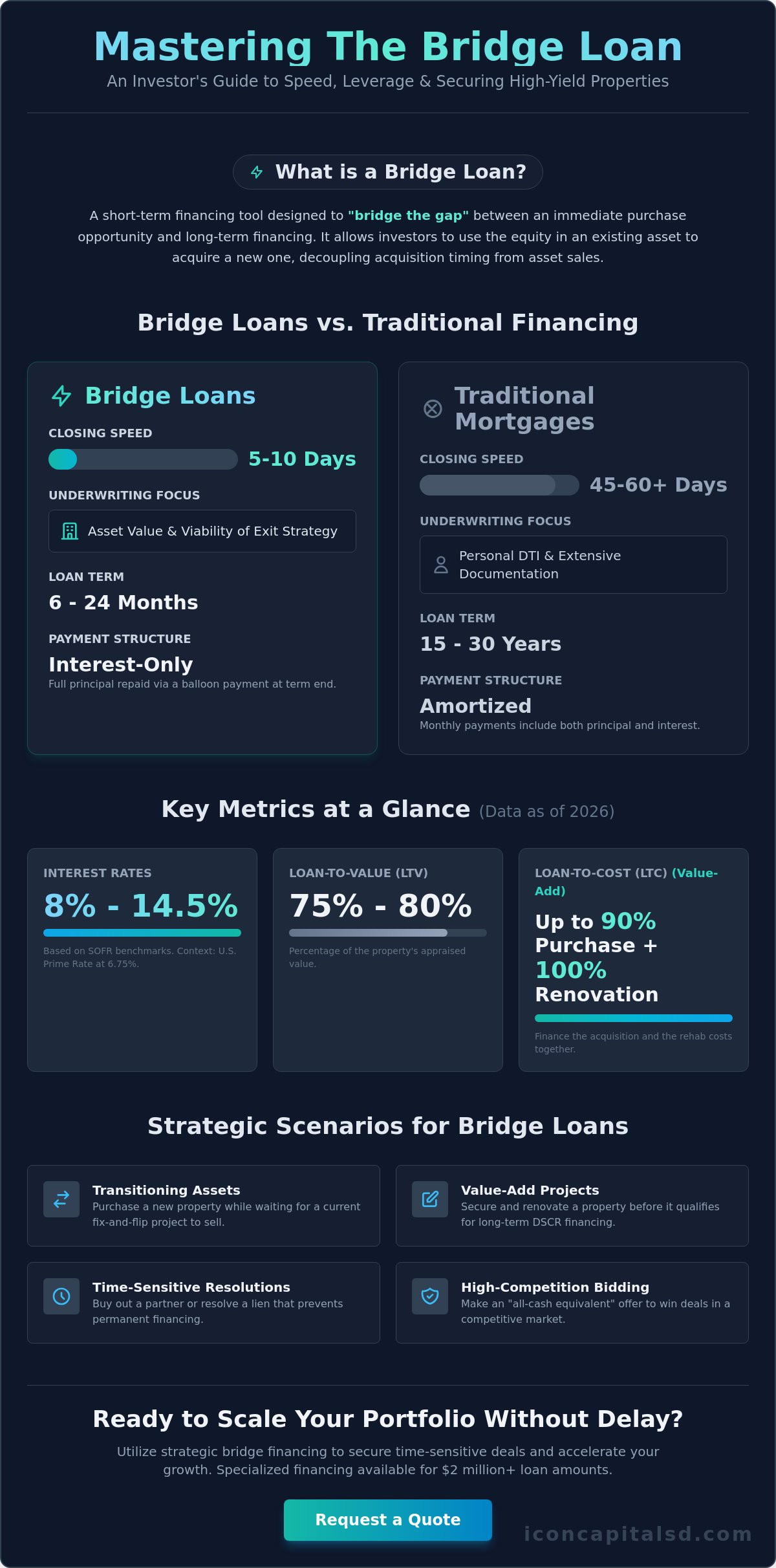

A bridge loan is a specialized short-term financing tool designed to provide immediate capital by leveraging the equity of an existing asset to fund a new acquisition. In the professional real estate sector, these instruments are often referred to as swing loans, gap financing, or interim debt. To understand how do bridge loans work, you must view them as a financial connector. They bridge the temporal gap between an immediate purchase opportunity and the eventual realization of long-term liquidity, whether that comes from a property sale or a permanent refinance.

According to the industry definition of What is a Bridge Loan, these products are transactional in nature. In May 2026, sophisticated investors prioritize speed of execution over the lowest possible interest rate. With the U.S. Prime Rate holding at 6.75%, bridge loan rates typically range from 8% to 14.5%. While this is higher than conventional debt, the ability to close a deal in days rather than months is often the difference between scaling a portfolio and missing a high-yield opportunity.

Bridge Loans vs. Traditional Mortgages

The primary distinction between bridge financing and traditional mortgages lies in the underwriting focus. Conventional lenders prioritize personal debt-to-income (DTI) ratios and extensive documentation, a process that can take 45 to 60 days. Bridge lenders focus almost exclusively on the asset value and the viability of the exit strategy. This allows for funding in as little as 5 to 10 business days. To truly grasp how do bridge loans work in a competitive environment, you must look at the approval speed. While traditional loans are structured for 15 to 30 years, bridge loans are designed for agility. Terms typically span 6 to 24 months, providing enough runway to execute a value-add strategy without locking the investor into long-term obligations. For investors who also need assistance with personal home purchases or state-specific programs, visit Jeremy Drobeck – Treadstone Mortgage to explore traditional residential loan options.

Common Investment Scenarios

Investors utilize bridge debt to solve specific liquidity constraints that traditional banks often avoid. Common applications include:

- Transitioning Assets: Purchasing a new investment property while waiting for a current fix-and-flip project to close.

- Value-Add Projects: Securing a multi-unit building that requires immediate, heavy renovation before it qualifies for a DSCR loan.

- Time-Sensitive Resolutions: Buying out a partner or resolving a lien that must be cleared before permanent financing can be secured.

- High-Competition Bidding: Making an all-cash equivalent offer to win a deal in a tight market.

If you have a deal that requires rapid funding, you can request a quote to see how we structure these interim solutions for your specific portfolio needs.

The Mechanics: How Bridge Loans Function in Real Estate Deals

Understanding the structural framework is essential for any professional investor. While residential guides often explain how bridge loans work for homebuyers, the investment application is far more data-driven. It relies on the interplay between Loan-to-Value (LTV) and Loan-to-Cost (LTC) ratios. Lenders typically cap LTV at 75% to 80% of the property’s appraised value. For value-add projects, LTC becomes the primary metric. This allows investors to finance up to 90% of the purchase price and 100% of the renovation costs.

To understand how do bridge loans work in practice, you must account for the lien position. Most bridge financing requires a first lien position, ensuring the lender has primary claim to the asset. Funds are often disbursed in staged draws for renovations. This ensures capital is deployed as value is added to the property. This process prevents the investor from paying interest on the full renovation budget from day one. Instead, you pay interest only on the funds that have been disbursed.

Interest-Only Payments and Balloon Terms

Amortization schedules don’t apply to bridge debt. Most loans require interest-only monthly payments. This structure preserves liquidity during the construction or transition phase. As of May 2026, with the U.S. Prime Rate at 6.75%, these payments remain manageable for high-margin deals. The full principal is repaid via a balloon payment at the end of the 12 to 24-month term. This repayment usually coincides with a property sale or a transition to long-term DSCR financing. Managing this timeline is the most critical aspect of the deal.

Cross-Collateralization Strategies

Professional investors often use cross-collateralization to scale quickly. This involves securing one loan with multiple properties. If a single asset doesn’t provide enough equity for a new acquisition, you can leverage other assets in your portfolio to close the gap. This strategy can significantly increase your maximum loan amount. However, it requires a precise risk management plan. If one asset underperforms, the lender has recourse against the entire collateral pool. Balancing this risk is a key part of how do bridge loans work for aggressive portfolio growth. You can examine your leverage options to see how cross-collateralization fits your current assets.

Bridge Loans vs. Traditional Financing: A Strategic Analysis

A bridge loan is often defined by its cost, but for the professional investor, the true metric is the opportunity cost of a missed deal. Traditional financing offers lower interest rates, yet the 45 day underwriting cycle is a liability in high competition markets. Understanding how do bridge loans work in comparison to standard mortgages reveals a fundamental shift in focus. Traditional lenders prioritize borrower paperwork and historical tax returns. Bridge lenders prioritize asset liquidity and the speed of the transaction.

These instruments are frequently categorized as hard money or private money. This classification exists because the capital comes from private sources rather than federal bank deposits. This detachment from institutional bureaucracy allows for the flexibility required by self employed borrowers and business owners. When analyzing how do bridge loans work for non-traditional borrowers, the advantage is clear. You don’t need to provide two years of W-2s to secure a $2 million acquisition. The equity in your portfolio and the viability of your exit strategy serve as the primary qualifications.

Choosing a bridge loan over a Home Equity Line of Credit (HELOC) or a personal loan is a matter of scale and timing. A HELOC can take 30 to 60 days to fund, which is too slow for a time sensitive purchase. Personal loans rarely offer the capital depth needed for commercial or high value residential assets. Bridge financing fills this gap by providing high leverage debt that functions like cash in the eyes of a seller.

Speed as a Competitive Advantage

In the May 2026 real estate market, certainty of execution is a premium. While traditional buyers are stuck in a 45 day cycle, bridge financing allows you to close in 7 to 14 days. This speed creates a “cash-like” offer that often wins bidding wars even when competing against higher bids with financing contingencies. This rapid deployment is essential for Fix and Flip Loans where the acquisition must happen before a competitor can secure traditional funding.

Cost Structure and Fee Transparency

The cost of bridge capital is higher than long term debt, but it is a temporary expense. As of May 2026, investors can expect origination fees ranging from 1.5% to 2.5% of the total loan amount. Processing and underwriting fees typically fall between $500 and $1,500, with appraisal costs ranging from $300 to $600. While the interest rates of 8% to 14.5% are higher than a 30 year mortgage, they are only paid for the duration of the “bridge” period. Once the asset is stabilized or the previous property is sold, the investor transitions to lower cost, long term leverage.

Qualifying and Structuring Your Bridge Loan for Maximum Leverage

Qualification for bridge financing moves at the speed of the market. Unlike traditional banks that scrutinize personal income, bridge lenders prioritize the asset’s potential and the borrower’s track record. Understanding how do bridge loans work during the underwriting phase requires a shift from personal creditworthiness to deal structure. The process follows a methodical five-step sequence designed to minimize risk and maximize speed.

First, you must define a concrete exit strategy. Lenders won’t fund a bridge loan without a clear path to repayment. Second, evaluate the equity position across your current portfolio. High-leverage deals often require cross-collateralization to reach the desired loan amount. Third, gather property-level documentation. This includes current rent rolls and recent appraisals, which typically cost between $300 and $600 as of May 2026. Fourth, align with a lender specializing in Non-QM structures to avoid the delays of institutional banks. Finally, finalize your “takeout” financing plan before the bridge term expires.

The Critical Role of the Exit Strategy

Lenders care more about the exit than the entry. A bridge loan is a temporary phase. If your goal is to hold the property, the most common transition is moving into a DSCR loan. This allows you to pay off the bridge principal once the asset is stabilized and generating income. If you plan to sell, you must prove marketability. Lenders look for a Realistic Sales Price (RSP) that covers the balloon payment. Effective March 1, 2026, FinCEN requires a “Real Estate Report” for all-cash purchases by legal entities or trusts. Your exit strategy must account for these transparency regulations to ensure a seamless transition.

Non-Traditional Qualification Standards

Self-employed investors and business owners often lack the W-2 documentation required by retail banks. Non-QM bridge products solve this by using P&L statements or bank statements to verify cash flow. This asset-based qualification allows high-net-worth investors to secure capital based on their liquid reserves rather than taxable income. This flexibility extends to Foreign Nationals who may not have a U.S. credit history but possess significant equity in domestic assets. By focusing on the numbers rather than the narrative, investors can structure how do bridge loans work to fit their specific financial profile. If you’re ready to move forward, you can submit your loan scenario for a professional review of your leverage options.

Scaling Your Portfolio with Icon Capital’s Bridge Financing

Icon Capital specializes in high-leverage interim debt for complex real estate scenarios. We focus on loan amounts exceeding $2 million. Our role as a direct Non-QM specialist allows us to bypass the rigid constraints of traditional depository institutions, which are currently limited by the $59 million HMDA asset-size exemption threshold for 2026. When you analyze how do bridge loans work through our platform, you see a focus on technical efficiency. We simplify the transaction into a streamlined four-step process:

- Structure Loan: We define the LTV, LTC, and the specific exit strategy.

- Submit Loan: You provide the property-level data and borrower profile.

- Underwrite Loan: Our experts evaluate the asset and the transition plan.

- Close Loan: Capital is deployed in as little as 7 to 14 days.

This methodical approach ensures that your capital is deployed exactly when the deal requires it. By focusing on the mechanics of the deal rather than long-form narratives, we enable investors to scale their portfolios with speed and certainty.

Creative Solutions for Complex Deals

Consider a multi-unit transition. An investor needs to acquire a $5 million apartment complex that requires immediate stabilization before qualifying for long-term debt. A traditional bank might decline the loan due to current occupancy levels. Icon Capital structures a bridge solution based on the property value and a clear 18-month exit strategy. We handle the complexities of self-employed and business owner borrower profiles that institutional lenders often reject. If your scenario involves unique collateral or non-traditional income, you can Request a Quote to see our specific terms.

Next Steps: Securing Your Interim Capital

Preparation is the key to a fast close. Before your consultation, ensure you have your property-level data ready. This includes the purchase contract, current rent rolls, and a detailed budget for any planned renovations. We leverage our expertise in Fix & Flip and Construction to ensure your bridge loan is structured for maximum leverage. Whether you are managing the March 1, 2026 FinCEN reporting rules for entity-based purchases or reacting to the March 13, 2026 executive orders on housing credit, we provide the technical support needed for a successful close.

Understanding how do bridge loans work is the first step toward aggressive portfolio scaling. The next step is execution. Our team is ready to review your $2 million+ loan scenarios and provide the creative financing solutions necessary to bridge the gap. Please give us a call or shoot an email to explore your options today.

Leveraging Interim Capital for Portfolio Growth

Mastering the mechanics of how do bridge loans work transforms a temporary liquidity gap into a strategic advantage. You now understand that these high-leverage tools prioritize asset value and exit viability over traditional debt-to-income ratios. By securing financing in as little as 7 to 14 days, you position yourself to capture opportunities that conventional lenders cannot fund. Whether you are transitioning to a DSCR loan or executing a value-add renovation, the focus remains on a clear path to long-term stabilization. In the 2026 market, where the Prime Rate sits at 6.75%, speed is the ultimate currency for the professional investor.

Icon Capital provides the creative financing expertise required for complex, $2 million+ acquisitions. We specialize in Non-QM structures that support self-employed investors and Foreign Nationals who require agile capital solutions. Our team focuses on the technical aspects of your deal to ensure a seamless close. Don’t let slow institutional processes stall your growth. Request a Bridge Loan Quote from Icon Capital to secure your next asset with confidence. We are ready to help you scale your portfolio today.

Frequently Asked Questions

How much equity do I need for a bridge loan in 2026?

You typically need 20% to 25% equity in the collateral asset. Lenders generally cap the Loan-to-Value (LTV) ratio at 75% to 80% for purchase transactions. If you use an existing property as collateral, the available equity must be sufficient to cover the down payment and closing costs of the new acquisition without exceeding these leverage limits.

Can I get a bridge loan if I am self-employed?

Yes, bridge loans are specifically designed for self-employed borrowers and business owners who don’t meet traditional W-2 requirements. Qualification focuses on the asset’s value and your exit strategy rather than historical tax returns. Lenders often use bank statements or P&L statements to verify your ability to manage the interest-only payments during the loan term.

What is the typical interest rate for an investment bridge loan?

As of May 2026, interest rates range from 8% to 14.5%. These rates are influenced by the U.S. Prime Rate of 6.75% and the Secured Overnight Financing Rate (SOFR). Your specific rate depends on factors like property type, LTV, and your experience level. Understanding how do bridge loans work helps you realize that while rates are higher than 30-year debt, the short-term nature limits the total interest expense.

What happens if my property doesn’t sell before the bridge loan is due?

You must either refinance the debt or negotiate an extension with the lender. If a sale is delayed, many investors transition the bridge loan into a long-term DSCR loan to stabilize the asset. Failure to repay the balloon payment by the maturity date can result in default; therefore, having a secondary exit strategy is a critical part of deal structuring.

Is a bridge loan the same as a hard money loan?

Bridge loans and hard money loans are both forms of short-term, asset-based financing, but they serve different functions. Hard money is often used for distressed properties or rapid fix-and-flip projects. Bridge loans are typically used to bridge a timing gap between two transactions or to stabilize an asset before securing permanent financing. Both fall under the Non-QM and private money umbrella.

Can I use a bridge loan for a multi-family or commercial property?

Yes, bridge financing is a standard tool for multi-family and commercial acquisitions. It allows investors to secure properties that may not yet meet the occupancy or debt-service coverage requirements of traditional commercial lenders. This provides the necessary capital to renovate or lease up the property before moving to a permanent agency or CMBS loan.

How fast can a bridge loan be funded?

Funding typically occurs within 7 to 14 business days. This is significantly faster than the 45-day cycle required for traditional mortgages. The speed is possible because the underwriting focuses on the collateral and the exit plan rather than an exhaustive review of the borrower’s personal financial history. This rapid deployment is a key factor in how do bridge loans work for competitive bidding.

Do bridge loans require a full appraisal?

Most lenders require a full appraisal to verify the current market value of the collateral. In 2026, appraisal fees for investment properties typically range from $300 to $600. Some private lenders may accept an interior or exterior Broker Price Opinion for smaller deals, but high-leverage or $2 million+ loans almost always necessitate a formal valuation to manage risk.