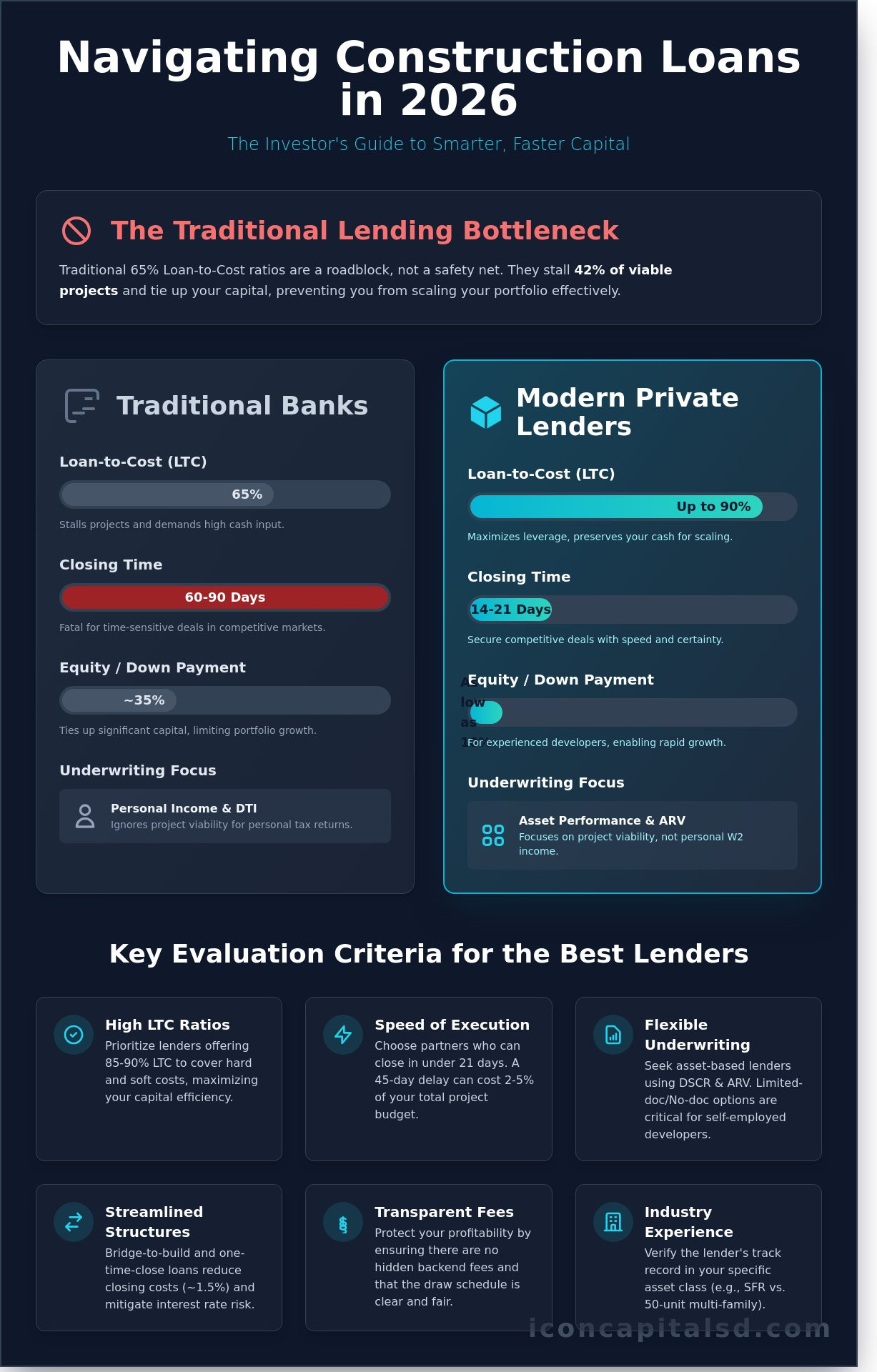

A 65% Loan-to-Cost ratio isn’t a safety net; it’s a bottleneck that stalls 42% of viable development projects before the first permit is pulled. For active investors, capital efficiency determines your ability to scale. Finding the best construction loan lenders in 2026 requires looking beyond traditional banks that demand three years of tax returns and 35% equity down. You need a partner who understands that project viability and future ARV are more important than a self-employed developer’s personal adjusted gross income.

You’ve likely felt the frustration of a 15 day delay in a draw request that causes your framing crew to move to a different job site. We understand that speed and leverage are the lifeblood of your portfolio. This guide shows you how to secure up to 90% LTC and 100% of construction costs through lenders who utilize streamlined, tech-driven inspection processes. We’ll analyze the top-tier financing options that prioritize asset performance and flexible qualification, ensuring your 2026 projects stay on schedule and under budget.

Key Takeaways

- Identify the critical differences between consumer construction-to-perm loans and investor bridge-to-build financing in the current 2026 market.

- Evaluate the best construction loan lenders based on Loan-to-Cost (LTC) ratios and the transparency of their draw schedules.

- Leverage Non-QM and asset-based lending solutions to secure capital when traditional credit requirements create barriers to entry.

- Protect your project’s profitability by recognizing hidden backend fees and preventing communication breakdowns between lenders and builders.

- Access creative financing structures and direct underwriting to accelerate the closing process for complex real estate investment deals.

The 2026 Construction Loan Landscape for Investors

The 2026 construction financing market is defined by a shift toward private credit and specialized lending. Interest rates for investor-focused construction products have stabilized between 6.75% and 8.5%, depending on leverage and experience. Finding the best construction loan lenders today requires looking beyond the interest rate. Modern developers prioritize capital providers who offer bridge-to-build structures. This model allows an investor to acquire land and transition immediately into a construction draw schedule without a second closing.

Private capital has largely replaced traditional institutional lending for mid-market residential and commercial projects. While banks have tightened liquidity, private funds focus on the asset’s projected value and the developer’s track record. Speed of execution has become the most critical metric. A 45-day delay in funding can increase carrying costs by 2% to 5% of the total project budget. Efficient developers now seek lenders capable of closing in under 21 days to secure sites in competitive markets.

Construction-to-Permanent vs. Standalone Construction

One-time close loans, or construction-to-perm products, are gaining traction because they reduce closing costs by approximately 1.5% of the loan amount. These loans mitigate interest rate risk by locking in the permanent mortgage rate before the first shovel hits the dirt. This is vital in 2026 as market volatility continues to affect long-term yields. Standalone construction loans remain the preferred choice for short-term flips or “build-to-sell” strategies. These interest-only products typically have 12 to 24-month terms. For a technical overview of the construction process and how it impacts draw schedules, investors should consult industry standards to align their financing with physical milestones.

Why Traditional Banks Often Fail Real Estate Investors

Traditional banks operate on a rigid framework that doesn’t account for the realities of professional real estate investment. They rely heavily on debt-to-income (DTI) ratios and personal tax returns. This creates a “red tape” barrier for self-employed developers or those with complex portfolios. A typical big bank takes 60 to 90 days to move from application to funding. This timeline is often fatal for time-sensitive deals. The best construction loan lenders avoid these hurdles by using project-based underwriting. They prioritize the Debt Service Coverage Ratio (DSCR) and Loan-to-Cost (LTC) metrics over personal W2 income. If you need a faster solution, you can request a quote to see how private structures outperform traditional bank requirements.

- Bank Closing Time: 60 to 90 days

- Private Lender Closing Time: 14 to 21 days

- Typical LTC: Up to 85% for experienced developers

- Documentation: Limited doc or No-doc options available through private channels

Evaluation Criteria for Ranking the Best Construction Loan Lenders

Selecting a lending partner requires a forensic look at the capital stack and operational efficiency. The best construction loan lenders distinguish themselves through high Loan-to-Cost (LTC) ratios rather than strictly relying on Loan-to-Value (LTV). While LTV focuses on the projected after-repair value, LTC covers the actual hard and soft build costs. This distinction is critical for maintaining liquidity throughout the project lifecycle. A lender’s ability to finance soft costs, such as architectural fees, engineering reports, and municipal permits, often determines whether a project achieves its target internal rate of return. Investors must also verify a lender’s track record in specific asset classes. A lender specializing in single-family residential may lack the internal infrastructure to manage the complex draw schedules and compliance requirements of a 50-unit multi-family development.

Leverage and Capital Requirements

Experienced developers with 5 completed projects in the last 36 months typically qualify for 85-90% LTC. This high leverage allows for portfolio scaling without exhausting cash reserves. For those with fewer than 2 completed builds, down payment requirements usually jump from 10% to 30% of the total cost. Understanding how construction loans work involves analyzing interest reserves. Lenders often bake 12 to 24 months of interest into the loan amount. This ensures the developer doesn’t face monthly debt service obligations while the asset is non-income producing. For a precise breakdown of available leverage for your next project, you can request a quote to see current market rates and terms.

Speed of Funding and Draw Reliability

The anatomy of a draw is the most frequent point of failure in construction financing. The process starts with a site inspection, moves to budget line-item verification, and ends with fund disbursement. A 48-hour turnaround for draw requests is the industry benchmark for excellence. When a lender takes 7 to 10 business days to release funds, it creates a bottleneck that leads to sub-contractor attrition and project delays. Vetting a lender involves identifying red flags in their draw process during the initial due diligence phase. Beware of lenders who require excessive notarized lien waivers for minor draws or those who don’t utilize digital inspection platforms to accelerate verification. Consistent, predictable capital flow is the only way to keep a job site active and on schedule in a competitive 2026 market.

Specialized Financing: When Traditional Credit Isn’t Enough

Standard bank underwriting often falls short for complex development projects. Traditional lenders prioritize W-2 income and strict debt-to-income ratios, which excludes many successful real estate investors. Non-QM (Non-Qualified Mortgage) solutions provide the flexibility required for ground-up construction or major renovations. The best construction loan lenders in 2026 focus on asset-based lending rather than personal tax returns. This approach evaluates the project’s projected value and the borrower’s liquidity instead of just a credit score.

Asset-based underwriting differs from traditional methods by prioritizing the Loan-to-Cost (LTC) and Loan-to-Value (LTV) ratios. Lenders look at the “As-Completed Value” (ACV) to determine risk. Investors with a strong portfolio can leverage existing equity to secure better terms, often reaching 80% to 85% LTC. This enables developers to scale without depleting their cash reserves. Creative financing structures also allow for interest-only periods during the build phase, which preserves cash flow for the developer.

Using Bank Statement and P&L Loans for Construction

Self-employed developers often show significant deductions on tax returns. This lowers their qualifying income for traditional banks. We solve this by using 12 to 24 months of bank statements to verify actual cash flow. Alternatively, a Guide to P&L Home Loans explains how a business-prepared Profit and Loss statement can serve as the primary qualification document. This method focuses on the actual health of the development firm. It provides a clearer picture of repayment ability than outdated tax filings from two years ago.

Foreign National Construction Financing Options

The US real estate market remains a primary target for international capital. Foreign national investors often lack a US credit score, which makes traditional financing impossible. Specialized programs now allow non-citizens to build in the States using international credit reports or asset verification. This Foreign National Loan Guide details how investors can access up to $5 million in construction capital. Requirements typically include a 30% to 40% down payment and 12 months of reserves held in a US bank account.

Creative financing is no longer a niche alternative; it’s a necessity for high-volume investors. To see how these structures apply to your next project, you can request a quote from our team today. The best construction loan lenders are those who understand that every deal requires a custom structure to maximize ROI.

Avoiding Common Pitfalls with Construction Lenders

Selecting the best construction loan lenders requires looking beyond the initial interest rate. Many investors fall for “cheap” capital that carries heavy backend exit fees or administrative surcharges exceeding 1.5% of the total loan volume. These hidden costs erode project margins before the first shovel hits the ground. Teaser rates frequently mask restrictive draw contingencies. If a lender requires 100% completion of a specific phase before releasing any funds, you’ll need significant cash reserves to bridge the gap.

Soft costs are another common trap. In 2026, architectural fees, permits, and environmental impact studies can account for 18% of a total project budget. If your lender only finances hard costs, you’ll face a capital shortfall early in the cycle. Poor communication between the lender and your builder is a primary project killer. A 48 hour delay in responding to a budget modification can stall a site for a week, leading to missed milestones and potential default triggers.

The High Cost of Inefficient Draw Processes

Time is your most expensive line item. On a $2 million construction loan at a 9% rate, the daily carry cost is approximately $493. A 14 day delay in a draw inspection costs you $6,902 in pure interest. Beyond the interest, draw delays cause contractor attrition. Skilled trade professionals in 2026 won’t wait 15 days for payment; they’ll move to a competing job site. Ask these specific questions to vet a lender’s inspection network:

- Does the lender use a local inspection network or a national third party service?

- What is the average turnaround time from draw request to cash in hand?

- Is there a dedicated draw administrator assigned to the file?

Vetting Builder Approval Requirements

The best construction loan lenders vet your general contractor (GC) as thoroughly as they vet your credit. They view the GC as the primary guarantor of the collateral’s completion. Your builder must provide a resume showing at least 5 completed projects of similar scope, 2 years of corporate tax returns, and active liability insurance. This documentation ensures the builder has the capacity to manage the 2026 labor market and material supply chains.

If you’re a developer acting as your own builder, expect stricter terms. Lenders typically require a 20% liquidity reserve or the involvement of a third party fund control company to manage disbursements. This adds a layer of oversight but ensures the project stays solvent through completion. Efficient lenders use this vetting process to mitigate risk for both the bank and the investor.

To secure a term sheet that fits your specific project timeline and mitigates these common risks, request a quote for your construction project today.

Securing Your Capital with Icon Capital LLC

Icon Capital LLC provides the liquidity required for complex real estate developments. We specialize in creative financing for investors who don’t meet the rigid criteria of traditional banks. Our team understands that speed and high leverage are critical for maintaining project momentum. By offering direct access to decision-makers, we eliminate the delays common in institutional lending environments. This direct model allows us to structure deals based on the specific merits of the project rather than generic credit boxes. We position ourselves as one of the best construction loan lenders for those requiring non-QM solutions and flexible underwriting.

Our Creative Financing Suite for Developers

We bridge the gap between initial acquisition and the final certificate of occupancy. Our programs combine the agility of short-term financing with the long-term capacity needed for ground-up construction. This is particularly effective for 5-8 unit residential projects where traditional retail lenders often struggle with valuation. We focus on the asset’s potential and the developer’s track record. Our lending parameters often reach up to 85% LTC (Loan-to-Cost), providing the leverage necessary to scale your portfolio without depleting all liquid reserves. We handle the complexities of multi-unit builds by focusing on the project’s projected DSCR and exit strategy.

The Application to Groundbreaking Process

Icon Capital uses a streamlined 4-step process to move your project from a concept to a funded reality. We prioritize transparency, ensuring you know exactly where your file stands at every stage. Our internal underwriting team works directly with you to clear hurdles quickly.

- Structure Loan: We review your project’s scope, budget, and exit strategy to determine the optimal leverage and rate.

- Submit Loan: You provide the necessary documentation, including construction budgets, site plans, and permits.

- Underwrite: Our internal team performs a deep dive into the deal’s fundamentals to verify feasibility and project timelines.

- Close and Fund: We finalize the legal components and release the initial draw so site work can begin.

To receive an initial quote within 24 to 48 hours, have your executive summary, detailed pro-forma, and schedule of real estate owned (SREO) ready. Providing clear documentation of your soft costs and hard costs allows our underwriters to issue a term sheet with precision. We value efficiency and expect our partners to maintain the same level of professional readiness. This collaborative approach is why investors rank us among the best construction loan lenders in the private sector. If you’re ready to secure funding for your next project, request a construction loan quote to speak with our specialists.

Our goal is to be a solution-oriented partner for your most ambitious builds. We don’t just provide capital; we provide a structured path to completion. Whether you’re breaking ground on a single-family luxury build or a mid-sized multi-family complex, Icon Capital has the expertise to close your deal.

Scale Your Portfolio With Precision in 2026

Navigating the 2026 construction landscape requires more than just a high credit score. Successful investors must prioritize liquidity management and avoid common pitfalls like restrictive bank covenants or delayed funding cycles. Identifying the best construction loan lenders means finding a partner that understands the specific demands of Non-QM products and mid-range developments. Efficiency is the standard for 2026; a delay in capital is a direct hit to your ROI.

Icon Capital LLC bridges the gap where traditional institutions fail. We specialize in creative financing for 5-8 unit builds, providing the leverage needed for complex residential and commercial projects. Our team delivers a potential 48-hour draw turnaround to keep your job site active and your schedule on track. You don’t have to settle for rigid terms that stifle your growth. Take the next step toward securing your project’s capital with a team that values speed and technical expertise.

Request a Creative Construction Loan Quote from Icon Capital today to lock in your financing strategy. Let’s get your next build funded and moving.

Frequently Asked Questions

What is the typical down payment for a construction loan in 2026?

Most construction loan lenders require a 20% to 25% down payment in 2026. This equity stake secures the lender’s position during the ground-up phase of your project. If you already own the land, its current appraised value can often count toward this 25% requirement. High-leverage programs might allow 15% for experienced developers who’ve completed 5 or more projects in the last 3 years.

Can I get a construction loan if I am self-employed?

You can secure a construction loan as a self-employed investor by utilizing Non-QM products like bank statement programs. Instead of traditional tax returns, underwriters analyze 12 to 24 months of business bank deposits to verify your cash flow. This approach allows business owners to qualify based on their actual gross revenue rather than net income after tax deductions. It’s an efficient solution for investors with complex tax profiles.

How long does it take to get approved by construction loan lenders?

Approval timelines for construction loans typically range from 30 to 45 days. This period includes the standard credit underwriting process plus a detailed review of the builder’s credentials and the project’s line-item budget. The best construction loan lenders streamline this by performing the credit and project approvals simultaneously to meet tight closing deadlines. Having your site plans and permits ready before application can reduce this timeline by 10 days.

What is the difference between a construction-only loan and construction-to-perm?

A construction-only loan is a short-term facility, usually 12 to 18 months, that requires a separate refinance once the build is finished. Construction-to-perm loans simplify the process by automatically converting the balance into a 30-year mortgage once the certificate of occupancy is issued. This single-close option reduces total closing costs by approximately 2% of the loan amount. It’s a pragmatic choice for investors looking to hold the asset long-term.

Do construction lenders allow for “owner-builder” projects?

Most lenders require a third-party licensed General Contractor and don’t allow owner-builder projects unless the borrower holds a current GC license. Risk mitigation policies in 2026 demand professional oversight to ensure projects finish on time and within budget. If you lack a license, you’ll need to hire a builder with at least 5 years of documented experience. This ensures the project meets the structural standards required by the underwriter.

What credit score is needed for the best construction loan rates?

You need a minimum credit score of 720 to access the best construction loan lenders and their most competitive interest rates. While some programs accept scores as low as 660, these typically come with a 1% to 2% rate premium and higher down payment requirements. Maintaining a high score ensures lower origination fees and higher LTV limits for your project. Lenders look for a clean 24-month payment history on all active credit lines.

Are there construction loans available for foreign national investors?

Foreign national investors can access construction financing through specialized Non-QM programs that don’t require a U.S. credit history. Lenders typically cap the LTV at 65% for these borrowers and require a 12-month interest reserve in a U.S. bank account. Documentation focuses on international assets and a valid passport or visa to satisfy KYC requirements. This enables global investors to scale their real estate portfolios within the U.S. market efficiently.

How do interest-only payments work during the construction phase?

Interest-only payments during construction apply only to the funds that have been disbursed to the builder through the draw schedule. If your total loan is $1 million but you’ve only drawn $200,000 for the foundation, you only pay interest on that $200,000. This structure preserves your cash flow until the project is fully funded and moves to the permanent phase. It’s a standard feature designed to keep carrying costs low during the development cycle.