Your pro forma accounts for every nail and permit, but it likely ignores the 25% drain on your mental capacity caused by unexpected project delays. Real estate investing is a numbers game, but the emotional cost of flipping a house can bankrupt your productivity long before the final inspection. You already know that market shifts and contractor friction are part of the business. It’s a high-pressure environment where decision fatigue is as real as a failed foundation. With 76% of builders reporting material shortages in recent years, the logistical hurdles alone are enough to compromise your focus.

This guide provides a pragmatic framework to protect your psychological ROI. We’ll show you how to implement professional systems that automate complex choices and use reliable financing to eliminate the anxiety of carrying costs. You’ll learn to treat your mental bandwidth like any other asset. We’ll cover how to structure your Fix & Flip loans to maintain liquidity and reduce the burden of financial uncertainty. By the end, you’ll have the strategies needed to scale your portfolio with the same efficiency you use to calculate your LTV.

Key Takeaways

- Contrast media myths with the reality of carrying costs to navigate the renovation’s “trough of sorrow” effectively.

- Recognize signs of decision fatigue and the sunk cost trap to maintain objective, profitable renovation standards.

- Mitigate the emotional cost of flipping a house by implementing professional systems that shift management from hands-on to eyes-on.

- Utilize a comprehensive Scope of Work (SOW) to act as a psychological contract, reducing friction and daily decision-making stress.

- De-risk your investment by partnering with reliable lenders who provide a vital sanity check and a transparent closing process.

HGTV vs. Reality: The Hidden Psychological Toll of Flipping

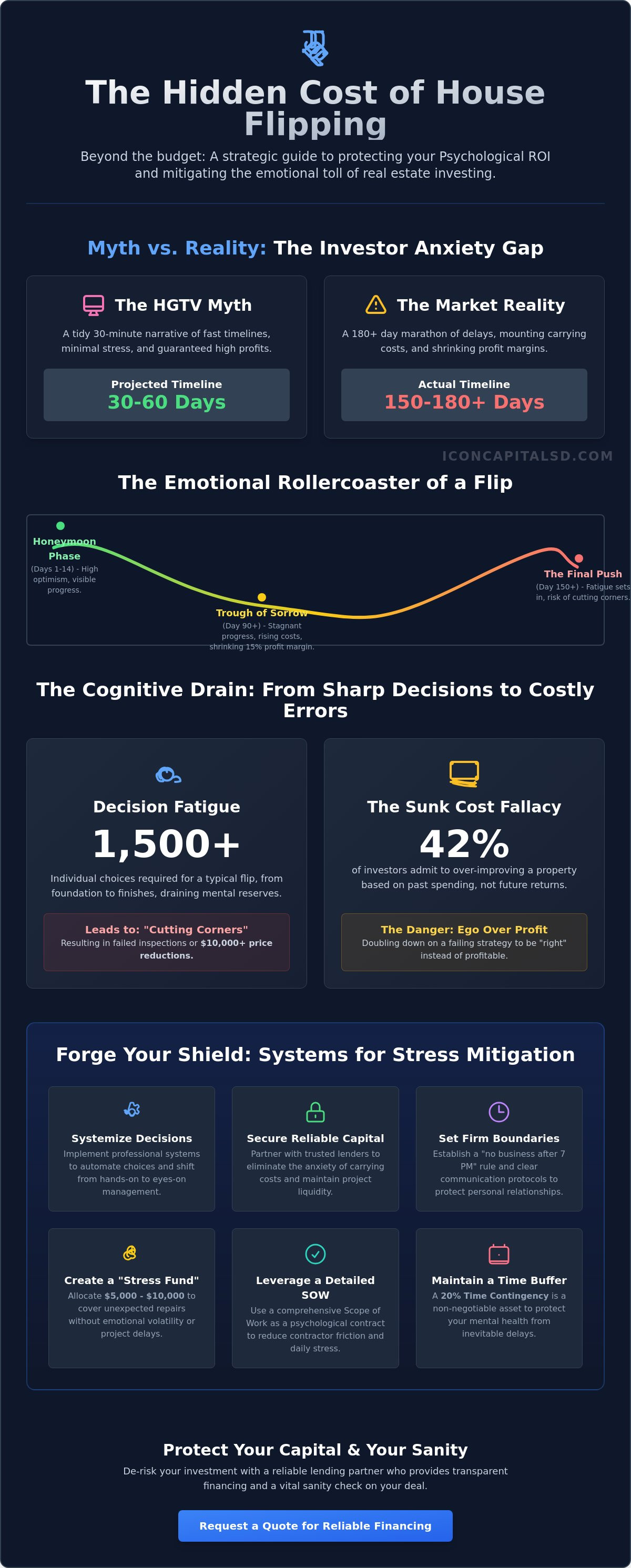

Television programs condense a 180-day renovation into a 30-minute narrative. This creates a dangerous misconception of the emotional cost of flipping a house. Most investors experience a predictable “honeymoon phase” during the first 14 days of demolition when progress is visible and rapid. However, by day 90, many hit a “trough of sorrow.” This period is characterized by stagnant progress, mounting carrying costs, and the realization that the projected 15% profit margin is shrinking. Successful investors treat emotional resilience as a core metric. They prioritize “Psychological ROI,” which measures the mental energy expended against the final financial gain. If a project yields $50,000 but causes six months of chronic sleep deprivation and high cortisol levels, the investment may be a net loss in terms of total lifestyle impact.

The Gap Between Expectation and Execution

Unrealistic timelines are the primary drivers of early-stage burnout. While an investor might project a 90-day turnaround, municipal permit backlogs or supply chain disruptions often push the completion date to 150 days or more. The Realities of House Flipping involve managing high-stakes risks that television often glosses over. Discovering $12,000 in hidden foundation damage or extensive mold behind a bathroom wall can trigger immediate psychological distress. We define the investor anxiety gap as the space between projected and actual timelines. When this gap exceeds 30 days, decision-making quality typically declines. Investors must maintain a 20% time contingency to protect their mental health from these inevitable discoveries.

The Social Cost: Partners, Family, and Contractors

The financial pressure of a fix and flip rarely stays on the job site; it bleeds into personal relationships. When a project is over budget, the stress impacts household dynamics and long-term partnerships. Managing the emotional cost of flipping a house requires navigating the often adversarial psychology of contractor management. General contractors and investors frequently have misaligned incentives, leading to friction over quality and deadlines. To mitigate this, professional investors establish rigid emotional boundaries before the first hammer swing. This includes:

- Implementing a “no-business” window after 7:00 PM to preserve family stability.

- Setting clear, written communication protocols with all sub-contractors to reduce daily friction.

- Allocating a specific “stress fund” of $5,000 to $10,000 to cover unexpected repairs without emotional volatility.

Pragmatic investors recognize that financing is a tool to reduce this burden. To stabilize your project’s capital structure and reduce liquidity-related stress, you can request a quote for professional financing solutions tailored to your specific asset. This allows you to focus on execution rather than capital shortfalls.

Decision Fatigue and the Sunk Cost Trap

Successful real estate investing requires high-level cognitive function, yet the sheer volume of choices in a renovation often leads to decision fatigue. This psychological state occurs when the quality of an investor’s choices deteriorates after a long sequence of decision-making. A typical fix-and-flip project requires over 1,500 individual choices, ranging from structural engineering specs to the specific sheen of cabinet hardware. By the time a project reaches the 60-day mark, mental reserves are often depleted. This exhaustion significantly increases the emotional cost of flipping a house, frequently leading to “cutting corners” that result in failed inspections or $10,000 price reductions during the closing process.

Ego frequently exacerbates these issues. When a deal goes south due to unforeseen foundation issues or a shifting market, an investor’s refusal to pivot often stems from a desire to be “right” rather than profitable. Instead of selling the asset at a small loss or restructuring the financing to hold the property as a rental, investors may double down on a failing strategy. This stubbornness is a primary driver of financial insolvency in the residential redevelopment sector.

Recognizing the Sunk Cost Fallacy

The Sunk Cost Fallacy occurs when you justify additional spending based on past investments rather than future returns. In a 2023 industry survey, 42% of residential investors admitted to over-improving a property because they felt they had already “invested too much to quit.” You must distinguish between a necessary repair, which is required for safety or code compliance, and an emotional attachment based on personal preference. The Rule: If a specific feature does not offer a documented 120% return on cost based on current local comps, delete it from the budget immediately.

Combating Decision Fatigue in Renovations

Pragmatic investors eliminate daily choices by using standardized finish schedules. Selecting tile colors or light fixtures at 4 PM on a Friday is a high-risk activity; cognitive drain makes you more likely to pick expensive or mismatched items just to end the workday. Utilizing professional design templates preserves your mental energy for high-stakes tasks like negotiating with contractors or reviewing closing disclosures. Standardizing your materials across your entire portfolio reduces the emotional cost of flipping a house by removing the friction of the unknown.

- Create a “Master Specs” sheet for all projects to eliminate 90% of design choices.

- Limit contractor meetings to Tuesday mornings when cognitive clarity is at its peak.

- Use pre-vetted color palettes (e.g., Sherwin Williams “Agreeable Gray”) to avoid the stress of custom matching.

How Financial Uncertainty Compounds Emotional Stress

Financial uncertainty is the primary driver of investor burnout. The emotional cost of flipping a house is directly tied to the “burn rate,” which is the daily cost of holding a property. High-interest carrying costs, property taxes, and insurance premiums create a ticking clock that never stops. For an investor with a $400,000 loan at a 10% interest rate, every day costs roughly $110 in interest alone. This constant financial leak makes delays in permitting or contractor scheduling feel like personal attacks on your net worth.

Anxiety often spikes during the renovation phase when “capital gaps” emerge. These are the moments when the initial budget fails to cover discovered defects, such as faulty wiring or foundation cracks. If an investor hasn’t budgeted a 15% contingency fund, these gaps force difficult decisions. You’re often left choosing between cutting corners or injecting more personal capital, both of which degrade mental clarity and project confidence.

Hard money debt is fundamentally different from a traditional 30-year mortgage. It is transactional and time-sensitive. The pressure stems from the short-term nature of the balloon payment. While a traditional mortgage allows for decades of market fluctuation, hard money demands a result within 6 to 12 months. This performance-based debt creates a high-stakes environment where every week of inactivity feels like a step toward financial ruin.

The final emotional hurdle is the appraisal gap. After months of labor, a low appraisal can destroy the projected profit. This fear often leads to “over-improving” a property in a desperate attempt to guarantee a high valuation, which ironically reduces the actual ROI. The emotional cost of flipping a house is highest when you realize your hard work may not translate into the expected equity.

The Link Between Liquidity and Mental Clarity

Cash reserves function as the most effective anti-anxiety tool for real estate professionals. Maintaining liquid capital ensures that a $5,000 plumbing emergency remains a tactical problem rather than a financial catastrophe. While some avoid the cost, flipping houses with hard money offers the agility to capitalize on opportunities that traditional banks reject. This speed reduces the total time an investor is exposed to market risk and high-stress environments. Investors operating on thin margins, such as those with less than 10% equity, experience significantly higher stress levels because they lack a buffer for error.

Market Volatility and the “Exit Strategy” Panic

A 180-day project window is long enough for macro-economic shifts to occur. If buyer demand drops while the house is mid-renovation, panic often sets in. Successful investors counter this by preparing a secondary exit. Transitioning to a DSCR loan allows the investor to hold the asset as a rental if the sales market softens. This flexibility removes the “must-sell” requirement and stabilizes the investor’s psychological state. Data-driven analysis of local absorption rates provides the clarity needed to stay the course when headlines turn negative, ensuring decisions are based on equity rather than fear.

Systems for Stress Mitigation: Treating Flipping Like a Business

Successful investors reduce the emotional cost of flipping a house by transitioning from hands-on labor to eyes-on management. Daily friction occurs when an investor tries to manage every hammer swing or paint stroke personally. Business-minded flippers use professional project management software to offload mental tracking and centralize communication. This shift allows for objective oversight rather than reactive panic. Implementing a 20% buffer time in every project schedule accounts for supply chain disruptions or labor shortages. This isn’t a suggestion; it’s a structural requirement for maintaining psychological ROI. When the schedule accounts for the unknown, a three-day delay becomes a planned variable instead of a crisis. It keeps the project moving without the mental fatigue of constant rescheduling.

The Power of Professional Documentation

Clarity eliminates conflict. Detailed types of loans for flipping houses documentation forces an investor to analyze the capital stack and interest carry before a single wall is demolished. A precise Scope of Work (SOW) functions as a psychological contract between the investor and the contractor. It defines expectations and sets boundaries that prevent “scope creep.” To mitigate financial anxiety, treat a 15% contingency fund as a non-negotiable line item. This capital isn’t a safety net but a pre-allocated resource for the inevitable surprises found behind drywall. Having this liquidity ready prevents the paralysis that occurs when unexpected costs arise during the demolition phase.

Automating the Investor Mindset

Decisions shouldn’t be made under duress. Establish “if/then” triggers to handle project delays automatically. For example, if a contractor misses a milestone by more than 48 hours, then a formal site meeting is triggered. If the renovation budget exceeds the 15% contingency, then the finish spec is adjusted to maintain the margin. This removes the emotional burden of deciding when to intervene. Delegating low-value decisions, such as selecting hardware or standard paint codes, allows the investor to focus on high-value strategy and portfolio scaling. A mentor or a professional partner provides the objective perspective needed to see past the immediate stress of a deal. They help maintain focus on the LTV and the eventual exit strategy rather than the temporary chaos of the job site.

De-Risking Your Flip with Reliable Capital

The emotional cost of flipping a house often peaks during the funding phase. Investors frequently prioritize the lowest interest rate while ignoring the reliability of the source. Cheap money from an inexperienced private lender often becomes the most expensive capital when draws are delayed or the closing process stalls. Professional lending partners provide a necessary sanity check for your investment strategy. A professional underwriter’s approval validates your project’s viability, confirming that your ARV and renovation budget align with current market data.

Speed is a psychological asset in real estate. A transparent, 10-day closing process eliminates the uncertainty that leads to investor burnout. When you know the capital is secured, you can focus on contractor management and project timelines rather than chasing wire transfers. This shift from “funding anxiety” to operational execution defines the difference between a hobbyist and a professional investor.

If market conditions shift, having a versatile lender allows you to pivot. You can transition a stressful flip into a stable rental using DSCR financing. This strategy allows you to recoup your initial capital while maintaining a 1.20 or higher debt service coverage ratio. It turns a potential short-term loss into a long-term wealth-building asset.

The Value of Capital Certainty

Fix and Flip loans from Icon Capital provide predictable draws that keep your job site moving. Novice investors often face 15% to 20% budget overruns due to interest carry when funding is inconsistent. Reliable capital removes this friction. Our team focuses on the mechanics of the deal, ensuring that your LTV and liquidity requirements meet the demands of the project. This systematic approach reduces the emotional cost of flipping a house by replacing guesswork with institutional-grade underwriting standards.

- Predictable draw schedules based on completed work phases.

- Clear communication on holdback requirements.

- Validation of exit strategies including sale or refinance.

Your Next Step: Securing Your Foundation

Moving from emotional chaos to systematic investment requires a partner who understands the Fix & Flip lifecycle. You need a lender that values efficiency and technical accuracy over narrative. By securing a foundation of professional capital, you scale your portfolio without the psychological weight of unreliable funding. We provide the leverage you need to close quickly and move to your next acquisition with confidence. Our process is designed for busy professionals who require quick access to critical data and fast approvals.

CTA: Ready to de-risk your next project? Request a Quote from Icon Capital

Mastering the Mechanics of Scalable Investing

Success in real estate investment requires more than just construction knowledge; it demands mental resilience. Managing the emotional cost of flipping a house starts with replacing uncertainty with repeatable systems. Industry data shows that professional investors who utilize structured capital often reduce project timelines by 15% compared to those relying on traditional bank approvals. Decision fatigue often stems from capital bottlenecks, which you can avoid by securing reliable funding partners before the first hammer falls. Moving from a reactive mindset to a proactive one is the hallmark of a professional operator.

Icon Capital provides the financial infrastructure needed to move from stress to scale. We offer specialized Fix & Flip and DSCR programs designed for non-traditional borrowers who require creative financing solutions that traditional lenders often overlook. Our direct, professional underwriting process ensures capital certainty, allowing you to focus on project management rather than liquidity crises. By treating financing as a core business system, you protect your psychological ROI and your bottom line. We handle the mechanics of the deal so you can focus on the next acquisition.

Secure your next deal with Icon Capital’s Fix & Flip financing

Build your portfolio with confidence.

Frequently Asked Questions

Is house flipping as stressful as it looks on TV?

House flipping is often more stressful than reality TV suggests because the financial stakes are higher and timelines are longer. While TV shows resolve issues in 42 minutes, real investors face 3 to 6 months of holding costs and unexpected permit delays. According to a 2023 ATTOM report, gross flipping profits dropped to a 15 year low. These tighter margins increase the emotional cost of flipping a house for most investors.

What is the biggest emotional mistake new house flippers make?

The biggest emotional mistake is developing a personal attachment to the property instead of treating it as a financial asset. New investors often spend 15% more on high end finishes that don’t increase the appraisal value. This emotional bias leads to over-capitalization. You must prioritize the LTV and ROI over your personal aesthetic preferences to maintain a professional distance from the project.

How do I know if I should quit a house flip that’s going wrong?

You should consider exiting a flip when the cost to complete exceeds the projected After Repair Value (ARV) by a margin that eliminates your 10% contingency fund. If structural issues increase your renovation budget by 20% or more, the deal is likely compromised. Professional investors use a stop loss strategy to sell the property mid renovation to another investor. This prevents further capital erosion and psychological burnout.

Can I flip a house while working a full-time job without burning out?

Flipping a house while working 40 hours a week is possible if you outsource the project management to a licensed General Contractor. Investors who attempt to DIY renovations while working full time often face a 50% increase in project duration. Burnout occurs when you exceed 60 total work hours per week for more than 3 consecutive months. Success requires a reliable team to handle daily site visits and inspections.

How does the type of financing I choose affect my stress levels?

Short term hard money loans increase stress because of high interest rates and 6 to 12 month maturity dates. If a project stalls, the daily interest drain creates significant pressure. Choosing creative financing options with 18 month terms provides a 6 month safety net. This buffer reduces the emotional cost of flipping a house by removing the immediate threat of default during minor construction delays.

What are the signs of ‘decision fatigue’ in real estate investing?

Decision fatigue manifests as an inability to choose between simple options or making impulsive, high cost purchases to end a discussion. A typical fix and flip requires over 150 individual decisions ranging from paint colors to plumbing fixtures. When investors reach this limit, they often ignore 5% cost variances that eventually destroy their profit margins. Standardizing your spec book for every project reduces this cognitive load.

How can I protect my personal relationships during a difficult flip?

Protect your relationships by establishing strict no work zones and times, such as after 7:00 PM or during Sunday mornings. Data from relationship studies suggests that financial stress is a top cause of conflict in 35% of partnerships. Clear communication about the 10% contingency budget ensures your partner understands the financial risks. Keeping business discussions separate from personal time prevents the flip from dominating your home life.

Does having a backup plan like a DSCR loan help reduce flipping anxiety?

A DSCR loan serves as a critical Plan B that allows you to pivot from a flip to a long term rental if the market shifts. Knowing you can refinance into a 30 year fixed loan based on the property’s cash flow rather than your personal income provides immense security. This exit strategy ensures you aren’t forced to sell at a loss if the local market inventory increases by 20% during your renovation period.