As a business owner, your tax returns reflect strategic deductions, not your actual purchasing power. Without traditional W-2s, you face a significant hurdle with lenders who often fail to see your true financial strength. This common scenario makes securing a self employed mortgage a uniquely challenging process, frequently leading to overwhelming paperwork and frustrating rejections from conventional institutions.

This guide provides a direct solution. We cut through the complexity to deliver a clear, actionable framework for approval. You will learn precisely how to leverage alternative documentation-like bank statements or 1099s-to qualify based on your real cash flow, not just your adjusted gross income. We will outline the exact documents required, introduce specialized loan options designed for entrepreneurs, and equip you to submit an application structured to succeed. Consider this your definitive roadmap to financing, connecting your business success to your real estate goals.

Key Takeaways

- Understand why traditional underwriting standards often conflict with self-employed income verification and how to navigate the “tax return dilemma.”

- Discover how Non-Qualified Mortgages (Non-QM) offer a direct path to approval using alternative documentation like bank statements instead of W-2s.

- Follow a clear, actionable checklist to prepare your documentation and streamline the application process for a self employed mortgage.

- Overcome common objections and gain confidence by learning the facts behind the most persistent myths surrounding loans for entrepreneurs.

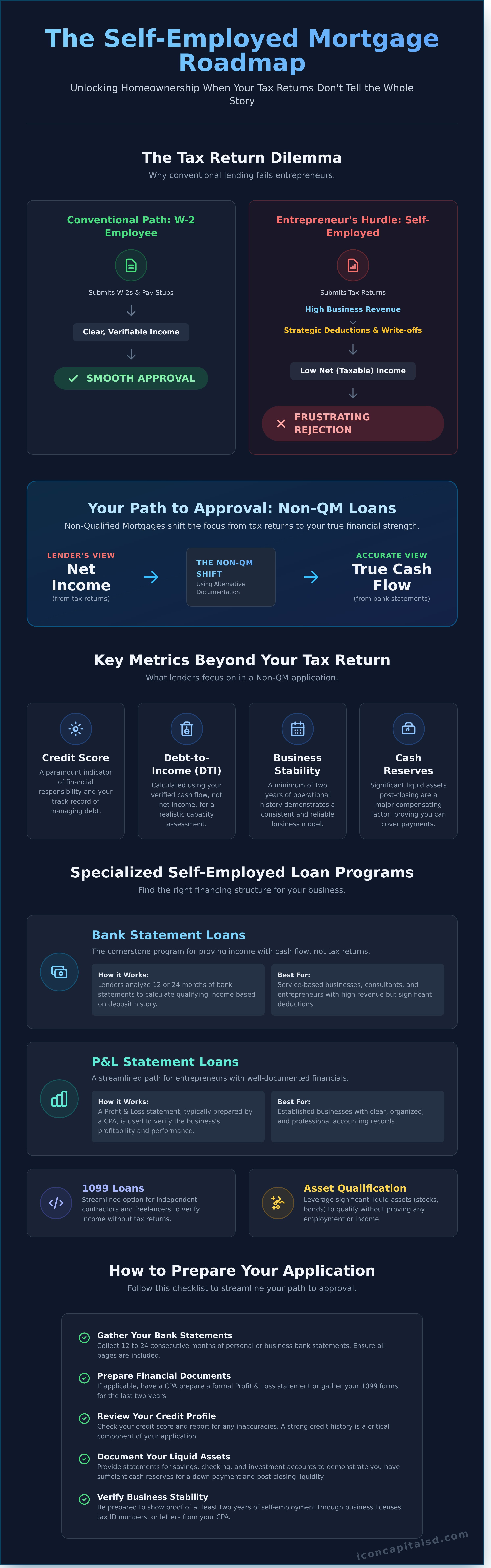

Why Getting a Mortgage Is Different When You’re Self-Employed

For business owners, the path to securing a mortgage is fundamentally different from that of a W-2 employee. Traditional lenders rely on tax returns and pay stubs to verify income-a system that often fails to represent the true financial strength of a successful enterprise. This creates the “Tax Return Dilemma”: savvy entrepreneurs use legitimate deductions to lower their taxable income, but this same practice can disqualify them from a conventional loan. Lenders need to see stable, consistent income, and for a business owner, this requires looking beyond the tax return’s bottom line.

The Underwriter’s View: Net Income vs. True Cash Flow

Conventional lenders focus almost exclusively on your net income-the profit shown on your tax returns after all business expenses and write-offs have been deducted. This focus on net income is a standard part of the underwriting process, but it penalizes successful business owners who are maximizing their deductions. An underwriter sees a low qualifying income, even if the business generates substantial revenue. True cash flow, which is the actual capital moving through your business bank accounts, provides a far more accurate assessment of your ability to service debt. This is the metric that matters in a modern self employed mortgage program.

Key Metrics Beyond Your Tax Return

When tax returns do not provide a complete financial picture, lenders specializing in loans for the self-employed pivot to other key indicators of financial health:

- Credit Score: A strong credit history is paramount. It serves as a primary indicator of financial responsibility and your track record of managing debt, carrying significant weight in Non-QM loan approvals.

- Debt-to-Income (DTI) Ratio: Instead of using your reduced net income, lenders calculate DTI using your verified cash flow from bank statements. This provides a more realistic picture of your capacity to take on a new mortgage payment.

- Business Stability: Lenders typically require a minimum of two years of operational history. This demonstrates a consistent and reliable business model, reducing perceived risk.

- Cash Reserves: Having significant liquid assets post-closing is a major compensating factor. These reserves show you can cover mortgage payments and unexpected expenses, strengthening your overall borrower profile.

Your Path to Approval: Non-QM Loans for Entrepreneurs

For entrepreneurs, the rigid requirements of a traditional Qualified Mortgage (QM) often create a significant barrier to homeownership. These loans demand tax returns and W-2s-documents that rarely reflect the true financial strength of a growing business. This is where Non-Qualified Mortgages (Non-QM) provide a direct path forward. Non-QM loans are specifically designed for borrowers with non-traditional income streams, using flexible and alternative methods to verify financial capacity. While the process can seem complex, understanding How to Get a Mortgage When You’re Self-Employed starts with knowing these alternative solutions exist.

At Icon Capital LLC, we focus exclusively on these creative financing structures, providing the essential self employed mortgage options that traditional lenders cannot.

Bank Statement Loans: Proving Income with Cash Flow

This is the cornerstone program for many business owners. Instead of tax returns, lenders analyze 12 or 24 months of personal or business bank statements to assess your actual cash flow. Income is calculated by totaling deposits and applying a standard expense factor to determine a qualifying figure. This approach is ideal for service-based businesses, consultants, and entrepreneurs with high revenue but significant business deductions that lower their taxable income.

P&L Statement Loans: For Established Business Owners

For entrepreneurs with well-documented financials, a Profit & Loss (P&L) statement loan offers another streamlined path. This option requires a P&L, typically prepared by a CPA, to verify the business’s profitability. Because it doesn’t rely on tax returns, it allows business owners to qualify based on their company’s actual performance. It is best suited for established businesses with clear and organized accounting records.

Other Specialized Self-Employed Loan Programs

Beyond bank statements and P&Ls, several other programs cater to specific entrepreneurial scenarios. These alternative solutions include:

- 1099 Loans: A streamlined option for independent contractors and freelancers who receive 1099 forms instead of W-2s, allowing for income verification without tax returns.

- Asset Qualification Loans: This program allows borrowers to leverage significant liquid assets (like stocks, bonds, or savings) to qualify for a mortgage without proving any employment or income.

Unsure which loan structure is right for your financial situation? Request a personalized quote to discuss your specific scenario with a specialist.

How to Prepare Your Self-Employed Mortgage Application: A Checklist

A successful self employed mortgage application hinges on preparation. Unlike W-2 employees, business owners must present a comprehensive financial picture that accurately reflects their true income and business stability. Following a structured approach minimizes delays and positions your application for approval. Begin by ensuring your business and personal finances are clearly separated to create the clear financial trail lenders need to see.

Step 1: Strengthen Your Financial Profile

Lenders evaluate your financial health to assess risk. Before applying, take proactive steps to present the strongest possible profile. This demonstrates financial discipline and increases your qualification potential.

- Review Your Credit Report: Obtain reports from all three major bureaus. Dispute any errors immediately, as this process can take time.

- Lower Your DTI Ratio: Pay down high-interest consumer debt, such as credit cards and personal loans. A lower debt-to-income (DTI) ratio is critical for mortgage qualification.

- Maintain Financial Stability: In the months leading up to your application, avoid taking on new debt, making large or undocumented cash deposits, or changing your business’s financial structure.

Securing a large asset like a home often prompts a broader review of your financial safety net. At this stage, many entrepreneurs also look into life insurance to protect their families from the new mortgage debt. Resources like LifeInsure.com offer a straightforward way to get instant quotes as part of this planning process.

Step 2: Organize Your Documentation

Having all necessary documents ready is the most effective way to accelerate the underwriting process. This is where organization prevents costly delays.

- For Bank Statement Loans: Gather 12 to 24 months of complete, consecutive business bank statements. Ensure all pages are included.

- For P&L Loans: Work with your CPA or a licensed tax preparer to create a recent, signed Profit & Loss statement and balance sheet.

- General Business Documents: Have your business license, articles of incorporation or organization, and personal identification readily available.

Step 3: Partner with a Non-QM Specialist

Conventional lenders often struggle to underwrite loans for business owners. A Non-QM specialist understands the nuances of alternative documentation and has access to loan programs designed specifically for entrepreneurs. They know how to structure a loan to highlight your strengths, navigate complex income streams, and secure the highest probability of approval. An expert can save you significant time and prevent unnecessary denials.

Take the first step with a lender who specializes in your success. Request a free quote from Icon Capital to explore your financing options.

Common Myths and Questions About Self-Employed Mortgages

Navigating the mortgage landscape can be complex for entrepreneurs. Misconceptions surrounding bank statement loans and other Non-QM products often prevent qualified business owners from securing financing. This section provides direct, expert answers to common questions, clarifying the realities of these flexible lending solutions.

Are Interest Rates and Down Payments Higher?

While interest rates for bank statement loans may be slightly higher than conventional mortgages, they remain highly competitive. The final rate is determined by factors like credit score, loan-to-value (LTV) ratio, and cash reserves. For a borrower with a strong financial profile, the difference is often minimal and represents a fair trade-off for the flexible income verification.

Down payment requirements typically range from 10% to 25%. This flexibility allows business owners to preserve liquidity while still accessing home financing, a crucial advantage over traditional loans that may demand different terms after scrutinizing tax returns.

Can I Get a Mortgage with Less Than 2 Years of Self-Employment?

The two-year self-employment history is a standard guideline, not a rigid rule in the Non-QM space. Lenders can often structure a self employed mortgage for business owners with as little as 12 months of verifiable income history. Approval with a shorter history depends on strong compensating factors, such as:

- Excellent credit scores (typically 700+)

- Significant liquid assets or post-closing reserves

- Demonstrable experience in the same field prior to starting the business

How Do Lenders Treat Business Debt?

Underwriters analyze business-related debts on a personal credit report to determine their impact on your debt-to-income (DTI) ratio. A common concern is that these debts will disqualify a borrower, but this is often not the case.

If a debt is paid directly from a business account and not from personal funds, it can frequently be excluded from your personal DTI calculation. To document this, you will typically need to provide 12 consecutive months of business bank statements showing the payments were made by the business entity. This is a key advantage of working with a lender experienced in creative financing solutions.

These Non-QM solutions are specifically engineered to address the unique financial structures of business owners. By looking beyond tax returns, they provide a clear path to homeownership that aligns with your true financial capacity. To get a clear assessment of your qualifications, explore your options with our loan specialists.

Your Path to Mortgage Approval as an Entrepreneur

Navigating the mortgage process as a business owner requires a different strategy than for a W-2 employee. While traditional lenders focus heavily on tax returns, this often fails to capture the full financial picture of a successful enterprise. The solution lies in understanding the alternative pathways available, particularly Non-QM loans that utilize documents like bank statements for qualification. The key to securing a self employed mortgage is meticulous preparation and partnering with a lender who understands your unique financial landscape. As we’ve covered, debunking common myths and assembling a comprehensive application package are the foundational steps toward achieving your goal.

At Icon Capital, we specialize in this exact area. We provide the creative financing solutions and Non-QM products that empower business owners. Our team understands the complexities of entrepreneurial income and is structured to deliver a fast, direct, and professional process from start to finish. We bypass the typical hurdles of conventional lending to focus on what matters: your capacity to invest. Ready to explore your options and see what you qualify for? Request a quote from an Icon Capital specialist today.

Your homeownership and investment goals are attainable.

Frequently Asked Questions

What is the minimum credit score needed for a self-employed mortgage?

Minimum credit score requirements for a self-employed mortgage vary by program. For most Non-QM bank statement loans, lenders require a FICO score of 660 or higher. However, certain programs can accommodate scores as low as 600. A stronger credit profile typically results in a more favorable loan-to-value (LTV) ratio and better interest rates. The score is a critical component of the overall qualification profile, evaluated alongside business cash flow and liquid assets.

Do I have to use a special lender or can my local bank help me?

You will need to work with a specialized lender. Traditional banks and credit unions must adhere to strict agency guidelines that require tax returns to verify income. Bank statement loans are a Non-QM (Non-Qualified Mortgage) product, meaning they fall outside these conventional rules. Lenders who offer these solutions have the specific underwriting expertise to analyze income based on business cash flow, a capability most local banks do not possess.

How do lenders verify my business is legitimate?

Lenders use several standard methods to verify your business is active and established. This process typically requires documentation such as a copy of your business license, articles of incorporation, or a letter from a licensed CPA or tax preparer. Underwriters may also perform a simple online search to confirm your company’s digital presence and operational history. This due diligence ensures the business has been operating for the required period, which is usually a minimum of two years.

This process of verification is a standard part of any major financial transaction. Just as lenders perform due diligence on applicants, savvy entrepreneurs often require their own investigations for business partnerships or investments. For comprehensive background checks and corporate due diligence, many turn to professional firms like the International Investigative Group.

Can I use a co-borrower who is a W-2 employee to help me qualify?

Yes, including a co-borrower with W-2 income is a common and effective strategy. Lenders can use the co-borrower’s verifiable salary to strengthen the loan application in two ways: by combining their income with your calculated bank statement income or by using it to offset joint debts. This improves the overall debt-to-income (DTI) ratio, potentially increasing your borrowing power and securing more favorable loan terms. The co-borrower shares full financial responsibility for the mortgage.

If I pay myself a salary from my S-Corp, do I still count as self-employed?

Yes. For mortgage qualification, you are considered self-employed if you have 25% or more ownership in the S-Corporation, regardless of whether you draw a W-2 salary. A bank statement loan is designed for this scenario, as it allows underwriters to bypass the complex analysis of K-1s and corporate tax returns. Instead, the focus is placed on the consistent gross revenue demonstrated in your business bank statements to determine qualifying income for the loan.

What are the benefits of a P&L loan compared to a bank statement loan?

A Profit & Loss (P&L) loan is a strong alternative when business bank statements do not accurately reflect net income, often due to high but legitimate expenses, commingled funds, or inconsistent deposit patterns. A P&L prepared and signed by a licensed CPA can present a clearer picture of profitability. While it requires additional third-party verification, it can enable qualification. A bank statement loan remains the more streamlined option if your business accounts show clean, consistent cash flow.