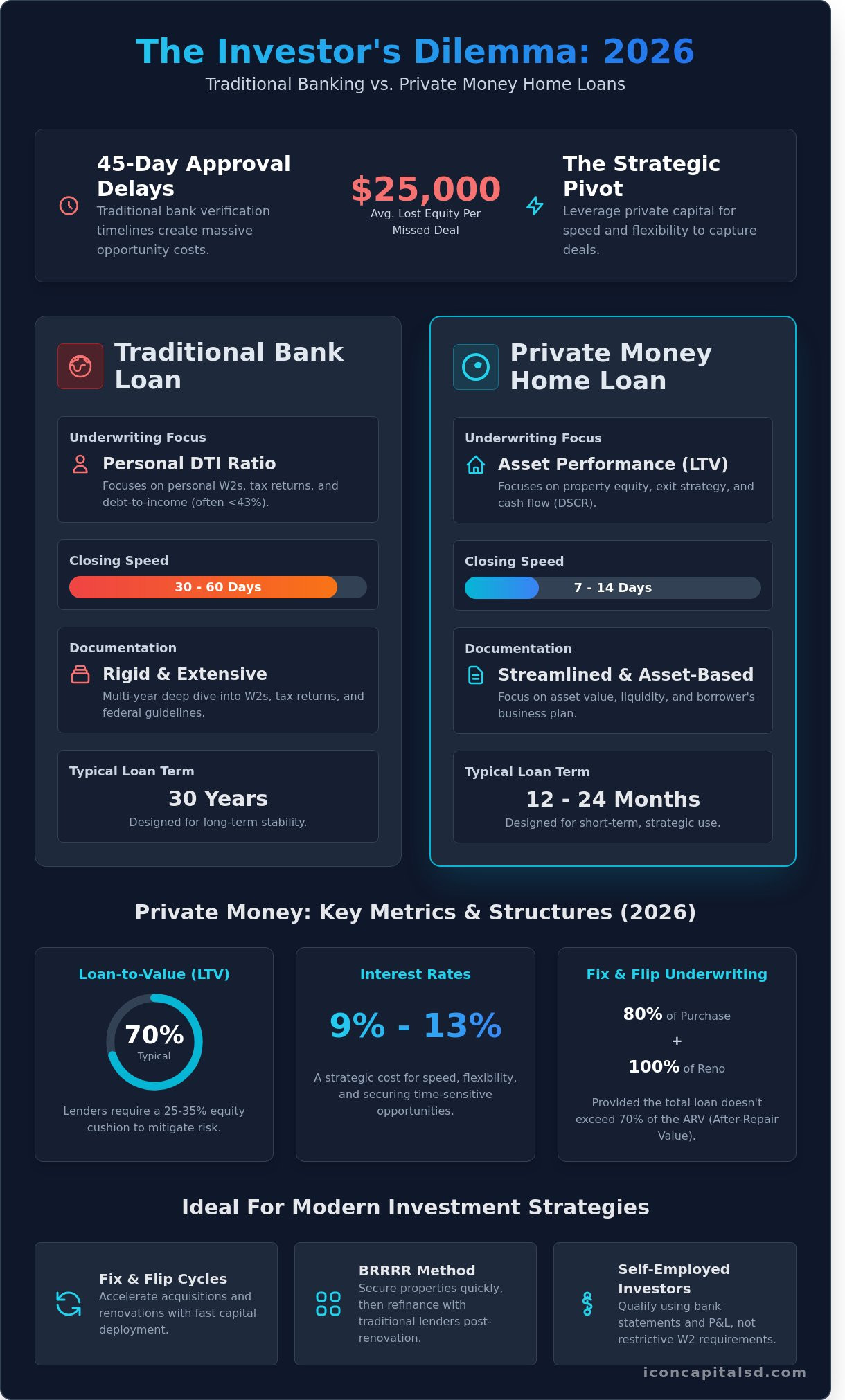

In 2026, waiting 45 days for a traditional bank to verify a tax return is a liability that costs investors an average of $25,000 in lost equity per missed deal. You already know that the most lucrative opportunities don’t wait for a legacy underwriter to approve your self-employment income. Traditional lenders often prioritize rigid W2 requirements over the actual value of the property, leaving sophisticated investors sidelined. Private Money Home Loans offer a strategic pivot; they allow you to secure funding based on asset performance and equity rather than personal debt-to-income ratios.

It’s clear that the standard mortgage process wasn’t built for the speed of modern real estate. You need a solution that prioritizes LTV and DSCR over a paycheck stub. This guide shows you exactly how to leverage asset-based qualification to close deals in under 14 days. We’ll explore how to bypass traditional friction and establish a reliable capital partnership to scale your portfolio with the speed and flexibility your business requires.

Key Takeaways

- Shift the focus from personal DTI to property equity by utilizing asset-based underwriting for faster funding.

- Identify 2026 LTV benchmarks to maximize leverage and maintain healthy equity positions across your portfolio.

- Distinguish between short-term bridge capital and Private Money Home Loans to align your financing with specific exit strategies.

- Apply creative financing techniques to accelerate Fix and Flip and BRRRR investment cycles without traditional banking friction.

- Reduce closing timelines through direct access to decision-makers and a no-nonsense approach to complex deal structuring.

What is a Private Money Home Loan? Defining the Strategic Alternative

A private money home loan represents a debt instrument secured by real estate but funded by non-bank entities. These sources include high-net-worth individuals and specialized investment funds rather than traditional depository institutions. This ecosystem, often categorized under Private Money Investing, operates on the logic of asset performance. While a bank prioritizes your personal history, a private lender prioritizes the property’s exit strategy and current equity position.

The fundamental shift occurs in the underwriting room. Traditional lenders focus on a borrower’s Debt-to-Income (DTI) ratio, often requiring it to stay below 43% for conventional approval. Private Money Home Loans pivot to the Loan-to-Value (LTV) ratio and the property’s intrinsic worth. If a property carries a 35% equity cushion, the deal often proceeds regardless of the borrower’s personal tax returns. This focus on collateral allows for capital deployment in scenarios where traditional credit boxes fail to provide a solution.

Market conditions in Q2 2026 have increased the demand for this financial agility. With interest rate volatility moving spreads by 50 basis points in a single week, investors can’t wait for a 45-day bank approval cycle. Private capital is the preferred tool for the 72% of active investors who require closing speeds under 10 business days to secure distressed assets or time-sensitive opportunities. It’s a strategic choice for those who value opportunity cost over the lowest possible interest rate.

Distinguishing between “Friends and Family” capital and institutional private lending is critical for scaling. While a personal loan from a contact might offer flexible terms, it lacks the scalability and legal structure required for professional portfolios. Institutional private lenders provide standardized draws for construction and loan amounts up to $10 million. They offer a level of reliability and capital depth that casual lending cannot match, ensuring the fund is available when the deal is ready to close.

Private Money vs. Traditional Mortgages

Traditional mortgages are designed for 30-year stability; private loans are designed for speed. A typical bank approval requires 30 to 60 days of processing. Private lenders often issue a Letter of Intent (LOI) within 24 hours and close within 7 days. Documentation is streamlined. We focus on the asset’s value and the borrower’s liquidity rather than a multi-year deep dive into W2 history. This regulatory flexibility allows for custom-tailored loan structures that don’t fit rigid federal guidelines.

The Role of Non-QM in Private Financing

Non-Qualified Mortgages (Non-QM) serve as the bridge between private capital and the broader market. These programs are essential for the 16 million self-employed individuals in the U.S. who may have high cash flow but significant tax deductions. Private channels leverage 12-month or 24-month bank statements and Profit and Loss (P&L) statements to verify ability to repay. Private Money Home Loans act as the primary engine for this creative financing. They allow investors to scale portfolios by using the income generated by the property itself rather than personal salary.

The Mechanics of Private Money: How These Loans Are Structured

Private money structures prioritize the underlying asset over the borrower’s personal financial history. This shift in focus allows for rapid deployment of capital, often closing in as little as 7 to 10 days. In the 2026 lending environment, most private lenders require a Loan-to-Value (LTV) ratio between 65% and 75%. This ensures a 25% equity buffer to protect the investment from market volatility. While traditional banks focus on debt-to-income ratios, private lenders analyze the property’s ability to generate a return or its immediate resale potential.

Interest rate structures in this space balance higher costs with the value of speed. You’ll typically see rates ranging from 9% to 13% depending on the risk profile. While these rates exceed those of conventional mortgages, the lack of red tape allows investors to secure properties that would otherwise be lost to competitors. The structure is designed for short-term use, usually spanning 12 to 24 months, making the total interest paid a manageable cost of doing business.

Collateral-Based Underwriting Standards

Lenders evaluate two primary values: the “as-is” value and the “after-repair” value (ARV). For a standard fix-and-flip project, a lender might fund 80% of the purchase price and 100% of the renovation costs, provided the total loan doesn’t exceed 70% of the ARV. Property type influences these terms significantly. Single-family residences often see the most aggressive LTVs. In contrast, multi-unit properties or commercial assets might face a 60% LTV cap due to the increased complexity of the valuation.

Credit scores don’t dictate the approval in private deals as they do in retail banking. A score of 620 might be acceptable if the equity position is strong. Lenders view the credit report primarily as an indicator of the borrower’s ability to execute an exit strategy. Successful investors often Raise Capital For Real Estate by leveraging these asset-heavy models to bypass the 45-day wait times common in traditional finance. When the property is the primary security, the borrower’s liquidity and experience take precedence over a FICO score.

Common Terms and Fee Structures

Borrowers should expect to pay points and origination fees ranging from 2% to 4% of the total loan amount at closing. These upfront costs represent the price of access to non-institutional capital. Most Private Money Home Loans utilize interest-only payment structures to keep monthly overhead low. This setup maximizes cash flow during the construction or stabilization phase. For example, on a $500,000 loan at 10% interest, the monthly payment stays at $4,166, with no principal reduction required. This allows the investor to keep more cash in the project for materials and labor.

It’s vital to check for prepayment penalties in the fine print. Many private contracts include a three-month or six-month minimum interest guarantee. If you flip a house in 60 days but your contract has a 90-day minimum, you’ll still owe that third month of interest. Understanding these nuances ensures there are no surprises at the closing table. If you’re ready to review a term sheet, you can structure your loan with our team to ensure the timeline matches your specific project goals.

A clear exit strategy is the foundation of every private money agreement. Lenders don’t want to own your property; they want their capital returned with interest. Before signing, you must demonstrate exactly how the debt will be satisfied. Common exits include selling the property for a profit or transitioning into a long-term DSCR loan once the property is leased. In 2026, lenders are scrutinizing these exit plans more than ever, often requiring a “Plan B” if the primary sale or refinance hits a hurdle.

Private Money vs. Hard Money: Choosing the Right Leverage

Investors often use the terms hard money and private money interchangeably. This is a technical error. Hard money is a specific, asset-based tool designed for rapid acquisition and heavy renovation. These loans typically carry interest rates between 9% and 12% with terms rarely exceeding 12 to 24 months. Private Money Home Loans offer a different profile. They bridge the gap between rigid institutional requirements and the high costs of short-term bridge debt by providing longer terms and more sustainable structures.

Analyzing the cost of capital requires looking beyond the interest rate. A 10% rate on a 6-month loan is often more profitable than a 7% bank loan that takes 60 days to close and causes you to lose a $450,000 acquisition. Speed is the primary metric for 82% of professional fix-and-flip investors. Understanding how private money lending works allows you to calculate the internal rate of return (IRR) based on deployment speed rather than just the annual percentage rate. Private capital focuses on the deal’s merit and the asset’s potential.

Relationship lending provides a level of certainty that institutional banks cannot match. When you work with a consistent private capital partner, the underwriting process for your fifth or tenth deal becomes streamlined. You aren’t just a loan number; you’re a proven operator. This partnership allows for higher leverage, often reaching 80% LTV on acquisitions and 100% of construction costs for experienced borrowers. This consistency is what enables investors to scale portfolios from single units to multi-family assets within a 12-month window.

When Hard Money Makes Sense

Hard money is the standard for distressed assets. If a property lacks a functioning kitchen or has significant structural issues, traditional lenders will reject the application. Use hard money for projects with high renovation needs where the budget exceeds 25% of the purchase price. It’s the correct choice for bridge scenarios where a 72-hour closing is the only way to secure a property in a market with a 1.5-month inventory supply.

The Case for Long-Term Private Financing

Private Money Home Loans are the preferred vehicle for stabilized rental portfolios. These products often utilize Debt Service Coverage Ratio (DSCR) underwriting, focusing on the property’s cash flow rather than the borrower’s tax returns. This is ideal for foreign national investors seeking U.S. real estate exposure who lack a domestic credit score but have 30% to 35% down payments. Most investors use these long-term private options to refinance out of high-rate hard money once a property is leased at market rates.

- Hard Money: 6-24 month terms, interest-only payments, 2-4 points upfront.

- Private Money: 5-30 year terms, DSCR-based qualification, competitive Non-QM rates.

- Speed: Hard money closes in 3-7 days; private long-term debt closes in 14-21 days.

- Asset Condition: Hard money accepts “shell” condition; private long-term debt requires “turnkey” or “stabilized” status.

Choosing the right leverage depends on your exit strategy. If the goal is a quick flip, the higher interest rate of hard money is a negligible cost of doing business. If the goal is a long-term hold, transitioning into a private money loan provides the 30-year amortization necessary to maximize monthly cash flow. Icon Capital structures these solutions based on the specific phase of your investment lifecycle.

Strategic Use Cases for Real Estate Investors

Investors utilize Private Money Home Loans to execute high-velocity strategies that traditional retail banks won’t touch. Speed is the primary driver here. In a fix and flip scenario, a private lender can fund a deal in 7 to 10 days, whereas a conventional mortgage takes 30 to 45 days. These lenders typically provide up to 90% of the purchase price and 100% of the renovation budget. This leverage allows an investor to control a $500,000 project with as little as $50,000 in liquidity.

The BRRRR method (Buy, Rehab, Rent, Refinance, Repeat) relies on this capital to fuel the initial acquisition. Once the property is stabilized with a tenant, the investor uses a cash-out refinance to pay back the private lender. This strategy recycles the same capital across multiple deals. Without the flexibility of private capital, investors would wait 6 to 12 months for traditional seasoning periods, stalling their growth.

Foreign national loans provide a specific pathway for international investors to enter the US market. These borrowers often lack a Social Security number or a domestic credit score. Private lenders fill this gap by focusing on a 30% or 35% down payment and the property’s performance. It’s a pragmatic approach that treats the real estate as the primary security for the debt.

Debt Service Coverage Ratio (DSCR) loans represent the most efficient way to hold long-term rentals. Qualification hinges on the property’s ability to pay for itself. Lenders analyze the gross monthly rent against the PITIA (Principal, Interest, Taxes, Insurance, and HOA). If the rent covers the debt, the loan moves forward regardless of the borrower’s personal debt-to-income ratio.

Scaling Portfolios with DSCR

DSCR is the ultimate tool for the landlord investor. To calculate it, simply divide the monthly rental income by the monthly debt obligation. A ratio of 1.20 indicates the property generates 20% more cash flow than the expenses require. This metric allows investors to bypass the 10-property limit found in conventional lending. You can scale to 15, 25, or 50 properties because the lender views each asset as a self-sustaining business unit.

Creative Solutions for Self-Employed Borrowers

Self-employed investors often find that their tax returns don’t reflect their true buying power due to aggressive business deductions. Bank statement loans solve this by using 12 or 24 months of deposits to verify income. If the cash is in the bank, the deal is viable. Asset qualification programs take this further, letting your total balance sheet prove repayment ability without requiring a traditional job. These Private Money Home Loans prioritize your actual net worth over a W-2. Request a quote for your next investment deal to see which program fits your current portfolio needs.

Ready to secure your next property? Explore our creative financing solutions to get started.

The Icon Capital Advantage: Simplifying the Loan Process

Securing capital requires a partner who understands the mechanics of the deal. Icon Capital LLC operates on a no-nonsense model designed for speed and technical precision. We eliminate the bureaucratic friction that often stalls traditional bank financing. Our team focuses on the asset’s value and the viability of your project rather than just personal credit history. This approach makes us a preferred choice for Private Money Home Loans in competitive markets where timing is the deciding factor between a closed deal and a lost opportunity.

Direct access to decision-makers is a core component of our service. You won’t wait weeks for a committee review. Our underwriters evaluate files within 24 to 48 hours of submission. We specialize in Non-QM products and creative investment structures that traditional lenders don’t touch. By prioritizing the technical mechanics of the transaction, we ensure that 95% of our pre-approved deals reach the closing table without last-minute surprises.

Our 4-Step Loan Process

Structure Loan: We begin by defining terms that align with your specific exit strategy. Whether you’re planning a 12-month fix-and-flip or a 30-year rental hold, we tailor the LTV and interest-only periods to maximize your cash flow. We analyze the DSCR and property potential immediately to confirm the deal’s feasibility.

Submit Loan: Our documentation process is lean. We’ve removed the fluff that adds days to the timeline. We require essential asset data and borrower information to move the file forward. This efficiency allows us to issue a term sheet while other lenders are still processing initial intake forms.

Underwrite: Professional evaluation focuses on the asset. We look at the property’s current value and its after-repair value (ARV). Our internal team understands Private Money Home Loans and how to mitigate risks without over-complicating the file. We use data-driven benchmarks to confirm the collateral’s strength.

Close: Fast funding keeps your projects on schedule. We target a 5-to-7-day closing window for most bridge and private money products. Our closing team coordinates directly with title and escrow to ensure funds are wired the moment the conditions are met. We don’t miss deadlines because we know your ROI depends on speed.

Why Investors Partner with Icon Capital LLC

Success in real estate investment depends on leverage and ROI. We speak the language of professional investors and provide the tools needed to scale portfolios quickly. Our solutions accommodate diverse borrower profiles, including those who don’t fit into standard lending boxes. We offer specific advantages that retail banks cannot match:

- Foreign National Programs: We provide financing for international investors with no U.S. credit required, using 65% to 70% LTV benchmarks.

- Business Owner Solutions: We utilize bank statement programs and 1099 income verification to bypass the limitations of tax-return-based underwriting.

- Creative Leverage: Our team structures cross-collateralization deals to help you extract equity from existing assets for new acquisitions.

- Technical Expertise: We understand complex entity structures, including LLCs, Trusts, and S-Corps, ensuring smooth title transfers and loan vesting.

Investors who need reliable, fast, and professional financing trust our team to deliver. If you’re ready to move forward with your next acquisition or refinance, Get a custom mortgage quote today to see how we can structure your deal for success.

Secure Your Competitive Edge in the 2026 Real Estate Market

Success in the 2026 investment landscape depends on your ability to deploy capital with speed and precision. Private Money Home Loans represent a critical tool for investors who need to bypass the rigid constraints of traditional banking. By prioritizing asset performance and deal structure over standard tax returns, these loans allow you to capture high-yield opportunities that others miss. You’ve learned how to distinguish these from hard money and how to use them for maximum leverage in your portfolio.

Icon Capital brings specialized expertise to every transaction. We provide dedicated solutions for foreign nationals and self-employed investors through our direct, data-driven underwriting process. Our focus on DSCR and Non-QM products ensures that your financing is as creative as your investment strategy. We handle the technical mechanics of loans up to $2 million, providing the liquidity you need to scale efficiently. It’s time to move past the limitations of conventional lending and start closing more deals.

Explore Creative Financing Options with Icon Capital

Your portfolio’s growth starts with the right financial partner.

Frequently Asked Questions

What are the typical interest rates for private money home loans in 2026?

Interest rates for private money home loans in 2026 typically range between 8% and 12% based on current market projections. These rates reflect the risk and speed of the capital provided. Investors often see 9.5% for bridge loans and 11% for fix and flip projects. Your final rate depends on the LTV and the specific deal structure.

Do I need a high credit score to qualify for a private money loan?

You don’t need a high credit score to qualify because these are asset-based loans. While traditional banks require a 720 FICO, private lenders prioritize the property’s value and equity. Some programs accept scores as low as 580. We focus on the deal’s exit strategy and the asset’s potential rather than just your personal credit history.

How much down payment is required for a private money home loan?

Most private money home loans require a down payment between 15% and 25% of the purchase price. For experienced investors with a strong track record, some lenders offer 10% down options. If the property has equity, you might leverage other assets to reduce the cash needed at closing. LTV ratios usually cap at 75% or 80% to protect the lender’s position.

Can I use a private money loan for my primary residence?

Private money loans are primarily for investment properties and business purposes rather than primary residences. Federal regulations like the Dodd-Frank Act impose strict requirements on consumer loans that most private lenders avoid. You can use this financing for a 4-unit rental or a fix and flip, but not for a home you intend to live in personally.

What is the difference between a private money lender and a hard money lender?

Private money lenders are typically individuals or small groups using their own capital; hard money lenders are more structured companies with pooled funds. Private money often offers more flexible terms and relationship-based underwriting. Hard money usually has set criteria and faster, more standardized processing. Both focus on the asset’s value rather than the borrower’s income.

How fast can a private money home loan close compared to a bank?

Private money loans close in 7 to 14 days, whereas traditional banks often take 30 to 60 days. This speed allows you to compete with cash buyers in hot markets. Our streamlined process removes the red tape of traditional underwriting. You get a term sheet within 24 hours and can move to funding once the title and appraisal are clear.

Are private money loans regulated by the government?

Private money lenders must follow state usury laws and federal fair lending practices. While they aren’t subject to the same Basel III requirements as commercial banks, they still operate under specific state licensing boards. In California, many lenders operate under a Department of Real Estate license or a California Financing Law license. Compliance ensures the loan is legally enforceable.

What happens if I cannot pay back a private money loan?

If you cannot repay the loan, the lender will initiate a foreclosure process to seize the collateral property. This typically begins after 30 to 90 days of non-payment depending on the loan agreement. The lender sells the asset to recover their principal and interest. It’s a standard legal procedure defined in the deed of trust or mortgage documents you sign at closing.