For self-employed professionals and real estate investors, the traditional mortgage application process is often a dead end. Your strong financial standing is frequently discounted because your income doesn’t fit into a standard W-2 format, leading to frustrating rejections and extensive paperwork. This is precisely where no income verification mortgage lenders provide a critical financing solution. These specialized lenders operate outside the rigid framework of conventional banking, offering a streamlined path to capital for qualified borrowers with non-traditional income streams.

For applicants looking to strengthen their credit profile to meet these stringent requirements, working with a professional credit consulting firm like Allen & Allen, Inc. can be a valuable step in the qualification process.

This definitive 2026 guide is engineered to demystify the process. We will detail how modern no-income-verification loans work-from asset-based qualification to DSCR loans for investment properties. You will gain a clear understanding of the mechanics and learn the key criteria for identifying a reputable lender for your specific financial situation. The objective is simple: to equip you with the knowledge to secure the financing you need and scale your portfolio without the documentation burdens of a traditional mortgage.

Key Takeaways

- Understand why true “no-doc” loans no longer exist and what “no income verification” means in today’s regulated market.

- Identify the main types of alternative documentation loans, including DSCR, bank statement, and asset-based programs.

- Learn the key metrics that no income verification mortgage lenders evaluate instead of pay stubs, such as LTV, credit, and asset reserves.

- Develop a clear framework for assessing the benefits and drawbacks of these programs to determine if one is right for your investment strategy.

What ‘No Income Verification’ Really Means in 2026

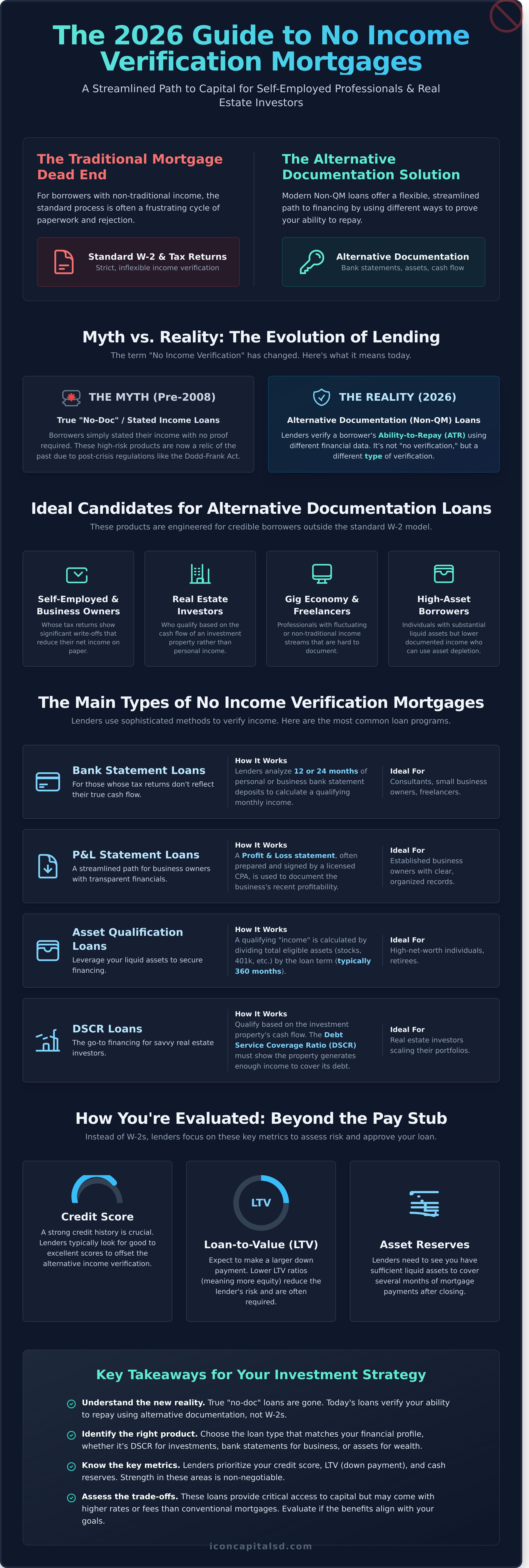

The search for no income verification mortgage lenders often leads to outdated information. In the current market, the true “no-documentation” or “no-doc” loan is a relic of the pre-2008 financial landscape. The regulatory framework established after the crisis fundamentally changed lending standards. Today, “no income verification” does not mean a lender ignores your financial standing; it means they use alternative methods to verify your ability to repay. These modern solutions fall under the category of Non-Qualified Mortgages (Non-QM).

The Myth of the ‘No-Doc’ Loan vs. Today’s Reality

The old system was characterized by stated income loans, where borrowers could simply state their income without providing proof. The 2008 financial crisis, largely fueled by these high-risk products, led to the Dodd-Frank Act. This legislation introduced the critical ‘Ability-to-Repay’ (ATR) rule, which mandates that all lenders make a good-faith effort to determine if a borrower can afford their mortgage payments. As a result, the concept of what ‘no income verification’ really means has shifted from a lack of verification to a different type of verification. Lenders are not taking your word for it; they are analyzing alternative financial data.

Who Are These Alternative Documentation Loans For?

Alternative documentation (Alt-Doc) loans are engineered for credible borrowers who cannot qualify using traditional W-2s and tax returns. The ideal candidates for these Non-QM products typically include:

- Self-Employed Professionals & Business Owners: Individuals whose tax returns show significant, legitimate write-offs that reduce their net income on paper. Lenders can use bank statements or profit & loss statements instead.

- Real Estate Investors: Borrowers who qualify based on the cash flow of an investment property (using a DSCR loan) rather than their personal income.

- Gig Economy Workers & Freelancers: Professionals with fluctuating or non-traditional income streams that are difficult to document with standard pay stubs.

- High-Asset Borrowers: Individuals with substantial liquid assets but lower documented income who can use asset depletion models to qualify for a loan.

In essence, today’s no income verification mortgage lenders are specialists in Non-QM and Alt-Doc financing. They provide essential liquidity for qualified borrowers who operate outside the standard W-2 employment model.

The Main Types of No Income Verification Mortgages

Modern “no income verification” loans are not the “no-doc” products of the past. Following regulations like the Consumer Financial Protection Bureau’s Ability-to-Repay rule, lenders must make a good-faith effort to confirm a borrower can afford their mortgage. This has led to the development of sophisticated Non-QM products that use alternative documentation methods to verify income, providing flexible solutions for non-traditional borrowers.

Understanding these loan types is the first step in identifying the right financing solution for your specific financial profile.

Bank Statement Loans

This is the most common solution for self-employed borrowers. Instead of tax returns, lenders analyze 12 or 24 months of personal or business bank statements to verify income. Underwriters calculate a qualifying monthly income by assessing the consistency of deposits, often applying a standard expense factor to business accounts. This product is ideal for consultants, small business owners, and freelancers whose tax returns may not accurately reflect their cash flow due to deductions and write-offs. To see if your bank statements are sufficient, request a free quote.

P&L (Profit and Loss) Statement Loans

For established business owners with transparent financials, a Profit and Loss (P&L) statement loan offers a streamlined path to qualification. This program allows a borrower to use a P&L statement, often prepared and signed by a licensed CPA, to document their business’s income. It is a ‘no tax returns required’ program, focusing instead on the recent and provable profitability of the enterprise, making it perfect for those with clear and organized financial records.

Asset Qualification / Asset Depletion Loans

Asset qualification loans allow borrowers to leverage their liquid assets to secure a mortgage. Lenders calculate a qualifying “income” by dividing the total value of eligible assets (such as stocks, bonds, 401(k)s, and mutual funds) by the loan term, typically 360 months. This method is an excellent fit for high-net-worth individuals or retirees who have substantial savings but may not have consistent W-2 or self-employment income.

DSCR Loans for Real Estate Investors

Designed specifically for real estate investors, the Debt Service Coverage Ratio (DSCR) loan qualifies a borrower based on the investment property’s cash flow, not personal income. The DSCR is a simple ratio comparing the property’s gross rental income to its proposed monthly mortgage payment. If the rental income covers the payment (a DSCR of 1.0 or greater), the loan is approved. This is a powerful tool from no income verification mortgage lenders that allows investors to scale their portfolios without their personal W-2s or tax returns acting as a bottleneck.

How to Qualify: What Lenders Evaluate Instead of Pay Stubs

When you apply for a loan with no income verification mortgage lenders, the underwriting process shifts its focus from traditional income proof to other key financial metrics. Lenders must mitigate their risk by confirming your ability to repay the loan through alternative, verifiable means. Instead of analyzing pay stubs and tax returns, these lenders scrutinize your financial stability through a different lens, a core principle behind all modern no-income verification mortgages. Success depends on demonstrating strength in three critical areas: credit, equity, and liquidity.

Credit Score and History

A strong credit profile is the foundation of a no-income loan application. Lenders view a high credit score as an indicator of responsible financial behavior and a history of meeting debt obligations. While requirements vary, a minimum FICO score in the 660-700 range is a typical starting point, with more favorable terms reserved for scores well above 720. A clean credit report, free of recent bankruptcies, foreclosures, or significant delinquencies, is essential.

Down Payment and Loan-to-Value (LTV)

A substantial down payment is almost always required to secure financing. By contributing more of your own capital, you reduce the lender’s risk exposure from day one. Expect a minimum down payment requirement of 20-30%, which is significantly higher than for conventional loans. This directly impacts your Loan-to-Value (LTV) ratio-the loan amount divided by the property’s appraised value. For no income verification mortgage lenders, a lower LTV (typically 70-80% or less) is a critical qualification factor.

Liquid Assets and Reserves

Beyond the down payment and closing costs, lenders need to see that you have sufficient liquid assets, often called post-closing reserves. These funds demonstrate your financial capacity to cover mortgage payments and other property-related expenses without strain. Lenders typically require you to have enough reserves to cover 6-12 months of total housing payments. Qualifying assets include:

- Cash in checking and savings accounts

- Stocks, bonds, and mutual funds

- Funds in retirement accounts (often valued at a percentage)

Finding and Vetting No Income Verification Mortgage Lenders

Securing financing without traditional income proof requires partnering with a lender specializing in Non-QM products. The right partner understands the complexities of asset-based and cash-flow lending, ensuring a smooth transaction. This section provides a framework for identifying and evaluating credible no income verification mortgage lenders.

Where to Find Lenders: Direct Lenders vs. Brokers

Borrowers typically engage with mortgage brokers, specialized direct lenders, or commercial real estate capital advisors like Flex V Capital LTD. A broker can access multiple lending sources but may not have deep expertise in any single Non-QM product. Conversely, a direct lender like Icon Capital LLC focuses exclusively on creative financing solutions. This specialization translates to a more streamlined underwriting process, faster closing times, and direct access to decision-makers who understand the nuances of your financial profile. To find these partners, search for terms like ‘Non-QM lenders’ or ‘Bank Statement loan lenders’.

Key Questions to Ask a Potential Lender

Due diligence is critical to ensure a transparent and predictable lending experience. Before committing, ask any potential lender these key questions to assess their programs and capabilities:

- What are your typical interest rates and associated fees for this loan program?

- What are your specific down payment, LTV, and cash reserve requirements?

- What is your average time to close for a borrower with my profile?

- Can you provide testimonials from other self-employed borrowers or investors you’ve worked with?

The Application Process: What to Expect

While different from a conventional loan, the application process for these specialized loans is methodical. Expect to move through pre-qualification, formal application, underwriting, and closing. Instead of tax returns, you will need to gather alternative documentation such as 12-24 months of personal or business bank statements, evidence of significant assets, or a P&L statement prepared by a CPA.

The underwriting and appraisal stages are focused on the documented cash flow or the asset itself, not personal W-2 income. Our streamlined process is designed for efficiency to help you secure financing quickly. Request a quote to get started.

Pros and Cons of No Income Verification Mortgages

While no income verification mortgages provide a critical financing solution for many borrowers, they are a specialized product with distinct trade-offs. Understanding the benefits and drawbacks is essential for making a sound financial decision. This balanced overview is designed to clarify whether this path aligns with your specific investment or homeownership goals.

Key Advantages

- Access to Capital: These loans are a vital tool for self-employed borrowers, real estate investors, and individuals with complex income streams who are often disqualified from traditional QM loans despite having a strong ability to repay.

- Simplified Documentation: For business owners with significant tax write-offs, the ability to qualify without tax returns is a primary benefit. Underwriting focuses on actual cash flow or assets, not adjusted gross income.

- Faster Closings for Investors: DSCR loans, a popular type of no-income-doc mortgage, can often close faster than conventional loans because underwriting is based on property cash flow rather than personal income verification.

- Asset-Based Underwriting: Lenders use practical, common-sense metrics to qualify borrowers, such as bank statement deposits, asset depletion, or the investment property’s income potential.

Potential Disadvantages

- Higher Interest Rates: The most significant trade-off is the cost. Lenders take on more perceived risk, which is priced into the loan with interest rates that are typically 1-3% higher than conventional mortgages.

- Larger Down Payment: Expect a higher barrier to entry. Most programs require a minimum down payment of 20-25% to ensure the borrower has significant equity in the property from day one.

- Potentially Higher Fees: Origination fees and points may be higher than on a standard loan to compensate for the specialized nature of the underwriting and processing.

- Fewer Lender Options: The market for these products is smaller. Borrowers must find specialized no income verification mortgage lenders with the expertise to structure and fund these loans.

A Practical Cost Comparison

To quantify the difference, consider a $700,000 loan. A conventional mortgage at 6.0% would have a monthly principal and interest payment of approximately $4,197. A comparable no-income verification loan at 8.0% would result in a payment of around $5,136. This difference of nearly $940 per month is the premium for flexible underwriting. For many real estate investors and entrepreneurs, the opportunity to acquire a cash-flowing asset or primary residence makes this additional cost a calculated business expense.

Ultimately, the decision depends on your financial profile and objectives. If traditional lending is not an option, the programs offered by experienced no income verification mortgage lenders can be an effective strategy to build your real estate portfolio. To explore your specific options, contact our loan specialists for a direct consultation.

Your Next Step in Creative Real Estate Financing

The landscape of mortgage lending has evolved. As we’ve explored, ‘no income verification’ in 2026 is not about a lack of documentation, but a shift towards alternative qualification methods like bank statement analysis or asset verification. This opens powerful avenues for self-employed borrowers and real estate investors with strong cash flow but non-traditional income streams. Successfully working with no income verification mortgage lenders means understanding these products and partnering with a specialist who can structure the right deal for your portfolio.

For those with complex financial profiles, finding a direct lender who understands your situation is critical. Icon Capital specializes in Non-QM and alt-doc loan products, offering a streamlined process built for investors and entrepreneurs. We remove the barriers of conventional lending to get your deal done efficiently. Explore your creative financing options with Icon Capital and see how our expertise can help you scale your investments.

The right financing solution can unlock your next opportunity.

Frequently Asked Questions

Can I get a no income verification mortgage with bad credit?

Yes, securing a no income verification mortgage with a lower credit score is possible. Lenders typically offset the increased risk with stricter requirements, such as a larger down payment to achieve a lower loan-to-value (LTV) ratio, or a higher interest rate. While some programs may accommodate scores as low as 600, a stronger credit profile will always secure more favorable terms. The key is to present compensating factors like significant liquid assets or a strong property profile.

Are interest rates significantly higher on no income verification loans?

Interest rates for no income verification loans are typically higher than those for conventional, fully documented mortgages. This premium reflects the increased risk the lender assumes by forgoing traditional income proof like W-2s or tax returns. Borrowers can generally expect rates to be 1% to 3% higher than the market rate for a comparable QM loan. The final rate depends on factors like credit score, LTV, loan type (e.g., DSCR vs. bank statement), and overall deal structure.

How much of a down payment is typically required for these mortgages?

A larger down payment is standard for no income verification mortgages. Most lenders require a minimum of 20% down, with 25-30% being more common, especially for borrowers with lower credit scores or on investment properties. For DSCR loans, the required down payment is directly tied to the property’s cash flow. A higher down payment reduces the lender’s loan-to-value (LTV) ratio and demonstrates the borrower’s financial commitment, mitigating risk and strengthening the application.

Are no income verification loans available for refinancing a property?

Yes, these loan products are widely available for refinancing. Property owners can use them for both rate-and-term refinances to secure a new rate or for cash-out refinances to access their property’s equity. This is a common strategy for real estate investors looking to leverage one property’s value to fund another acquisition or for self-employed individuals who need to tap into equity without providing extensive income documentation. The qualification process is similar to a purchase loan.

What is the difference between a Non-QM loan and a no income verification loan?

Non-QM (Non-Qualified Mortgage) is a broad category of loans that do not meet the strict criteria for conventional Qualified Mortgages. A no income verification loan is a specific type of Non-QM loan. The Non-QM umbrella includes various products like bank statement loans, DSCR loans, and asset-based loans, all of which use alternative methods to qualify a borrower. Essentially, all no income verification loans are Non-QM, but not all Non-QM loans are no income verification.

How quickly can I expect to close on a bank statement or DSCR mortgage?

The closing timeline for bank statement and DSCR mortgages is often comparable to, or even faster than, conventional loans. Because no income verification mortgage lenders are not collecting and verifying tax returns or pay stubs, the underwriting process can be more streamlined. A typical closing can take place within 21 to 30 days from the submission of a complete loan package, assuming the appraisal and title work are completed without delays. Efficiency is a key advantage of these programs.

Are these loans legal and safe in today’s market?

Absolutely. Today’s no income verification mortgage lenders operate in a highly regulated environment established after the 2008 financial crisis. These are not the “stated income” loans of the past. Lenders are still required by law (the Ability-to-Repay rule) to make a good-faith determination that you can afford the loan. They simply use alternative documentation, like bank statements or property cash flow, to do so, providing a safe and legal financing solution for qualified, non-traditional borrowers.