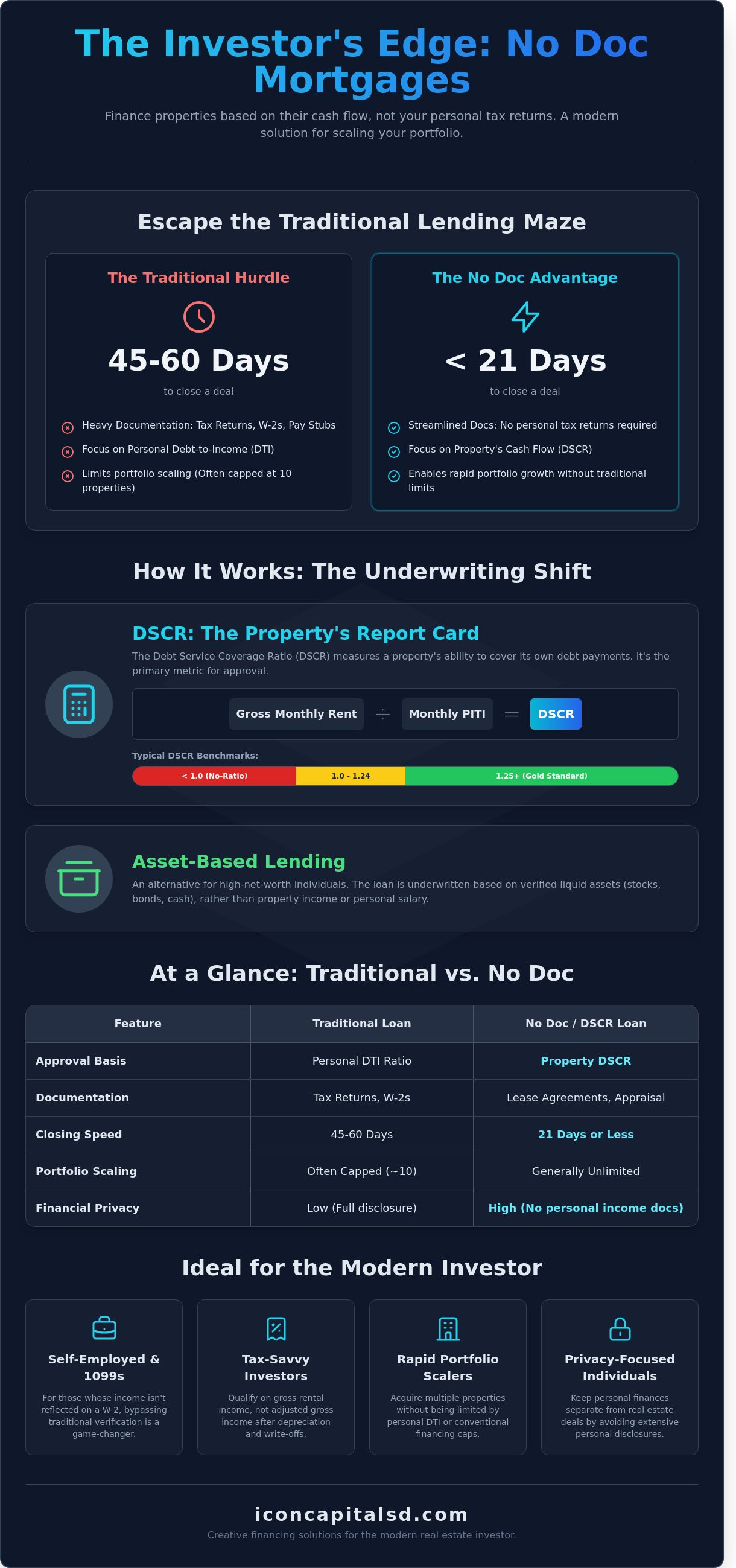

What if your personal tax returns had zero impact on your ability to secure a multi-million dollar real estate deal? Traditional debt-to-income limits and complex tax filings often create artificial barriers that hide actual cash flow. This results in lost opportunities, especially when conventional banks take 45 to 60 days to process a single application. Utilizing a no doc mortgage investment property allows you to decouple personal income from property financing. This strategy prioritizes the asset’s performance rather than your personal 1040.

You already know that waiting on a standard underwriter is the fastest way to lose a competitive bid in the 2026 market. We’ll show you how to leverage these creative financing tools to maximize your leverage and close deals with institutional efficiency. This guide covers the essential requirements for DSCR loans, asset-based lending structures, and the streamlined path to expanding your holdings without the typical paperwork burden.

Key Takeaways

- Accelerate your acquisition timeline by closing deals in 21 days or less to effectively compete with cash buyers.

- Understand the shift from personal income verification to property-centric underwriting using Debt Service Coverage Ratio (DSCR) mechanics.

- Leverage a no doc mortgage investment property to bypass tax return requirements and scale your portfolio with minimal financial documentation.

- Identify the specific credit score benchmarks and LTV expectations required to qualify for high-leverage Non-QM financing.

- Explore specialized lending solutions for 5-8 unit multi-family properties and financing options for foreign national investors.

What Is a No Doc Mortgage for Investment Property?

A no doc mortgage investment property loan is a specialized Non-QM financing product designed for real estate professionals who cannot or choose not to provide traditional income documentation. In the 2026 lending market, “No Doc” refers specifically to the exclusion of personal tax returns, W-2s, or pay stubs from the underwriting process. It does not mean the loan lacks oversight. Instead, the underwriting focus shifts from the borrower’s personal income to the value and revenue potential of the underlying asset.

Non-QM lenders use alternative methods to verify a borrower’s ability to repay. This often involves analyzing liquid assets or the property’s Debt Service Coverage Ratio (DSCR). If the rental income covers the mortgage payment, the deal is viable. This structure benefits self-employed investors and 1099 contractors who utilize legal tax deductions that lower their adjusted gross income. High-net-worth individuals also use these products to maintain privacy and avoid the administrative burden of traditional bank disclosures. Investors often ask What is a no-documentation loan in the context of modern regulations; it’s a tool for efficiency, not a shortcut around creditworthiness.

The Evolution of No-Income Verification Loans

Modern no-doc products bear little resemblance to the “Stated Income” loans that preceded the 2008 financial crisis. Following the 2010 Dodd-Frank Act, strict Ability to Repay (ATR) rules were established to protect the market. Today’s no doc mortgage investment property options are fully compliant because they establish ATR through property-level cash flow rather than borrower-level salary. While traditional QM loans enforce a strict 43% Debt-to-Income (DTI) ratio, Non-QM lenders bypass personal DTI entirely. They prioritize the asset’s performance, typically requiring a DSCR of 1.0x to 1.25x to ensure the property is self-sustaining.

Common Use Cases for Real Estate Investors

- Optimizing Tax Strategy: Many successful investors show minimal taxable income due to depreciation and expenses. A no-doc loan allows them to qualify based on gross rental receipts instead of the bottom line on a Schedule C.

- Rapid Portfolio Scaling: Traditional banks often cap the number of financed properties at 10. Non-QM lenders allow investors to acquire multiple properties simultaneously without the constraints of personal debt ratios.

- Stabilization Bridges: Investors use these loans to secure properties quickly, then refinance once the asset is fully leased and stabilized.

Icon Capital provides the expertise needed to structure these complex deals. If you need to leverage your assets without the paperwork of a traditional bank, request a quote to see your available leverage options. We focus on the numbers that matter: your property’s potential and your total liquidity.

How No Doc Mortgages Work: DSCR vs. Asset-Based Lending

A no doc mortgage investment property loan operates on the principle that the asset, not the individual, should qualify for the debt. Unlike traditional financing that requires W-2s and 1040 tax returns, these programs use alternative verification methods to gauge risk. The two primary paths involve analyzing the property’s income potential or the borrower’s total liquid net worth. For self-employed investors, “Lite Doc” options like Bank Statement or P&L loans provide a middle ground, using 12 to 24 months of deposits to calculate qualifying income without looking at IRS filings.

The appraisal process is the pivot point for these deals. Lenders require a 1007 Rent Schedule, which is a specific addendum where the appraiser determines the fair market rent for the subject property. This figure often supersedes the actual lease agreement if the current rent is below market value. Investors often leverage modern alternatives to no-doc loans to bypass the rigorous income documentation typically required by institutional banks.

The DSCR Framework: Rents vs. PITI

The Debt Service Coverage Ratio (DSCR) is the standard metric for investment property lending. It’s calculated by dividing the gross monthly rent by the PITI (Principal, Interest, Taxes, and Insurance). A ratio of 1.2x is the industry gold standard, meaning the property generates 20% more income than its debt obligations. If you’re looking for deeper technical details, read What Is a DSCR Loan? The Ultimate Guide for Real Estate Investors.

Some programs offer “No-Ratio” options. These allow for qualification even if the DSCR is below 1.0, provided the investor has a high credit score and significant equity. This is a strategic tool for properties in high-appreciation markets where immediate cash flow is secondary to long-term capital gains. If you’re ready to see how these ratios apply to your next acquisition, you can request a quote to review current market terms.

Asset-Based and No-Ratio Alternatives

Asset Qualification is the use of total net worth to secure property leverage. This method ignores monthly cash flow entirely, focusing instead on liquid reserves such as cash, stocks, and 401(k) accounts. Lenders typically require the borrower to show enough liquidity to cover the loan amount or a specific multiple of the monthly payments for a set period, often 60 months.

LTV limits vary based on the chosen subtype. While a standard DSCR loan might allow for 80% LTV, No-Ratio or pure asset-based programs often cap leverage at 70% or 75% to mitigate risk. This trade-off provides maximum privacy and speed, as the underwriter spends zero time verifying employment or historical income. The focus remains strictly on the strength of the collateral and the borrower’s capital position.

The Strategic Advantages of No-Income Verification Loans

The no doc mortgage investment property model prioritizes asset performance over personal tax returns. This shift offers significant leverage for active investors. Conventional lenders often mandate a 45 to 60 day closing window. Non-QM products reduce this to 21 days or less. This speed allows investors to compete with cash buyers in a high-demand 2026 market where inventory remains tight and competition is fierce.

Privacy is a primary driver for high-net-worth individuals and professional flippers. These loans eliminate the need for invasive financial audits. Underwriters focus on the property’s cash flow rather than personal bank statements or W-2s. Additionally, these programs support complex ownership structures including:

- Limited Liability Companies (LLCs)

- S-Corporations and C-Corporations

- Family or Revocable Trusts

Using these structures protects personal assets and simplifies tax reporting. Conventional financing often hits a wall at the 10-loan limit due to Fannie Mae and Freddie Mac regulations. No-doc programs offer unlimited scalability. You can expand your portfolio to 20, 50, or 100 properties without hitting arbitrary regulatory caps that stop traditional borrowers.

Bypassing the Debt-to-Income (DTI) Bottleneck

Traditional DTI calculations often stall an investor’s growth. Your personal mortgage, student loans, or car payments shouldn’t block a profitable acquisition. No-doc loans use Debt Service Coverage Ratio (DSCR) metrics. If the projected rent covers the debt service, the loan is viable. This keeps your personal credit profile clean for other financing needs. It also facilitates scaling into larger assets, such as 5 to 8 unit multi-family buildings, using commercial-style underwriting standards that ignore personal income levels.

Closing with Speed and Confidence

A 3-week close provides a distinct competitive edge. In the 2026 market, sellers prioritize certainty and speed over the highest offer price. Reducing the paperwork burden allows busy professionals to focus on deal sourcing rather than document gathering. For those involved in rapid transitions or renovations, understanding the Types of Loans for Flipping Houses: A Complete Investor’s Guide is essential for matching the right capital to the right project. Efficiency is the key to maintaining a high ROI. This streamlined approach ensures you don’t lose a deal to a more agile competitor while waiting for a traditional underwriter to review two years of tax transcripts.

Qualifying for a No Doc Rental Loan: Requirements & Process

Securing a no doc mortgage investment property requires a shift in focus from personal income to asset performance. Lenders don’t look at W2s or tax returns. Instead, they prioritize the property’s revenue potential and the borrower’s credit depth. A credit score between 620 and 680 serves as the standard entry point for most Non-QM programs. While scores in this range are acceptable, investors with a 720 or higher typically access the most aggressive interest rates and leverage options.

Loan-to-Value (LTV) expectations for 2026 center on risk mitigation. Most programs cap at 80% LTV for purchases. For cash-out refinances, lenders often limit leverage to 70% or 75%. The appraisal is the most critical stage of the qualification process. Unlike traditional residential appraisals, this process includes a Form 1007 Market Rent Schedule. This document verifies the property’s projected income. If the market rent doesn’t meet the lender’s specific Debt Service Coverage Ratio (DSCR) requirements, the LTV might be reduced to balance the risk.

Documentation requirements are streamlined but non-negotiable. Investors must provide specific business and property records to close the deal. These typically include:

- LLC Operating Agreement and Articles of Organization

- Proof of hazard and liability insurance coverage

- A preliminary title report

- Bank statements confirming the required cash reserves

The 4-Step Underwriting Process

Step 1: Application and Credit Pull. We establish the baseline eligibility and credit tier immediately. This allows for an accurate initial quote based on current market spreads and your specific credit profile.

Step 2: Property Appraisal and Rent Schedule verification. A certified appraiser completes Form 1007. This verifies the property’s physical condition and confirms the achievable monthly rent in the current market.

Step 3: Underwriting review. The underwriter examines the deal structure, entity documents, and liquidity. They ensure the property meets all safety standards and the cash flow projections are realistic.

Step 4: Clear to Close. Once all conditions are satisfied, the loan moves to funding. This process often takes 21 days or less because it’s not slowed down by personal income audits.

Key Financial Benchmarks for 2026

Typical LTV ranges fluctuate between 65% and 80% based on the investor’s experience and credit score. Experience is a major factor; seasoned investors with five or more successful exits often access higher leverage. Reserve requirements are another critical benchmark. Lenders expect to see 3 to 12 months of PITI (Principal, Interest, Taxes, and Insurance) in a liquid account. These funds must be seasoned in a bank account for at least 60 days. You can Request a Quote to see today’s specific LTV limits for your deal.

Ready to leverage your next asset? Contact Icon Capital today to review your property’s cash flow potential.

Scaling Your Portfolio with Icon Capital’s Creative Financing

Scaling a real estate portfolio requires a lender that moves beyond standard residential limits. Icon Capital specializes in the 5 to 8 unit multi-family space, a niche often underserved by traditional banks that stop at four units or jump straight to large commercial tiers. We provide direct access to underwriters who specialize in these mid-tier assets. This direct line of communication allows for rapid decisions on complex investor scenarios that don’t fit a standard box. Whether you’re targeting a value-add bridge loan or a long-term no doc mortgage investment property solution, our team structures deals based on asset performance rather than personal income tax returns.

Our bridge and construction options are designed for investors executing aggressive value-add strategies. We understand that a property’s current state doesn’t always reflect its future potential. By focusing on the After Repair Value (ARV) and the viability of the renovation plan, we provide the liquidity needed to transform underperforming assets into high-yield rentals. This pragmatic approach ensures that your capital isn’t tied up in red tape while market opportunities pass you by. We prioritize the numbers that drive your ROI, not the paperwork that slows you down.

Solutions for Foreign Nationals and Expats

International investors often face significant barriers due to a lack of domestic credit history. Icon Capital eliminates these hurdles through specialized financing. We offer programs that leverage global assets to secure US real estate without requiring a US credit score or Social Security number. These specific No Doc programs focus on the property’s projected cash flow and the investor’s international liquid reserves. You can learn more by reading our Foreign National Loans: The Ultimate Guide to Investing in U.S. Real Estate. We provide a clear path for expats and foreign entities looking to capture US market yields without the typical documentation strain.

The Icon Capital Advantage: From DSCR to Fix & Flip

We act as a professional partner for the entire investor lifecycle. Our product suite covers every stage, from initial acquisition and rehab to the final long-term hold. Investors don’t need to switch lenders when transitioning from a fix and flip project to a permanent DSCR loan. This continuity saves time and reduces closing costs across your portfolio. We also provide specialized tools for growth:

- Customized loan structures for diverse portfolios.

- Blanket mortgages to consolidate multiple properties under a single lien.

- Direct underwriting for 5-8 unit multi-family acquisitions.

- Construction-to-perm options for ground-up developments.

Our 2026 acquisition strategy centers on speed and certainty of execution. We eliminate the friction of traditional documentation to keep your momentum high. If you’re ready to expand your footprint in the current market, Request a Quote to start your next acquisition. We prioritize the numbers that matter: debt service coverage and asset value. Secure a no doc mortgage investment property today and keep your capital working for you.

Accelerate Your Portfolio Growth with Strategic Financing

In the 2026 lending landscape, traditional income verification is no longer a barrier to expansion. A no doc mortgage investment property solution shifts the focus from personal tax returns to the cash flow of the asset or your existing liquidity. This pivot allows you to bypass the standard 30 day underwriting cycles typical of retail banks. Icon Capital provides the infrastructure to leverage these non-QM products, including specialized programs for 5 to 8 unit multi-family properties and dedicated pathways for Foreign National investors. Our fast-track underwriting process is engineered specifically for professional real estate investors who need to move quickly on high-yield opportunities. By prioritizing DSCR and asset-based metrics, you can secure financing without the constraints of debt-to-income ratios. It’s time to transition from documentation hurdles to deal-closing efficiency. You’ve seen how these tools work; now apply them to your next acquisition.

Secure your next investment with a professional No Doc loan quote from Icon Capital

Position your portfolio for long-term growth today.

Frequently Asked Questions

Can I get a no doc mortgage for an investment property in 2026?

Yes, you can secure a no doc mortgage investment property loan in 2026 through specialized Non-QM lending channels. These programs allow investors to bypass traditional tax return requirements by focusing on asset value and property cash flow. Icon Capital provides these creative financing solutions to help you scale your portfolio without the documentation hurdles typical of conventional banks. We focus on the deal’s viability rather than your personal tax history.

What is the minimum credit score for a no-income verification loan?

Most no-income verification programs require a minimum credit score of 620 to qualify for competitive terms. Higher scores often result in better LTV ratios and more favorable interest rates. Icon Capital evaluates your credit history alongside the property’s potential to determine the best structure for your deal. Investors with scores above 720 typically access the most aggressive leverage options available in the current 2026 market.

Do no doc mortgages have higher interest rates than conventional loans?

No doc mortgages typically carry interest rates 1% to 3% higher than standard conventional loans. Lenders charge this premium to offset the increased risk associated with limited income documentation. While the rate is higher, the speed of execution and the ability to close deals that traditional banks reject provide a strategic advantage for active real estate investors. This cost is often offset by the rapid acquisition of cash-flowing assets.

Is a DSCR loan the same as a no doc mortgage?

A Debt Service Coverage Ratio (DSCR) loan is a specific type of no doc mortgage investment property solution used by professional real estate firms. It qualifies the borrower based on the property’s rental income rather than personal tax returns or pay stubs. If the annual gross rent exceeds the annual debt service by a ratio of 1.0 or higher, the loan meets the primary qualification metric. This allows for rapid portfolio scaling.

Can a foreign national apply for a no doc investment loan?

Foreign nationals can apply for no doc investment loans to acquire or refinance U.S. real estate assets. These programs don’t require a Social Security number or U.S. credit history in many instances. Icon Capital utilizes international credit reports or alternative data to verify eligibility. This allows global investors to leverage their capital and expand their domestic property holdings efficiently. We handle the complexities of cross-border financing to ensure a smooth closing.

What is the typical down payment for a no-documentation rental loan?

Investors should expect a typical down payment of 20% to 25% for a no-documentation rental loan. Some specialized programs may require a 30% down payment depending on the property type and the borrower’s credit profile. This equity position protects the lender and ensures the investor has a vested interest in the asset’s performance. Higher down payments often streamline the underwriting process and may eliminate the need for secondary reserves.

How long does it take to close a no doc mortgage with Icon Capital?

Closing a no doc mortgage with Icon Capital generally takes between 14 and 21 business days from submission to funding. Our streamlined process eliminates the lengthy income verification steps and tax transcript requests required by traditional institutions. Once we receive the appraisal and title work, our underwriters move quickly to clear all conditions. This efficiency allows you to compete with cash buyers in high-demand markets where speed is critical.

Can I use an LLC to close a no doc investment property loan?

You can close a no doc investment property loan using an LLC, corporation, or partnership. Icon Capital encourages this structure because it provides liability protection and aligns with professional investment strategies. You’ll need to provide the entity’s formation documents and an operating agreement during the submission phase. This approach simplifies the management of multi-property portfolios and facilitates easier asset transfers between partners or family offices.