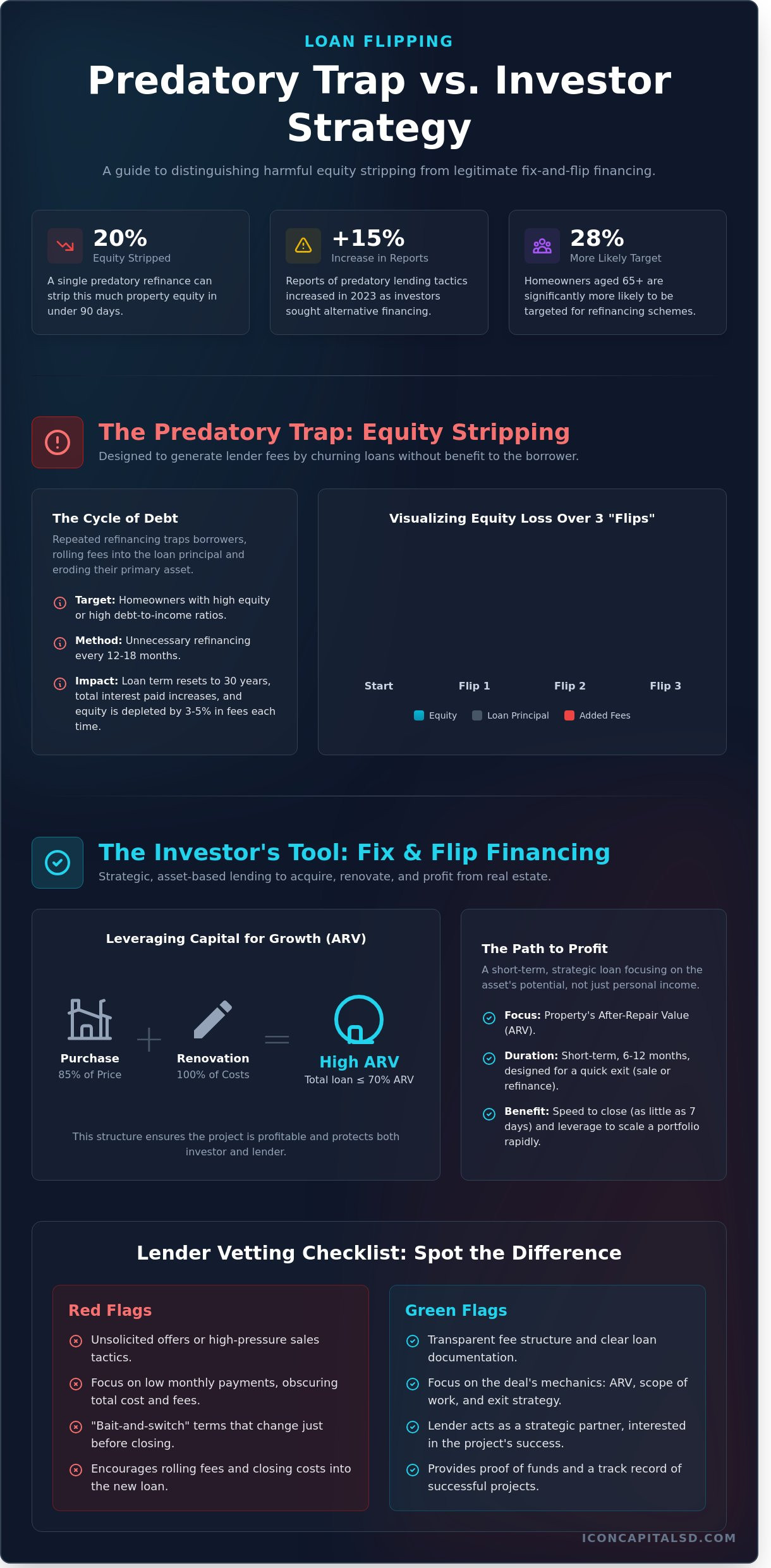

A single predatory refinance can strip 20% of your property’s equity in under 90 days. You know that rapid capital is essential for scaling a portfolio; however, the line between a strategic bridge loan and a predatory trap is often blurred. Loan flipping targets equity through repeated, unnecessary refinancing that generates excessive fees for the lender while draining your cash position. In 2023, reports of predatory lending tactics increased by 15% as more investors sought alternatives to traditional bank products.

It’s frustrating to search for transparent capital only to face hidden costs or bait-and-switch terms. You need a partner that focuses on the mechanics of the deal rather than empty promises. This article provides the technical framework to distinguish between predatory scams and legitimate fix-and-flip financing. You’ll learn how to protect your equity and identify the markers of professional, asset-based lending that actually supports your scale.

We’ll examine the specific red flags found in predatory contracts and outline the 4 key documentation standards required for high-leverage, non-QM investment funding.

Key Takeaways

- Distinguish between predatory refinancing practices and legitimate fix-and-flip financing to safeguard your investment equity.

- Learn to identify the psychological red flags and mathematical traps used in loan flipping scams to avoid equity depletion.

- Understand the fundamental differences between traditional income-based underwriting and professional asset-based Non-QM lending.

- Master a systematic framework for vetting investment lenders to ensure you secure reliable, transparent capital for your real estate projects.

- Discover how creative financing solutions and local market expertise allow serious investors to scale portfolios efficiently.

What is Loan Flipping? The Two Sides of the Term

The term loan flipping carries two distinct meanings in the 2026 mortgage market. For a homeowner, it often signals a predatory trap designed to strip equity through unnecessary refinancing. For a real estate investor, it describes a legitimate strategy for leveraging capital to renovate and resell property. Distinguishing between these two definitions is the first step in protecting your assets while accessing the growth capital required for scale.

In the current financial environment, where benchmark interest rates have stabilized at 5.25% after the volatility of the mid-2020s, many lenders are aggressively pursuing refinance volume. Predatory loan flipping occurs when a lender induces a borrower to refinance their mortgage repeatedly within a short window, often 12 to 18 months, without providing a net tangible benefit. The primary objective of this guide is to help you identify these harmful patterns while utilizing professional financing tools to build wealth. Clarity on these mechanics ensures you maintain a healthy debt-to-income ratio and preserve long-term equity.

The Predatory Definition: Equity Stripping

Predatory lenders profit by churning loans to generate points and administrative fees. A standard refinance in 2026 carries closing costs averaging 3% to 5% of the total loan amount. When a borrower is encouraged to refinance every year, these costs are typically rolled into the new principal balance. This process systematically reduces the homeowner’s equity. To understand the broader context of these unethical tactics, it’s helpful to review What is Predatory Lending? and how it targets vulnerable populations.

- Target Demographics: Statistics from 2025 indicate that homeowners aged 65 and older are 28% more likely to be targeted for frequent refinancing schemes.

- Fee Stacking: Lenders often charge 2 points upfront on each transaction, meaning a $500,000 loan flip generates $10,000 in immediate lender profit at the borrower’s expense.

- Financial Impact: Repeated flipping extends the loan term back to 30 years, ensuring the borrower pays more in interest over time while never reducing the principal.

The Investor Definition: Fix and Flip Leverage

Professional real estate investors use “flip loans” as a tool for rapid portfolio expansion. This is not loan flipping in the predatory sense; it’s asset-based lending. These products, such as bridge loans or hard money, are designed for short durations of 6 to 12 months. They allow an investor to acquire a distressed asset, renovate it, and exit the loan through a sale or a long-term DSCR (Debt Service Coverage Ratio) refinance once the property is stabilized.

Asset-based lending focuses on the property’s potential rather than just the borrower’s personal income. In 2026, a typical fix and flip loan provides up to 85% of the purchase price and 100% of the renovation costs, provided the total loan doesn’t exceed 70% of the After-Repair Value (ARV). These loans carry higher interest rates, often between 9.5% and 11%, but they serve as a necessary bridge to move from acquisition to profit. Successful investors use this leverage to close deals in as little as 7 days, a speed that traditional consumer mortgages can’t match. This distinction is vital for those looking to scale their operations without falling into the traps of predatory consumer debt.

Anatomy of a Loan Flipping Scam: Red Flags for Homeowners

Predatory lenders rely on psychological manipulation to initiate loan flipping. They target homeowners with high debt-to-income ratios or substantial home equity. These lenders frame refinancing as a financial rescue rather than a debt restructuring. They focus on the cash-out amount while obscuring the total cost of credit. Between 1998 and 2000, federal regulators increased oversight as predatory lending practices became a systemic risk. The math of these deals is destructive. A borrower might receive $5,000 in cash but pay $12,000 in points and fees rolled into the new balance. This process, known as churning, allows the lender to collect origination fees before selling the debt on the secondary mortgage market. The homeowner loses equity; the lender secures a quick commission.

The secondary market provides the liquidity that fuels these scams. When a lender flips a loan, they often sell the note to investors within 90 days. This removes the risk from the lender’s books while they retain the upfront fees. Because the lender doesn’t hold the loan long-term, they have no incentive to ensure the borrower can actually afford the payments. They prioritize volume over loan quality. This cycle erodes the borrower’s wealth. If you refinance a $350,000 mortgage three times in 36 months with 4% closing costs each time, you’ve added $42,000 to your debt without reducing your principal balance by a single dollar.

Unsolicited Offers and High-Pressure Sales

Legitimate firms rarely cold-call with guaranteed approvals. High-pressure tactics, like 24-hour expiration dates on quotes, prevent borrowers from consulting an attorney or a qualified lending specialist. It’s vital to verify a lender’s 12-digit NMLS ID via the Consumer Access portal before sharing financial data. If a solicitor discourages independent review, they’re likely hiding unfavorable terms.

Excessive Fees and Hidden Balloon Payments

Points are upfront fees calculated as 1% of the loan amount. Paying 3 or 4 points on a refinance that only lowers your rate by 0.25% is mathematically unsound. Balloon payments are large, lump-sum balances due at the end of a short term, often 5 or 7 years. These are used to force a borrower into another refinance. Prepayment penalties are tools for predatory lock-ins that charge you for paying off the loan early.

Immediate Red Flags Checklist:

- Unsolicited Contact: You receive a “personalized” offer for a loan you didn’t apply for.

- Frequent Refinancing: The lender suggests a new loan less than 18 months after your last closing.

- Negative Amortization: The monthly payments don’t cover the interest, causing the total debt to increase.

- Document Pressure: The loan officer asks you to sign blank documents or skip reading the “standard” disclosures.

- Fee Loading: Total closing costs exceed 5% of the loan amount without a significant reduction in interest rate.

- Mandatory Add-ons: The lender claims you must purchase credit life insurance to qualify for the loan.

Analyzing the Loan Estimate is the only way to spot loan flipping before it’s too late. Compare the “Total Interest Percentage” and the “Total of Payments” against your current mortgage. If the new loan doesn’t provide a tangible net benefit, such as a significantly lower interest rate or a shift from an adjustable to a fixed rate, the deal only benefits the originator. Professional investors always run the numbers on a 5-year and 10-year horizon to ensure the math holds up.

Predatory Refinancing vs. Professional Fix & Flip Loans

Predatory refinancing and professional real estate lending occupy opposite ends of the financial spectrum. While both involve debt, the intent differs fundamentally. Predatory lenders target equity in primary residences to strip wealth from vulnerable homeowners through high fees and repeated refinancing. This practice, commonly known as loan flipping, relies on the borrower’s lack of financial literacy. In contrast, professional fix and flip loans are commercial tools designed for profit. Investors utilize these high-leverage products to acquire and renovate distressed assets, turning a profit within a 6 to 12-month window. The professional borrower views the interest rate as a cost of goods sold, not a lifelong burden.

The regulatory environment reflects this distinction. Consumer loans are governed by the Truth in Lending Act (TILA) and the Ability to Repay (ATR) rule, which mandate strict income verification. Commercial lending focuses on the asset. Lenders evaluate the property’s potential rather than the borrower’s personal debt-to-income ratio. Government reports from as early as 2001 have detailed the dangers of property flipping when it involves fraudulent appraisals and predatory terms on residential homes. Legitimate commercial lending avoids these pitfalls by requiring skin in the game and clear transparency through standardized closing documentation.

Understanding Underwriting Standards

Professional underwriting relies on data-driven metrics to mitigate risk for both the lender and the investor. Unlike loan flipping schemes that ignore the borrower’s outcome, asset-based lending uses specific ratios to ensure a project’s viability. If a deal doesn’t meet these benchmarks, it doesn’t get funded. This objective analysis acts as a built-in safeguard against bad investments.

- DSCR (Debt Service Coverage Ratio): Lenders typically require a minimum 1.20x ratio. This means the property’s net operating income must cover the debt service by 120%, ensuring the asset generates enough cash to sustain itself.

- LTV (Loan-to-Value): Most Non-QM and fix-and-flip lenders cap LTV at 75% or 80%. This 20% to 25% equity buffer protects against market fluctuations and ensures the investor is committed to the project.

- Closing Disclosure Transparency: Legitimate deals use a Closing Disclosure or HUD-1 settlement statement. These documents clearly list every fee, commission, and interest charge, leaving no room for the hidden costs typical of predatory “churning.”

The Use of Leverage in Real Estate

Professional investors don’t fear high-interest capital; they use it strategically. A 10% or 12% interest rate is a tool for speed and scale. By using leverage, an investor can control a $500,000 asset with only $100,000 of their own capital. This allows them to diversify across multiple projects simultaneously. The goal is “borrowing for renovation and resale,” which adds value to the housing stock.

The defining characteristic of a professional loan is the exit strategy. Every legitimate short-term loan is underwritten with a clear plan to either sell the property or refinance into a long-term DSCR loan once the renovation is complete. Predatory lenders don’t want an exit; they want to trap the borrower in a cycle of debt. Professional lenders, however, prioritize the successful completion of the project. Their business model depends on the borrower’s ability to successfully exit the loan and move on to the next deal, creating a repeatable cycle of growth rather than a spiral of equity loss.

How to Vet Investment Lenders and Secure Safe Capital

Avoiding loan flipping requires a data-driven approach to lender selection. Professional investors prioritize transparency and execution over the lowest teaser rate. A reliable lending partner provides clear, written terms and demonstrates a deep understanding of the capital stack. You should evaluate a lender based on their ability to close complex deals, such as those involving 90% LTC (Loan to Cost) or 75% LTV (Loan to Value) on a cash-out refinance. A professional framework ensures you aren’t caught in a cycle of predatory refinancing that erodes your equity.

Local market knowledge is a non-negotiable asset in investment lending. A lender familiar with specific zip codes and neighborhood appreciation trends can provide more accurate valuations than an out-of-state call center. They understand that a property in a 92101 zip code carries different risk profiles than one in a rural county. This expertise allows for more aggressive leverage and faster appraisals, which are critical in competitive markets where a 10-day closing window is the standard.

Specialized Non-QM and creative lenders offer flexibility that traditional banks cannot match. These institutions focus on the asset’s performance, using metrics like the Debt Service Coverage Ratio (DSCR) rather than just personal income. If your DSCR is 1.25 or higher, you can often secure financing without the restrictive debt-to-income requirements of conventional loans. This specialized focus allows investors to scale portfolios quickly while maintaining safe debt levels.

Questions Every Investor Should Ask

Directly ask about their experience with Fix & Flip or DSCR products. You need to know how many of these specific loans they funded in the last 12 months; a track record of 50 or more deals indicates a stable operation. Inquire about the speed of funding and the specific draw schedules for renovations. Some lenders reimburse after work is completed, while others provide advances. Request a full breakdown of all origination fees, processing fees, and underwriting costs to ensure there are no hidden loan flipping triggers in the fine print.

Verifying Lender Credibility

Verify that the lender maintains a physical office and a verifiable track record of closed deals. You can check NMLS records or state licensing boards to confirm their standing. A credible lender provides “proof of funds” letters within 24 hours to help you secure properties in high-demand markets. Transparency is the hallmark of a secure partner. To get a clear view of your potential costs, Request a Quote to see a transparent term sheet that outlines every dollar involved in the transaction.

The loan term sheet is your primary defense against predatory practices. When you receive this document, analyze the interest rate, the points charged at closing, and the prepayment penalty terms. A standard term sheet should be no more than two pages and clearly state the “all-in” cost of the capital. If the lender refuses to provide a written term sheet before asking for an application fee, walk away. Professionalism in the initial stages is the best indicator of a smooth closing process and a long-term partnership.

Icon Capital’s Approach: Transparent Financing for Serious Investors

Predatory loan flipping relies on deception and equity stripping. Icon Capital LLC operates as a professional alternative for investors who prioritize transparency and long-term portfolio growth. We don’t trap clients in cycles of unnecessary refinancing. Instead, we provide the leverage needed to acquire, renovate, and hold real estate assets through high-leverage Non-QM products. Our team focuses on your success because repeat business is the foundation of our lending model.

Our focus remains on creative financing for complex scenarios that traditional banks won’t touch. Whether you’re dealing with a short-term liquidity gap or a large-scale commercial conversion, we prioritize the deal’s merit over rigid credit box requirements. We understand that serious investors need a partner who moves at the speed of the market, not the speed of a bureaucratic committee. We’ve built our reputation on being a no-nonsense facilitator for the 25% of investors who fall outside conventional lending guidelines.

Our Fix & Flip and Bridge Loan Programs

Investors requiring substantial capital can access loan amounts exceeding $2,000,000 through our specialized programs. We offer competitive LTV options, often providing up to 90% of purchase costs and 100% of renovation budgets for qualified borrowers. This high-leverage approach is designed for rapid scaling, allowing you to deploy capital across multiple projects simultaneously rather than tying it up in a single property. Our bridge options close in as little as 10 days, ensuring you never miss a time-sensitive opportunity.

- Hard Money & Bridge: Secure distressed assets before competitors by using our 10-day closing window.

- Foreign National Support: We provide financing for non-US citizens without requiring domestic credit history or Social Security numbers.

- Self-Employed Flexibility: We use 12 or 24-month bank statements rather than tax returns to verify your ability to perform.

- DSCR Loans: Scale your rental portfolio using property income to qualify, with LTVs reaching up to 80% for new purchases.

Simplifying the Loan Process for 2026

Efficiency is the primary differentiator in a competitive 2026 real estate market. We’ve stripped away the administrative bloat that defines traditional lending. Our “cash in hand” advantage ensures you have the liquidity to close on properties within a 14-day window, putting you on equal footing with institutional cash buyers. This speed allows you to negotiate better purchase prices from motivated sellers who value certainty over a slightly higher, but slower, offer.

We follow a disciplined 4-step protocol to ensure every deal stays on track:

- Structure: We define the loan terms, LTV, and interest rate within 24 hours of your initial inquiry.

- Submit: You provide the property details and basic borrower information through our secure digital portal.

- Underwrite: Our internal team completes a focused review of the asset and the exit strategy to ensure viability.

- Close: Legal documents are executed, and funds are disbursed immediately to your title company.

We avoid the pitfalls of loan flipping by being upfront about all costs from day one. There are no hidden fees or surprise charges at the closing table. Our goal is to enable your success so you can return for your next deal. If you’re ready to move past the limitations of traditional banking and predatory lenders, Explore our creative financing options today and see how we can help you scale your investment business.

Scale Your Portfolio with Professional Capital

Distinguishing between predatory loan flipping scams and legitimate investment financing is the first step toward long-term real estate success. Avoid the trap of equity-stripping refinancing by vetting your partners based on transparency and industry specialization. Investors need high-leverage tools like DSCR and Non-QM loans to maintain momentum in competitive markets. Icon Capital provides the specialized expertise required to navigate these complex structures without the delays of traditional banks. We offer loan amounts up to $2M or more, providing the liquidity needed for significant fix-and-flip or rental acquisitions. Our streamlined 4-step closing process ensures you move from application to funding with maximum efficiency. By focusing on asset-based qualifications and clear underwriting, we enable you to scale your portfolio with confidence. You’ve done the hard work of finding the deal; now it’s time to secure the financing that supports your bottom line. Get a transparent loan quote for your next flip. We’re ready to help you close your next deal quickly and securely.

Frequently Asked Questions

Is loan flipping illegal in the United States?

Loan flipping is illegal under the Home Ownership and Equity Protection Act of 1994 when it lacks a net tangible benefit for the borrower. This practice involves a lender refinancing a mortgage repeatedly to generate fees, often stripping 15% or more of the home’s equity in the process. Regulatory bodies like the FTC actively prosecute lenders who engage in these predatory cycles.

How is loan flipping different from a standard cash-out refinance?

Loan flipping differs from a cash-out refinance because it provides no financial advantage to the borrower and serves only to generate lender profit. A standard cash-out refinance typically has a 6 to 12 month seasoning requirement and a specific purpose like home improvement. In contrast, predatory flipping might see 3 refinances within 18 months, each adding 3% to 5% in closing costs.

Can I get a loan to flip a house if I am self-employed?

Self-employed investors can secure financing for a house flip through Non-QM programs that use 12 or 24 months of bank statements for income verification. You don’t need traditional tax returns if you can show consistent business deposits. Icon Capital requires a 20% down payment and a clean 12-month housing history to qualify for these specialized investment products.

What are the typical interest rates for legitimate fix and flip loans in 2026?

Legitimate fix and flip loans in 2026 carry interest rates between 8.5% and 12.5% depending on market conditions and borrower experience. High-leverage loans covering 90% of purchase costs often sit at the higher end of that range. Investors who have completed 5 successful projects in the last 24 months can often negotiate lower points and reduced origination fees.

How do I report a suspected loan flipping scam?

Report suspected scams to the Consumer Financial Protection Bureau or your state’s Attorney General’s office immediately. The CFPB tracked over 320,000 mortgage complaints in 2023 to identify patterns of predatory lending. Keep copies of all 3 or 4 loan estimates you received to prove the lender didn’t provide a net tangible benefit during the refinancing process.

Does Icon Capital offer loans for foreign national investors?

Icon Capital offers specialized loan programs for foreign national investors with LTV ratios up to 75% for residential properties. We don’t require a U.S. credit history or Social Security number for these deals. Instead, we qualify borrowers from over 50 countries based on international assets and the debt service coverage ratio of the specific investment property.

What is the minimum credit score required for a professional flip loan?

A professional flip loan typically requires a minimum credit score of 620, though a score of 720 or higher unlocks the most competitive 8.99% rates. Icon Capital looks at the total deal structure, including the 15% to 20% equity contribution and the project’s after-repair value. Lower scores may be accepted if the investor has a track record of 3 successful exits.

How quickly can a bridge loan be closed compared to a traditional mortgage?

Bridge loans close in 7 to 10 days, providing a significant speed advantage over traditional 30-day or 45-day bank financing. This rapid execution is essential for securing distressed assets in competitive markets. Icon Capital focuses on the asset’s value and the 12-month exit strategy to bypass the exhaustive paperwork that slows down conventional mortgage approvals.