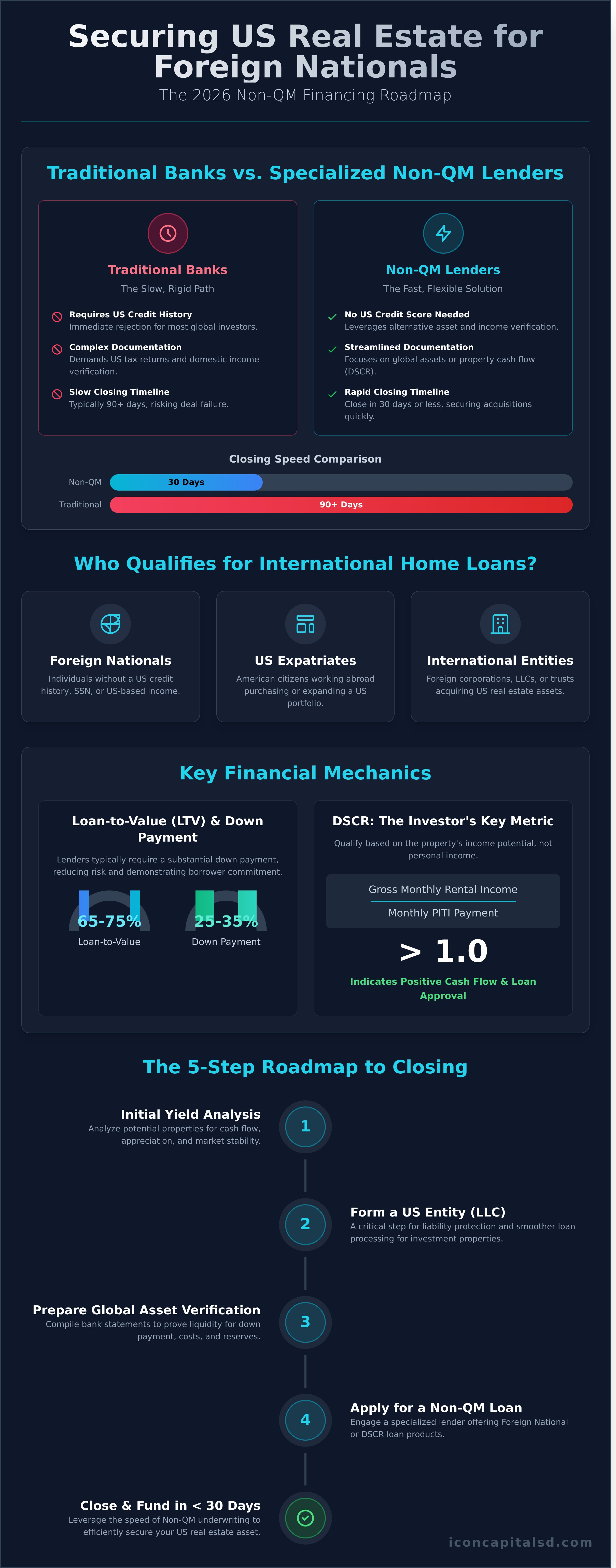

Securing US real estate financing as a foreign national is often a complex and frustrating process. Traditional lenders present significant hurdles: rigid documentation, slow underwriting, and immediate rejection for investors without a US credit history. For global investors looking to capitalize on the US market, these obstacles can halt a promising acquisition before it begins. The solution lies in moving beyond conventional financing. Specialized international home loans, specifically non-QM products, are engineered to bypass these exact challenges, providing a direct path to funding.

This guide is your strategic roadmap for 2026. We will detail how to secure high LTV financing and close on US property in 30 days or less, without the need for domestic credit. You will gain a clear understanding of the non-QM loan products available to foreign nationals, the streamlined documentation required for qualification, and the precise steps to structure a successful deal. It’s time to leverage US real estate assets with confidence and efficiency.

Key Takeaways

- Discover how foreign nationals can secure US property financing without a domestic credit score by leveraging alternative asset and income verification.

- Learn why Non-QM loans provide a significant speed advantage, reducing closing timelines to 30 days compared to the 90-day cycles of traditional banks.

- Proper entity structuring, such as forming a US-based LLC, is a critical preliminary step for successfully closing international home loans for investment purposes.

- Understand the strategic roadmap for acquiring US real estate, from initial yield analysis to establishing the necessary financial infrastructure.

Defining International Home Loans for the 2026 US Market

An international home loan is a financing instrument structured specifically for non-US citizens or non-permanent residents to purchase real estate within the United States. Unlike conventional mortgages, these loans are designed for borrowers without a US credit history, Social Security Number, or domestic income verification. While some loans cater to residential use, the market overwhelmingly focuses on investment-centric financing, enabling global investors to acquire income-producing US assets.

Entering 2026, the United States continues to be the primary “safe haven” for global real estate capital. Its stable legal framework, transparent property rights, and strong economic fundamentals offer a secure environment for asset preservation and appreciation. This perceived stability drives consistent demand from overseas investors seeking to diversify their portfolios and hedge against volatility in their home markets.

Historically, securing a US property loan as a foreign national was a complex process dominated by a few large banks with strict documentation requirements. The modern market has shifted decisively toward specialized Non-QM (Non-Qualified Mortgage) lenders. These lenders offer greater flexibility and faster execution by underwriting the loan based on the property’s income potential (like DSCR) or the borrower’s global assets. This approach streamlines the standard mortgage loan process for a global clientele, making international home loans more accessible than ever.

Who Qualifies for an International Home Loan?

Qualification criteria are designed for non-traditional borrowers and entities, including:

- Foreign Nationals: Individuals without a US credit history, Social Security Number (SSN), or US-based income.

- US Expatriates: American citizens working abroad who wish to purchase or expand a real estate portfolio in the US.

- International Entities: Foreign-based corporations, LLCs, or trusts seeking to acquire US real estate assets directly.

Primary Use Cases for Overseas Borrowers

These loans are primarily utilized for investment strategies that generate returns from the US property market. Common applications include:

- Long-Term Rental Properties: Acquiring single-family residences (SFR) and multi-unit buildings for consistent cash flow.

- Short-Term Vacation Rentals: Leveraging platforms like Airbnb and VRBO in high-demand tourist markets for higher yield potential.

- Fix-and-Flip Projects: Utilizing short-term financing to purchase, renovate, and sell properties for capital appreciation.

The Mechanics of Foreign National and DSCR Loan Programs

Traditional U.S. lending models are not designed for global real estate investors. Foreign National and DSCR loan programs operate on a different framework, prioritizing asset quality and cash flow over domestic income and credit history. Unlike the standard U.S. mortgage process, which is heavily reliant on domestic documentation, these products offer a direct path to financing for non-resident buyers. Understanding these mechanics is critical for structuring successful international home loans.

Foreign National Loan Specifics

These programs are specifically engineered for borrowers without a U.S. credit footprint. Qualification is based on a global financial profile and the strength of the subject property, making them an effective “No US Credit” solution. Underwriters evaluate risk by analyzing the borrower’s global financial standing, the property’s location, and the down payment size.

- Typical LTV Ratios: For 2026, we anticipate typical Loan-to-Value (LTV) ratios for non-residents to range from 65% to 75%. This requires a substantial down payment, generally 25-35%, which demonstrates borrower commitment and reduces lender risk.

- Asset Verification Requirements: Lenders require proof of sufficient global liquidity to cover the down payment, closing costs, and several months of reserves. This is verified through bank statements from U.S. or international financial institutions.

Leveraging DSCR for International Portfolios

For investment properties, the Debt Service Coverage Ratio (DSCR) loan is a powerful tool. It qualifies the borrower based on the property’s income-generating potential, not personal income. This focus on cash flow is a key advantage for international home loans aimed at portfolio growth.

- Calculating DSCR: The formula is direct: Gross Monthly Rental Income / Monthly PITI (Principal, Interest, Taxes, Insurance). A ratio above 1.0 indicates positive cash flow, with most lenders requiring 1.25 or higher for qualification.

- Why International Borrowers Prefer DSCR: The primary appeal is that DSCR loans do not require U.S. tax returns or employment verification. The property qualifies itself, streamlining the process for investors whose income is generated abroad.

- Closing in a U.S. Entity: Many global investors choose to close in the name of a U.S.-based LLC or corporation. This strategy can offer significant liability protection and potential tax efficiencies, separating personal assets from investment properties.

Traditional vs. Creative Financing: Why Non-QM Wins

Traditional U.S. banks operate within a rigid framework, often struggling to underwrite foreign nationals. Their reliance on conventional income verification-W-2s, U.S. tax returns, and domestic credit histories-creates significant “red tape” for global investors. This system is ill-equipped to evaluate complex international income streams or assets held abroad, a limitation heavily influenced by strict GSE guidelines for non-citizen borrowers. The result is a slow, frustrating process that frequently ends in denial.

Non-Qualified Mortgage (Non-QM) lenders bypass these obstacles. Where a major bank may take 90 days or more to process an application, a specialized Non-QM lender can often close in 30 days. This speed is a critical competitive advantage in active real estate markets. Furthermore, Non-QM financing offers superior flexibility in asset selection, providing capital for properties that fall outside traditional lending boxes, from non-warrantable condos to 5-8 unit multi-family buildings.

Investors must weigh the cost of capital against the cost of a missed opportunity. While Non-QM rates may be higher than conventional loans, this premium secures speed and certainty. In a competitive bidding situation, the ability to close quickly is often the deciding factor, making Non-QM a strategic investment rather than a mere expense.

Evaluating the Non-QM Advantage

Our specialized international home loans leverage creative structures designed for global investors:

- Minimal Documentation (Low-Doc): Pathways for high-net-worth individuals using asset depletion or bank statement analysis to qualify, avoiding the need for traditional income proof.

- Interest-Only Options: Loan structures that require payment only on the interest for a set term, maximizing monthly cash flow on investment properties.

- Bridge Loans: Short-term financing to facilitate rapid acquisitions, allowing investors to secure a property now and arrange permanent financing later.

The 2026 Interest Rate Environment for Global Capital

Currently, the spread between domestic and international loan rates typically ranges from 1.5% to 3%, reflecting the perceived risk and complexity. To mitigate currency risk when financing in USD, investors should consider holding USD-denominated assets or utilizing forward contracts to hedge against exchange rate fluctuations. The 2026 LTV landscape for foreign nationals is projected to see maximum leverage stabilize at 70-75% for well-qualified borrowers on prime U.S. assets.

The 2026 Roadmap to Closing an International Home Loan

Securing a U.S. property investment requires a structured, methodical approach. The process for international home loans is distinct from conventional financing, emphasizing asset verification, legal structure, and logistical coordination. Following a clear roadmap ensures efficiency and mitigates delays in a cross-border transaction. This five-step framework outlines the critical path from property selection to closing.

- Property Identification and Yield Analysis: The process begins with identifying a target property. For investors, this includes a thorough analysis of its potential yield, calculating metrics like Debt Service Coverage Ratio (DSCR) and potential cash-on-cash return.

- Entity Formation and U.S. Bank Account: Many foreign nationals choose to purchase property through a U.S.-based Limited Liability Company (LLC) for asset protection and tax advantages. Establishing an LLC and a corresponding U.S. bank account is a foundational step for holding the asset and managing funds.

- Document Submission: Lenders require specific documentation to verify identity and financial capacity. This stage involves gathering and submitting all required paperwork for pre-approval and underwriting.

- Underwriting and Appraisal: The lender’s underwriting team will review the complete loan file to assess risk and ensure compliance. Concurrently, a third-party appraiser is engaged to determine the property’s fair market value according to U.S. standards.

- Escrow and Global Closing Logistics: A neutral third-party escrow or title company manages the final stage. They handle the secure transfer of funds and legal documents, coordinating with all parties to facilitate a remote closing from anywhere in the world.

Required Documentation Checklist

While requirements vary by lender and loan program, a standard package for foreign national borrowers includes several key items. Assembling these documents early in the process is critical for a streamlined approval.

- A clear, valid copy of your passport and a U.S. visa (if applicable, such as a B-1/B-2).

- Verifiable proof of funds for the down payment, typically 25-35% of the purchase price for most international home loans.

- Reference letters from your international banking or financial institutions confirming your good standing.

- Every loan scenario is unique. Request a Quote to receive a personalized list and verify your specific document needs.

Navigating the Appraisal and Inspection

The U.S. property appraisal is a strictly regulated process based on comparable recent sales (“comps”) and is fundamentally different from valuation methods in other countries. It provides an objective market value for the lender. For remote owners, engaging a reputable local property management company post-inspection is crucial for asset maintenance and tenant relations. For coastal properties, inspections should specifically address potential issues like flood zone compliance, storm-readiness, and saltwater corrosion on structural components.

Icon Capital: Specialized Solutions for Global Real Estate

Navigating the U.S. real estate market requires a lending partner with specific expertise in structuring complex deals for foreign nationals. At Icon Capital LLC, we specialize in creative financing solutions tailored to global investors. Our focus is on high-value acquisitions, with proven expertise in loan amounts exceeding $2 million. We bypass conventional lending constraints, providing direct access and decisive action for investors with sophisticated income profiles and ambitious portfolio goals.

For brokers and realtors, our process integrates seamlessly into your workflow, providing your international clients with the reliable, efficient financing they need to close. We understand the unique documentation and verification challenges associated with international home loans and have built our systems to solve for them.

The Icon Capital LLC Process

Our model is built on efficiency and direct access. We eliminate the friction of automated portals and lengthy communication chains. When you work with Icon Capital LLC, you communicate directly with decision-makers. This direct-to-underwriter approach accelerates timelines and provides clear, actionable feedback. Key advantages include:

- Aggressive LTVs: We offer competitive loan-to-value ratios for qualified foreign national investors, maximizing leverage on prime U.S. assets.

- Diverse Asset Experience: Our expertise extends beyond single-family residences to include more complex properties, such as 5-8 unit multi-family buildings.

- Direct Underwriter Access: Get definitive answers quickly, without intermediaries, to structure your deal with confidence.

Ready to Scale Your US Portfolio?

Securing your first U.S. property is a significant step; scaling your portfolio requires a strategic, long-term lending partner. At Icon Capital LLC, we provide the consistent and creative financing necessary for sustained growth. The pre-qualification process is straightforward, designed to give you a clear understanding of your purchasing power and loan options. A reliable U.S. lending partner is the key to executing your investment strategy effectively.

Structure your next international deal with a team that specializes in your unique requirements. Request a Quote today to begin the process.

Finalize Your US Real Estate Strategy

As we look toward 2026, the US real estate market presents a prime opportunity for global investors. The key to unlocking this potential lies not in traditional financing, but in strategic Non-QM solutions like Foreign National and DSCR loan programs. These instruments are specifically designed to evaluate international assets and income, making US property acquisition a streamlined, data-driven process for those who qualify.

Navigating the complexities of international home loans requires a partner with specialized expertise. Icon Capital provides direct access to creative financing engineered for the sophisticated global investor. Our specialized Foreign National programs require no US credit history, and we structure loan amounts exceeding $2M for high-value investment properties. With deep expertise in DSCR and Non-QM lending, we underwrite complex global profiles with efficiency and precision.

Take the definitive next step to leverage your global assets. Request a Professional Loan Quote to structure your financing with an industry expert. Your next high-value US property is within reach.

Frequently Asked Questions About International Home Loans

Can a non-US citizen get a mortgage in the USA in 2026?

Yes, a non-US citizen can secure a mortgage in the United States. The ability to obtain financing is not determined by a specific year but by the borrower’s ability to meet lender requirements. Key factors include possessing a valid visa, providing verifiable international income and asset documentation, and having sufficient funds for a down payment. Lenders specializing in foreign national loans are equipped to handle these specific underwriting needs.

Do I need a US credit score for an international home loan?

A US credit score is not a mandatory requirement for all international home loans. Lenders who specialize in financing for foreign nationals can utilize alternative credit verification methods. This may include a comprehensive credit report from your country of residence or official reference letters from your current financial institutions. The objective is to demonstrate a consistent and reliable history of meeting your financial obligations, regardless of origin.

What is the typical down payment for a foreign national loan?

The down payment for a foreign national loan is typically higher than for a domestic mortgage, generally ranging from 20% to 40% of the purchase price. The exact percentage, or loan-to-value (LTV), is determined by factors such as the property type, loan amount, and the borrower’s overall financial profile. Investment properties or unique property types may require a larger down payment to mitigate lender risk.

Can I use a DSCR loan if I do not live in the United States?

Yes, foreign national investors can effectively use a Debt Service Coverage Ratio (DSCR) loan to purchase US investment properties. This loan product qualifies the borrower based on the property’s rental income potential rather than personal income. Because it does not require verification of foreign employment or income, the DSCR loan is an efficient financing vehicle for non-resident investors seeking to build a US real estate portfolio.

What documents are required for an international mortgage?

Standard documentation for an international mortgage includes a valid passport and US visa, proof of income from your home country (such as tax returns or employment letters), and bank statements verifying funds for the down payment and reserves. You will also need the signed purchase contract for the property. Providing a complete and well-organized document package is critical for an efficient underwriting process for all international home loans.

How long does it take to close a foreign national loan?

The closing timeline for a foreign national loan typically ranges from 30 to 60 days. This process can be longer than for a domestic loan due to the complexities of verifying international income, assets, and credit. The efficiency of the closing is heavily dependent on the borrower’s responsiveness and the completeness of the initial application package. A proactive approach can help expedite the underwriting and funding stages.

Can I buy a US property through an LLC as a foreign national?

Yes, purchasing property through a U.S.-based Limited Liability Company (LLC) is a common and permissible strategy for foreign nationals. This structure can provide significant liability protection and potential tax advantages. Lenders with expertise in foreign national financing are proficient in underwriting loans to an LLC owned by non-resident borrowers, though personal documentation from the LLC members will still be required for qualification.

Are international home loan rates higher than domestic rates?

Interest rates for international home loans are typically higher than rates for conventional loans available to US residents. This rate differential accounts for the increased perceived risk associated with cross-border lending, including complexities in credit verification and international legal jurisdiction. The final interest rate is determined by the specific loan product, loan-to-value (LTV) ratio, and the overall strength of the borrower’s financial profile.