A lack of a U.S. credit score shouldn’t prevent you from leveraging the 2026 Florida real estate market. International buyers accounted for 23% of Florida’s residential sales volume according to 2023 industry reports, yet many investors remain sidelined by the perceived barriers of domestic lending. Securing a foreign national mortgage florida requires a specialized approach that bypasses traditional FICO requirements. Standard institutional lenders often struggle with international wire seasoning and non-resident documentation, creating friction that stalls high-value deals and prevents portfolio scaling.

Icon Capital provides the technical expertise to manage these hurdles. This guide provides the framework to master the complexities of securing U.S. real estate financing as a non-resident. We’ll examine specific LTV thresholds for non-QM products and the legalities of U.S. closing costs. You’ll learn how to structure your assets to meet underwriter expectations without a domestic credit history. We’ve mapped out the 2026 landscape to ensure your capital moves efficiently from your home country into Florida’s most lucrative investment properties.

Key Takeaways

- Understand how non-U.S. citizens can secure property financing without a Social Security Number or established domestic credit score.

- Identify the specific documentation and LTV requirements needed to qualify for a foreign national mortgage florida in today’s market.

- Evaluate the advantages of DSCR-based financing to determine if property-based income qualification is more effective for your investment goals.

- Follow a structured five-step roadmap designed to streamline everything from initial loan structuring to final submission.

- Leverage specialized Non-QM expertise to navigate international financial profiles that traditional banks often overlook.

What is a Foreign National Mortgage in Florida?

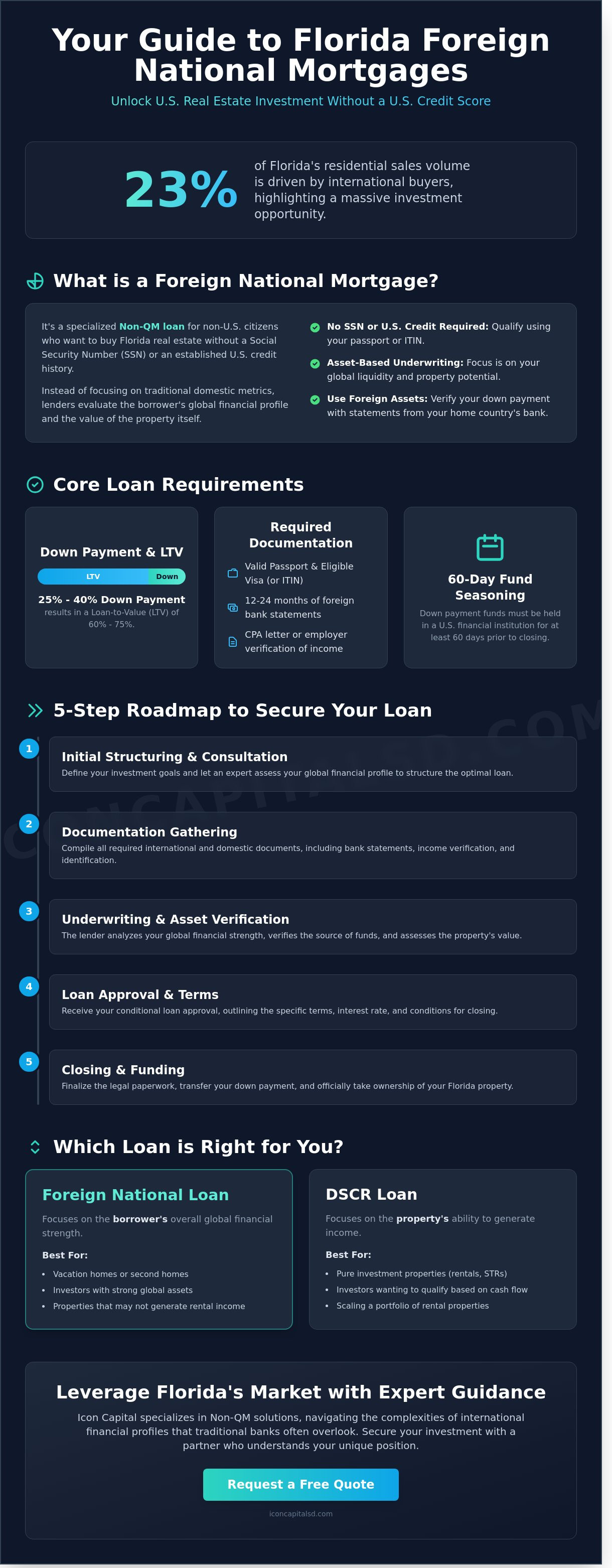

A foreign national mortgage florida is a specialized Non-QM loan product designed for non-US citizens who want to acquire real estate without a Social Security Number (SSN) or a domestic credit history. These programs prioritize the value of the asset and the borrower’s global financial profile over traditional US-based metrics. In 2026, Florida continues to dominate the international investment sector, accounting for 23% of all foreign buyer transactions in the United States according to recent market data. This financing allows investors to leverage capital for rental income properties, vacation homes, and high-value luxury estates.

The primary distinction of this loan type is the underwriting flexibility. To understand the baseline requirements, investors often ask What is a Foreign National Mortgage? and how it facilitates entry into the US market. These loans typically require a down payment between 25% and 35%, depending on the LTV (Loan-to-Value) ratio and the property type. Because lenders don’t require a US credit score, they often utilize international credit reports or bank references to establish creditworthiness. This makes it a pragmatic solution for global investors looking to diversify their portfolios into US hard assets.

Florida’s Global Appeal: Miami, Orlando, and Beyond

Florida remains the primary gateway for international capital. Miami attracts 54% of the state’s foreign investment, acting as a financial bridge for LATAM and European wealth. Orlando provides a high-yield environment for short-term rental (STR) investors, driven by a tourism sector that saw 140 million visitors in the previous fiscal year. Florida’s tax-friendly structure, specifically the absence of state income tax, significantly improves the net ROI for foreign entities. Investors can request a quote to analyze how these tax advantages impact specific property yields.

Eligible Visa Types and Residency Status

Lending eligibility in 2026 is broad, covering various residency statuses and visa categories. Financeable visas include B-1 and B-2 for business and tourism, H-2 and H-3 for specialized work, and J-1 or J-2 for exchange visitors. Canadian citizens and residents from “visa-waiver” countries enjoy even more streamlined qualification paths. The ITIN (Individual Taxpayer Identification Number) plays a critical role in the current lending landscape, allowing non-residents to fulfill tax obligations and build a recognizable financial identity within the US mortgage system without needing a green card or permanent residency.

- No SSN Required: Qualification is based on ITIN or foreign passport.

- Asset-Based Underwriting: Focus on the property’s DSCR (Debt Service Coverage Ratio) or personal liquidity.

- Flexible Property Types: Includes condos, condotels, and multi-family units.

- Global Capital Integration: Ability to use foreign bank statements for down payment verification.

Foreign National Loan Requirements and Documentation

Securing a foreign national mortgage florida requires a shift from standard domestic underwriting toward a focus on global liquidity and asset verification. Lenders typically offer Loan-to-Value (LTV) ratios between 60% and 75% for most Florida residential and commercial projects. This higher equity requirement, often a 25% to 40% down payment, mitigates the risk associated with borrowers who lack a domestic credit footprint. Asset qualification allows investors to leverage global liquidity, effectively converting non-US holdings into qualifying collateral for US-based financing.

The seasoning requirement is a critical timeline for any international investor to track. Lenders generally require down payment funds to be seasoned in a US-based financial institution for 60 days before the loan closing. This period allows for the verification of the source of funds and compliance with anti-money laundering protocols. If an investor lacks a US credit score, lenders utilize alternative credit verification. This involves collecting 12 months of payment history from international bank references, utility companies, or specialized international credit reporting agencies.

The Alternative Documentation Framework

Underwriting for foreign nationals relies on a specialized documentation set. Primary proof of income is established through CPA letters or international employer verification forms that detail the last two years of earnings. Lenders require 12 to 24 months of bank statement history from the borrower’s home country to establish financial stability and consistent cash flow. Asset Utilization is a method for high-net-worth foreign nationals to qualify by using a formulaic portion of their total liquid assets as a substitute for traditional monthly income.

Reserve Requirements and Liquidity

Post-closing liquidity is a mandatory component of the approval process. Borrowers should prepare to show 6 to 12 months of PITI (Principal, Interest, Taxes, and Insurance) in a liquid account. These reserves act as a safety net for the lender, ensuring the debt service is covered regardless of vacancy or currency fluctuations. Accepted forms of reserves include cash, publicly traded stocks, and international brokerage accounts, provided they can be liquidated and transferred if necessary.

Data regarding foreign investment trends indicates that Florida remains the primary destination for international capital, capturing 23% of all foreign buyer transactions in the United States. For a deeper look at specific eligibility criteria, see the Foreign National Loans guide. If you have a specific property in mind, you can request a quote to see how these LTV and reserve requirements apply to your scenario.

Foreign National vs. DSCR Loans: Which is Best for Investors?

Investors securing a foreign national mortgage florida often face a choice between traditional income-based lending and Debt Service Coverage Ratio (DSCR) structures. Traditional loans require proof of global personal income, which often entails translating multi-year tax returns and bank statements from the borrower’s home country. DSCR loans bypass this entirely. They qualify the borrower based solely on the property’s ability to generate enough rental income to cover the monthly debt obligations.

The Power of DSCR for Non-Residents

For international business owners, DSCR is the most efficient path to closing. It eliminates the need for complex personal financial disclosures that often stall traditional applications. If the property’s gross rent exceeds the principal, interest, taxes, insurance, and HOA fees (PITIA), the deal is viable. Most lenders look for a ratio of 1.0 or higher. You can request a quote to see how your target property’s specific cash flow affects your leverage. This structure is particularly useful because U.S. regulations for foreign buyers remain focused on transparency, and DSCR provides a clear, asset-centric transaction model that satisfies modern compliance standards.

Loan Terms and Flexibility

Florida investors typically choose between 30-year fixed rates and Adjustable Rate Mortgages (ARMs). A 30-year fixed loan provides long-term protection against interest rate volatility. Conversely, 5/1 or 7/1 ARMs often offer lower initial interest rates. These are ideal for investors planning to sell or refinance within a five to seven year window. Interest-only payment options are also available to maximize monthly cash flow during the initial years of the investment. Be aware of prepayment penalties, which typically range from one to five years. These penalties are a standard trade-off for the flexible qualification requirements of a foreign national mortgage florida.

Scaling a portfolio becomes significantly faster with DSCR. Since the lender doesn’t calculate your personal debt-to-income (DTI) ratio, you aren’t limited by your personal salary or international tax liabilities. You can acquire multiple properties simultaneously as long as each asset’s rental income supports its own debt. This allows non-residents to build significant Florida real estate holdings without the friction of traditional mortgage underwriting. Key benefits of this approach include:

- No Personal Income Verification: No need for pay stubs or employer letters.

- Rapid Approval: Processing times are often 15 to 20 days faster than traditional routes.

- Unlimited Properties: No cap on the number of financed properties for qualified investors.

5 Steps to Securing a Florida Foreign National Mortgage

Securing a foreign national mortgage florida requires a methodical approach to satisfy both US lending regulations and international compliance. The process moves from initial structuring to final funding through five distinct phases.

- Initial Consultation: We analyze your investment goals and liquidity. This stage determines if a DSCR or asset-based program fits your profile.

- Application Submission: You provide a complete documentation package. This includes your passport, visa (if applicable), and two months of bank statements.

- The Appraisal: We assess the Florida property value. In the 2026 market, appraisals focus on current market data and projected rental yields to ensure the asset supports the debt.

- Underwriting: Our team clears international verification hurdles. This involves validating the source of funds and ensuring the deal meets all Non-QM guidelines.

- Closing: The Title Company facilitates the transfer of deed. You receive final settlement statements and execute the loan documents.

Structuring the Deal for Success

Optimization starts with the Loan-to-Value (LTV) ratio. Most investors target a 65% to 75% LTV. This range balances your cash-on-cash return with more competitive interest rates. You must also decide on the holding entity. While individual ownership is simpler, many international investors use a US-based LLC to shield personal assets and optimize tax efficiency. Request a quote to see your customized terms and explore which structure fits your 2026 portfolio goals.

The Closing Process for International Buyers

You don’t need to be physically present in Florida to close. Remote closing options are standard. You can use a Power of Attorney (POA) or visit a US Embassy for document notarization. Be aware of the Foreign Investment in Real Property Tax Act (FIRPTA) implications. This law requires 15% of the gross sales price to be withheld at the time of a future sale if the seller is a foreign person. Final wire transfers must comply with international banking regulations. Ensure your bank can facilitate large USD transfers to a US escrow account at least 48 hours before the closing date. This ensures your foreign national mortgage florida funds are available for the final settlement without delay.

Why Icon Capital is the Preferred Choice for Florida International Loans

Traditional Florida banks often operate within narrow parameters that exclude international investors. They rely on standard US credit scores and domestic tax returns. Icon Capital specializes in the Non-QM space; we provide creative financing solutions that these institutions lack. Our team understands that global wealth doesn’t always fit into a standard 1040 form. We focus on the strength of the asset and the borrower’s global financial profile to secure a foreign national mortgage florida.

We provide direct access to underwriters who are trained to analyze international documentation. This eliminates the bureaucratic layers found at retail banks. Our product suite is designed for versatility. We offer Debt Service Coverage Ratio (DSCR) loans that qualify properties based on rental income rather than personal debt-to-income ratios. For investors focused on renovation, we provide Fix and Flip loans tailored for the Florida market. This flexibility allows us to structure deals that other lenders simply cannot approve.

The Icon Capital Advantage: Speed and Scale

Speed is a critical factor in the 2026 Florida real estate market. Average property listing times in high-demand areas like Tampa and Orlando remain tight, with many properties moving in approximately 14 to 18 days. Traditional retail banks often take 45 to 60 days to close an international loan. Icon Capital streamlines this process. We frequently close deals in 21 to 30 days. This efficiency is vital for securing competitive properties before other buyers can react.

Our underwriting team looks for ways to say yes. We handle complex deals that require outside the box thinking, such as using foreign assets as collateral or verifying income through international business bank statements. If you’re looking to expand a high-velocity portfolio, see how we handle flipping houses with hard money to understand our approach to rapid-growth strategies and leverage.

Expert Support for Every Florida Region

We translate complex industry jargon into actionable data. Whether you’re navigating LTV requirements or understanding the impact of 2026 interest rate shifts, our team provides the clarity you need. We act as a serious financial partner for those who value results over descriptive prose. To secure your next investment, Contact Icon Capital today to explore your financing options.

Maximize Your Investment Potential in Florida’s High-Growth Markets

Florida remains a primary destination for international capital, offering significant appreciation potential in 2026 across markets like Miami, Orlando, and Tampa. Navigating the requirements for a foreign national mortgage florida doesn’t have to be a bottleneck for your portfolio growth. Success in this competitive landscape depends on selecting a financing partner that understands Non-QM structures and the specific needs of international investors who don’t have a domestic credit history.

Icon Capital specializes in the mechanics of complex deals. We provide funding up to $2M+ for international investors, utilizing specialized DSCR and Non-QM underwriting to move your application through the pipeline quickly. Our approach focuses on the asset’s performance and your global financial strength rather than traditional domestic benchmarks. We’ve built our reputation on providing the creative financing solutions necessary to compete in Florida’s fast-moving real estate landscape.

Frequently Asked Questions

Can a foreign national get a mortgage in Florida without a US credit score?

Yes, you can secure a foreign national mortgage florida without a US credit history. Lenders utilize non-traditional credit data like international credit reports or reference letters from financial institutions in your home country. Most programs require three alternative credit references to establish your repayment history. This allows investors to bypass the lack of a FICO score while maintaining professional underwriting standards.

What is the typical down payment for a foreign national loan in Florida?

Expect to provide a down payment between 25% and 35% of the purchase price. Most lenders cap the loan-to-value ratio at 70% or 75% for non-resident borrowers. This higher equity requirement mitigates risk for the lender. You must also show 12 months of cash reserves in a verified bank account to cover mortgage payments; property taxes; and insurance costs.

Do I need a green card or SSN to buy investment property in Florida?

You don’t need a green card or a Social Security Number to acquire investment real estate. Investors typically use a valid passport and a B-1 or B-2 visa for the transaction. If you’re generating income, you’ll eventually need an Individual Taxpayer Identification Number for tax filings. IRS Form W-7 facilitates this process for non-resident aliens who are ineligible for a standard Social Security Number.

Can I use rental income from the property to qualify for the loan?

DSCR loan programs allow you to qualify based on the property’s projected rental income rather than personal earnings. The lender calculates a Debt Service Coverage Ratio to ensure the rent covers the monthly debt obligation. A ratio of 1.0 or higher is the standard requirement. This product is a core component of the foreign national mortgage florida market because it simplifies the qualification process for international investors.

How long does it take to close a foreign national mortgage in 2026?

A typical closing timeframe ranges from 30 to 45 days. While traditional loans might move faster, the documentation for international assets and identity verification adds complexity. Non-QM lenders have streamlined these workflows to ensure most deals reach the funding stage within five weeks. Efficiently providing translated bank statements and proof of assets can reduce this timeline by 5 to 7 days.

What are the current interest rates for foreign national mortgages in Florida?

Interest rates for foreign national products generally sit 1% to 3% above standard conventional rates. Industry benchmarks from 2024 show that non-resident loans remained in a higher tier due to the increased risk profile. These are typically structured as 5/1 or 7/1 Adjustable Rate Mortgages. Fixed-rate options are available but often carry a premium of 0.5% over ARM products in the current market.

Can I close on a Florida property remotely from my home country?

Remote closings are standard practice through Remote Online Notarization or mobile notary services at US embassies. Florida House Bill 409, which took effect in 2020, legalized these digital transactions. You can sign all necessary loan documents electronically from your home country. This eliminates the need for international travel; it makes the investment process efficient and geographically flexible for global buyers who cannot visit Florida.

Are there any specific taxes for foreign nationals selling Florida real estate?

The Foreign Investment in Real Estate Tax Act requires a specific withholding during the sale. The IRS mandates that the buyer withholds 15% of the gross sales price to ensure tax compliance. This isn’t a final tax; it’s a credit toward your total US tax liability. You can apply for a withholding certificate to reduce this amount if your actual tax bill is significantly lower than the 15% threshold.