In the competitive real estate market, securing the right fix and flip financing is as critical as finding the right property. A profitable deal can be lost to slow funding or a poorly structured loan, and navigating the landscape of hard money, private lenders, and conventional options presents a significant challenge. For investors, deciphering the differences between LTV, LTC, and ARV to determine the best path forward can be a complex and time-consuming process.

This guide provides a complete comparison of your funding options. We will analyze the leading loan types to eliminate confusion and empower your investment strategy. You will gain a clear, side-by-side breakdown of the qualification criteria, speed, and cost structures for each solution. The objective is to equip you with the critical data needed to select the most profitable financing structure for your next project, allowing you to secure capital quickly and close with confidence.

Key Takeaways

- Compare the core types of fix and flip financing-from hard money to conventional loans-to find the optimal balance of speed and cost for your deal.

- Master the key metrics lenders use to evaluate a deal’s profitability, significantly increasing your chances of loan approval.

- Discover what lenders assess in both the borrower and the property to strengthen your loan application and mitigate perceived risk.

- Align your financing strategy with your experience level to effectively manage risk as a new investor or leverage capital as you scale.

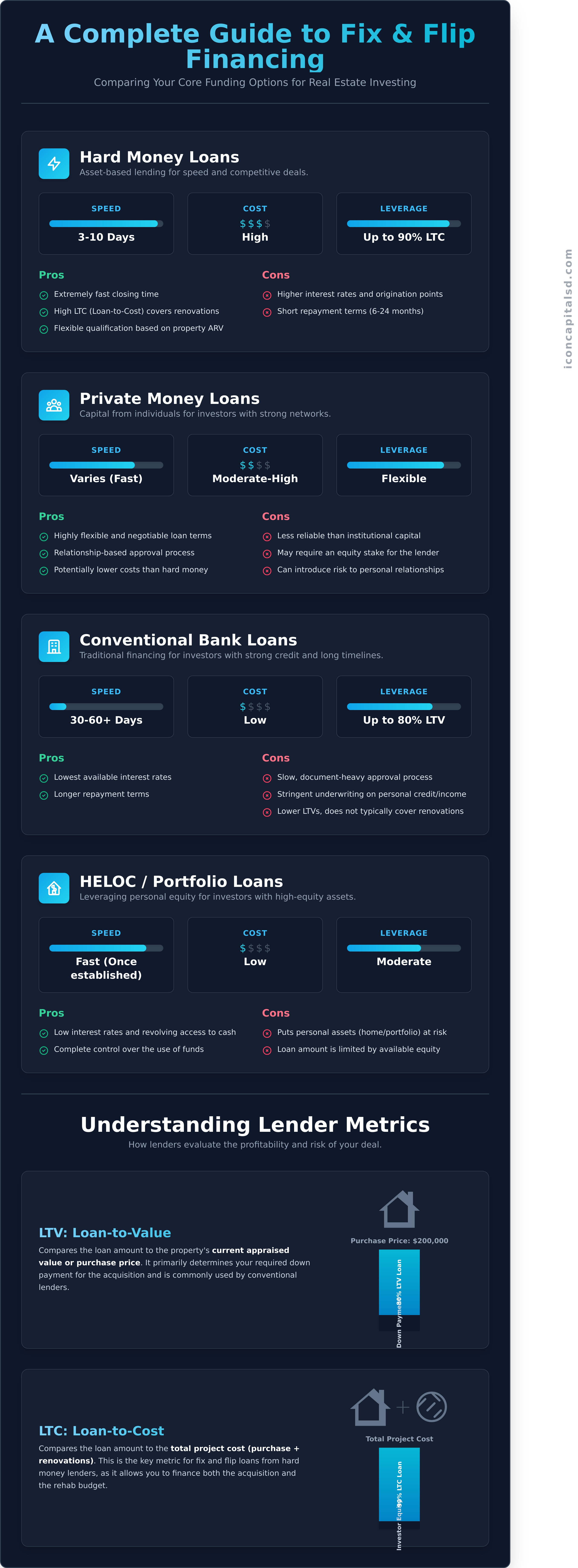

Core Fix and Flip Financing Options: A Head-to-Head Comparison

Executing a successful property flip requires access to the right capital. The world of fix and flip financing is comprised of four primary sources: hard money lenders, private individuals, conventional banks, and leveraging personal equity. The practice of flipping real estate often hinges on speed, making the choice of financing a critical decision. The optimal solution depends on the deal’s velocity, cost structure, and your financial position. Sophisticated investors frequently combine these options to structure the most advantageous deal.

The following table provides a high-level overview of these core options.

| Financing Type | Speed | Cost | Leverage (LTV/LTC) | Best For |

|---|---|---|---|---|

| Hard Money Loan | Very Fast (3-10 days) | High | High (Up to 90% LTC) | Speed & Competitive Deals |

| Private Money Loan | Fast (Varies) | Moderate-High | Flexible (Negotiated) | Strong Personal Networks |

| Conventional Loan | Slow (30-60+ days) | Low | Low (Up to 80% LTV) | Long Timelines & Strong Credit |

| HELOC / Portfolio Loan | Fast (Once established) | Low | Moderate (Based on equity) | Investors with High Equity |

Hard Money Loans

Hard money loans are short-term, asset-based loans from private lenders or funds. Underwriting focuses primarily on the property’s after-repair value (ARV), not the borrower’s personal credit score. Pros: Extremely fast closing, high loan-to-cost (LTC) ratios that can cover purchase and renovation, and flexible qualification. Cons: Higher interest rates and origination points, with short terms of 6-24 months. Best for: Investors who need to secure a competitive deal quickly.

Private Money Loans

This capital is sourced from individuals in your network, such as friends, family, or other investors. The loan structure is entirely negotiable between the borrower and the lender. Pros: Highly flexible terms, relationship-based approval process, and potentially lower costs than hard money. Cons: Can be less reliable than institutional capital, may require an equity stake, and introduces risk to personal relationships. Best for: Borrowers with a strong, trusted network.

Conventional Bank Loans & Lines of Credit

This is traditional financing from depository institutions like banks or credit unions. It is the most difficult type of financing to secure for a fix and flip project due to strict regulations. Pros: The lowest available interest rates and longer repayment terms. Cons: A slow, document-heavy approval process, stringent underwriting on personal income and credit, and lower LTVs. Best for: Experienced investors with excellent financials and no time pressure.

Home Equity Line of Credit (HELOC) or Portfolio Loans

A HELOC allows you to borrow against the equity in your primary residence, while a portfolio loan lets you leverage equity across multiple investment properties. Pros: Low interest rates, revolving access to cash, and complete control over the use of funds. Cons: Puts your personal assets directly at risk and the loan amount is limited by your available equity. Best for: Investors with significant home equity who are comfortable with the risk.

Understanding the Numbers: Key Metrics Lenders Use

To secure fix and flip financing, investors must understand that lenders evaluate the deal itself, not just the borrower. They use a specific set of financial metrics to assess a project’s viability and mitigate their risk. Mastering these formulas is critical for getting your loan application approved, as they directly determine how much capital you can borrow for both the property purchase and the required renovations.

Loan-to-Value (LTV)

The LTV ratio compares the requested loan amount to the current appraised value or purchase price of the property, whichever is lower. This metric is primarily used to calculate the down payment required for the acquisition. For example, if a property costs $200,000 and the lender offers a maximum of 80% LTV, your loan for the purchase would be capped at $160,000, requiring a $40,000 down payment from you.

Loan-to-Cost (LTC)

The LTC ratio is essential for fix and flip projects because it includes renovation funds. It measures the total loan amount against the total project cost (purchase price + rehab budget). A lender might offer to finance 90% of the purchase and 100% of the rehab costs, but they will often cap the entire loan at a maximum LTC. For instance, if your total project cost is $250,000, a 90% LTC cap means the maximum loan you can receive is $225,000.

After-Repair-Value (ARV)

ARV is the estimated market value of the property after all proposed renovations are successfully completed. Lenders use the ARV as a final guardrail, typically limiting the total loan amount to a percentage of this future value, such as 70% or 75%. This is a fundamental component of most fix and flip loans because it ensures the project is profitable enough to cover the loan and generate a return. A strong, well-supported ARV is key to demonstrating the deal’s potential.

These three metrics-LTV, LTC, and ARV-work together to define the parameters of your loan. At Icon Capital LLC, our expertise lies in analyzing these numbers to structure a deal that meets lender requirements, positions your project for approval, and maximizes your financial leverage.

How to Qualify: What Lenders Look for in a Borrower and a Deal

Lenders mitigate risk by assessing three pillars: the borrower, the property, and the deal’s financial viability. While many forms of fix and flip financing, such as a Hard money loan, are primarily asset-based, the borrower’s strength remains a critical factor. Preparing your documentation across these areas ensures a streamlined approval process. At Icon Capital, we guide investors through these requirements to structure a loan that aligns with their project goals.

The Borrower Profile

Lenders need confidence in the person managing the project. Your profile demonstrates your ability to execute the plan and handle unforeseen challenges. Key metrics include:

- Credit Score: While private lenders offer more flexibility than banks, a score above 660 typically secures more favorable terms and higher leverage.

- Experience: Documenting the number of successful flips you have completed, especially within the last 24-36 months, builds significant credibility.

- Liquidity: Lenders will verify you have sufficient cash reserves for the down payment, closing costs, and several months of interest payments.

The Property and Project Plan

The asset itself is the core of the deal. Lenders scrutinize the property’s potential and your plan to realize it. A comprehensive package includes:

- Property Type: Non-owner occupied single-family residences (SFRs) and 2-4 unit properties are the most common and easiest to finance.

- Scope of Work (SOW): A detailed renovation plan with a line-item budget and realistic timeline is non-negotiable for securing rehab funds.

- Appraisal & Inspection: An independent, third-party appraisal establishes the property’s current (“as-is”) value and After Repair Value (ARV).

The Financials of the Deal

Ultimately, the investment must be profitable. Lenders analyze the numbers to ensure the project is financially sound and has a high probability of success. Be prepared to present:

- Purchase Price & Rehab Budget: These figures must be realistic and supported by contractor bids and local market data.

- Profit Potential: The projected ARV must provide a healthy profit margin after accounting for all costs, including acquisition, rehab, and financing.

- Exit Strategy: A clear plan to either sell the property upon completion or refinance into a long-term rental loan is essential.

A well-structured deal with strong supporting documentation is the fastest path to securing fix and flip financing. Understanding these lender requirements allows you to present your project with confidence. See if your deal qualifies with Icon Capital.

Matching the Financing to Your Investor Profile

The optimal fix and flip financing strategy is not static; it evolves directly with your experience, capital, and deal volume. A beginner’s priority is securing reliable funding and managing risk, while a seasoned professional focuses on leveraging their track record to access cheaper, more flexible capital for scaling. Understanding where you are in your investment journey is critical to selecting the right financial tool for the job.

For the First-Time Flipper

For your initial projects, the primary objective is successful execution, not securing the absolute lowest rate. Your lack of a track record means traditional lenders are often not an option.

- Recommended Options: Hard money loans or private money loans.

- Why It Works: These lenders focus on the quality of the asset and its After Repair Value (ARV). The underwriting is based on the deal’s potential, making them accessible to new investors. Their speed is also a major competitive advantage in a hot market.

- Key Consideration: Prioritize a reliable lender with a history of closing on time. A failed funding attempt is far more costly than slightly higher interest or points.

For the Intermediate Investor (2-5 flips)

With a few successful projects completed, you now have a verifiable track record. This history is a valuable asset that can be leveraged to improve your financing terms and operational flexibility.

- Recommended Options: Build relationships with multiple hard money lenders; utilize a HELOC.

- Why It Works: Lenders will compete for your business, allowing you to negotiate better terms like lower rates and fewer points. A Home Equity Line of Credit (HELOC) can also be an excellent tool for covering down payments or smaller renovation budgets.

For the Seasoned Pro (5+ flips per year)

At this stage, your focus shifts from single-deal financing to building a scalable capital machine. Efficiency and cost of funds are paramount to support high deal volume and maximize profitability.

- Recommended Options: Bank lines of credit, portfolio loans, and a robust private lender network.

- Why It Works: These solutions provide access to cheaper and more flexible capital. A revolving line of credit allows you to acquire properties quickly without needing a new loan application for each deal, giving you a significant advantage over competitors.

- The Goal: Become your own ‘bank’ by reducing reliance on transactional funding, enabling you to deploy capital on your own terms and scale your business effectively.

As your real estate investment business grows, your financing needs will change. Partnering with a lender who understands this evolution is critical for long-term success. To explore creative fix and flip financing solutions tailored to your specific investor profile, contact the experts at Icon Capital.

Secure Your Next Profitable Flip with the Right Financing

Navigating the world of real estate investment requires a clear strategy, and your funding is the cornerstone of that plan. As we’ve detailed, choosing the right fix and flip financing is about more than just securing the lowest interest rate. It involves a critical analysis of loan structures and aligning them with your project timeline and profit goals. Understanding how lenders evaluate a deal using metrics like LTV and ARV, and how your own investor profile impacts qualification, gives you a significant competitive advantage in a fast-moving market.

The right financial partner simplifies this process. At Icon Capital, we are specialists in creative financing for real estate investors. We provide the fast, reliable funding essential for securing competitive deals in today’s market. Our team offers expert guidance on structuring your loan to maximize profitability, ensuring your capital works as efficiently as you do.

Get a quote for your next fix and flip project and put our expertise to work for you.

Your next successful investment is within reach. Secure the right capital and execute your strategy with confidence.

Frequently Asked Questions About Fix and Flip Financing

Can you get 100% financing for a fix and flip project?

While 100% financing is not standard, it can be achievable for highly experienced investors with a proven track record. Most lenders finance up to 90% of the purchase price and 100% of the renovation costs, requiring the borrower to contribute some capital. Achieving 100% loan-to-cost (LTC) typically depends on the deal’s strength, the borrower’s portfolio, and the lender’s specific program guidelines. For most beginners, expecting to provide a down payment is a more realistic approach.

What is the 70% rule in house flipping and how does it relate to financing?

The 70% rule is a standard underwriting guideline used to determine the maximum allowable offer on a property. The formula is: (After Repair Value x 70%) – Estimated Repair Costs = Maximum Purchase Price. Lenders use this or similar metrics to assess a deal’s viability and ensure a sufficient profit margin exists to cover financing costs, holding costs, and unforeseen expenses. Adhering to this rule demonstrates to a lender that the project is a sound, data-driven investment.

How are renovation funds typically disbursed in a fix and flip loan?

Renovation funds are not disbursed as a lump sum. Instead, they are held in escrow and released through a draw schedule. After you complete a pre-determined phase of the project, you request a draw. The lender sends an inspector to verify the completed work against your initial scope of work. Once approved, the funds for that phase are released. This process protects both the borrower and the lender by ensuring capital is used as intended for the project’s progression.

What’s the difference between a fix and flip loan and a construction loan?

The primary difference is the project’s scope. A fix and flip loan is designed for renovating an existing residential property. A ground-up construction loan, conversely, finances the building of a new structure on a piece of land. Fix and flip loans typically have shorter terms (12-24 months) and a simpler draw process, whereas construction loans are more complex, involve more extensive underwriting, and have longer terms to accommodate the entire building timeline from foundation to finish.

What is the typical interest rate for a fix and flip loan?

Interest rates for fix and flip financing are variable and depend on several key factors. These include the borrower’s experience level, credit score, the deal’s loan-to-cost (LTC) ratio, and the specific lender. Generally, rates can range from 9% to 13% or higher. More experienced investors with strong financials and lower-leverage deals typically secure rates at the lower end of this spectrum. Rates are higher than conventional mortgages due to the short-term nature and increased risk.

How quickly can you close on a fix and flip financing deal?

Speed is a primary advantage of specialized fix and flip financing. Unlike conventional loans that can take 30-60 days, most fix and flip loans can close in as little as 7 to 14 business days. The timeline is contingent on the lender’s efficiency and the borrower’s ability to promptly provide all required documentation, such as the purchase contract, scope of work, and entity documents. This rapid closing capability is critical for investors competing for properties in fast-moving markets.