Your personal tax returns shouldn’t dictate your ability to acquire a $2 million multifamily asset. For many investors, the traditional 43% debt-to-income limit acts as a hard ceiling that halts portfolio expansion regardless of property performance. You understand that when a rental generates a 1.25x coverage ratio, the borrower’s personal salary becomes irrelevant to the deal’s viability. It’s a common frustration to have the capital and the deal, yet find yourself blocked by rigid bank underwriting that ignores the asset’s actual income potential.

This guide provides the technical framework to master the dscr loan, a tool designed to bypass personal income verification by focusing entirely on asset-level cash flow. You’ll learn how to decouple personal debt from business assets and secure 30-year fixed-rate financing to accelerate your acquisition pace. We’ll examine current 2026 underwriting standards, LTV requirements up to 80%, and the specific mechanics of scaling a high-volume portfolio through property-based leverage. By the end of this article, you’ll have the data needed to structure your next deal without the constraints of traditional lending.

Key Takeaways

- Qualify for financing using property rental income instead of personal tax returns or debt-to-income (DTI) ratios.

- Leverage dscr loans to scale your portfolio without the limitations of personal income-based underwriting.

- Understand how Form 1007 appraisals and FICO scores determine your LTV and interest rate pricing.

- Utilize LLC closing options to shield personal assets while financing single-family or multi-unit properties.

- Learn how creative deal structuring can secure capital for complex files that traditional banks routinely reject.

What is a DSCR Loan? Understanding the Ratio and the Product

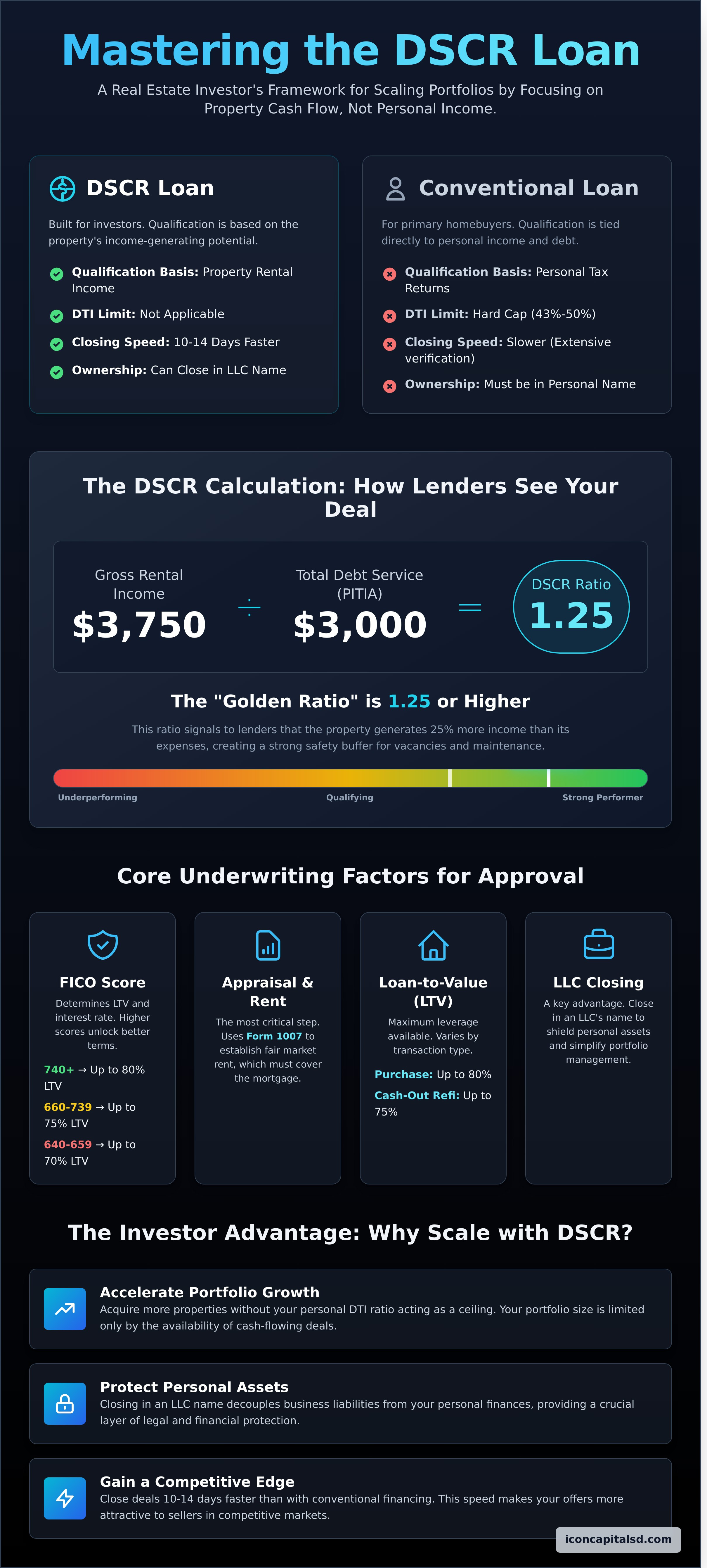

A DSCR loan is a specialized Non-QM mortgage product that qualifies borrowers based on property income rather than personal tax returns. This represents a fundamental shift in risk assessment. Instead of verifying personal income, lenders analyze the property’s ability to cover its own monthly debt. This assessment relies on the Debt Service Coverage Ratio (DSCR) to determine loan eligibility. This structure is essential for professional investors who utilize legal tax deductions that often lower their reported adjusted gross income on 1040 forms.

In 2026, speed and structural flexibility drive the demand for these products. Investors often choose this path because it allows them to close in the name of an LLC. This protects personal assets and simplifies the management of multiple properties. Conventional lenders usually require loans to be in an individual’s name, which creates liability risks and complicates partnership structures. By removing the borrower’s personal financial history from the primary equation, the loan becomes a tool for scaling portfolios efficiently.

The efficiency of the dscr model relies on the “Golden Ratio.” A 1.0 ratio serves as the baseline, indicating that the property’s gross rental income exactly matches its debt obligations. However, the 1.25 ratio is the industry sweet spot. At this level, the property produces 25% more income than its total monthly expenses. This provides a safety buffer for the lender and ensures the investor has a cushion for maintenance and vacancies.

The Basic DSCR Calculation for 2026

Calculating the ratio requires two primary figures. First, determine the Net Operating Income (NOI). Second, calculate the Total Debt Service. The DSCR is a financial metric used by lenders to measure a property’s available cash flow against its total debt obligations. For most residential investment properties, the debt service includes Principal, Interest, Taxes, Insurance, and HOA fees, collectively known as PITIA. Lenders reward higher ratios with better terms. A property with a 1.50 ratio might qualify for a lower interest rate compared to a 1.15 ratio property because the higher cash flow reduces the lender’s risk of default.

DSCR vs. Conventional Mortgages

Traditional conventional loans rely on strict Debt-to-Income (DTI) limits, usually capped between 43% and 50%. This creates a ceiling for investors. DSCR programs bypass these limits entirely. While a conventional underwriter spends weeks verifying W-2s and pay stubs, a dscr underwriter focuses on a lease agreement or a 1007 rent schedule. This streamlined focus allows these loans to close 10 to 14 days faster than traditional mortgages. This speed is critical in competitive 2026 markets where sellers prioritize buyers who can close quickly without the hurdles of personal income verification.

This data-driven approach simplifies the loan process for business owners and self-employed investors. It removes the need for complex tax transcript reviews. Instead, it focuses on the asset’s performance. If the numbers on the property work, the deal moves forward. This clarity allows investors to make offers with confidence, knowing their personal DTI won’t derail the transaction.

How DSCR Loans Work: Underwriting and Mechanism

Underwriting for a dscr loan bypasses personal debt-to-income ratios. Lenders focus on the property’s ability to generate cash flow relative to its debt obligations. How Lenders Use DSCR centers on risk mitigation through asset performance rather than personal salary. This shift allows investors to scale portfolios without the limitations of traditional W-2 documentation.

The appraisal process is the most critical step in the timeline. Unlike a standard residential appraisal, a DSCR appraisal requires Fannie Mae Form 1007. This Single Family Rent Schedule identifies the fair market rent for the property based on local comparables. If the 1007 shows $2,500 in rent but your mortgage is $2,600, the deal’s leverage will be adjusted downward. The appraiser’s data on market rent is just as important as the property’s valuation.

Credit scores still dictate the final terms. While you don’t provide tax returns, your FICO score determines your maximum Loan-to-Value (LTV) and interest rate. For example, an investor with a 740 FICO can often secure 80% LTV for a purchase. An investor with a 660 FICO might be capped at 70% LTV. Most programs require a minimum 640 score to qualify for any leverage at all.

LTV limits typically fluctuate between 70% and 80%. Refinance transactions, specifically cash-out options, usually cap at 75% LTV to maintain a safety buffer for the lender. These limits ensure the investor maintains enough equity to weather market volatility. Prepayment Penalties (PPP) are another standard mechanism. A common structure is a 5-4-3-2-1 schedule, where the penalty decreases by 1% each year. Accepting a longer PPP often results in a lower interest rate, which directly improves the property’s monthly cash flow.

Calculating Net Operating Income (NOI) for DSCR

Lenders calculate NOI by taking the gross potential rent and subtracting vacancy factors and operating expenses. Operating expenses include taxes, insurance, and HOA fees. For 2026, underwriters are applying stricter stress tests to insurance premiums. In high-risk states, we’re seeing 15% to 22% annual increases in insurance cost projections. Short-term rentals (STR) are handled with more scrutiny; lenders may use a 12-month average from AirDNA or apply a 20% haircut to projected income compared to long-term leases to account for higher turnover costs.

DSCR Tiers: 1.0 vs. 1.25 vs. No-Ratio Loans

- Standard Tier (1.20 – 1.25): This is the target for most professional investors. It offers the most competitive interest rates and allows for maximum leverage up to 80% LTV.

- Breakeven Tier (1.0 – 1.15): These loans cover the debt but leave little margin for maintenance. They often require a 700+ FICO or a reduction in LTV to 75% to offset the lender’s risk.

- No-Ratio/Negative Cash Flow: These loans are for properties where the rent doesn’t cover the mortgage, often seen in high-appreciation markets. Qualification is based entirely on the borrower’s liquidity and property equity. Expect to put 30% to 35% down for these specialized products.

If you’re looking to scale your portfolio quickly, you can view our current DSCR options to find the tier that fits your specific asset and credit profile.

The Investor Advantage: Why Scale with DSCR?

Investors use dscr loans to bypass the rigid limitations of debt-to-income (DTI) ratios. Conventional Fannie Mae and Freddie Mac guidelines typically cap an individual at 10 financed properties. This creates a hard ceiling for ambitious portfolios. DSCR loans remove this barrier. Because the loan qualifies based on the property’s cash flow, an investor can hold 20, 50, or 100 loans simultaneously. This is infinite scalability in action. The lender focuses on the asset’s ability to cover its own debt service, not your personal monthly paycheck.

Professional investors rarely hold title in their own names. DSCR lenders allow, and often require, closing in an LLC or Corporation. This structure separates personal assets from property-specific liabilities. If a legal dispute occurs at a rental property, the investor’s personal residence and private bank accounts remain shielded behind the corporate veil. It’s a pragmatic approach to risk management that traditional retail lenders often struggle to accommodate.

The self-employed segment of the workforce, which included 16.3 million workers in 2023, often faces hurdles with traditional financing. High tax write-offs reduce taxable income, which effectively kills a standard DTI calculation. DSCR underwriting ignores personal tax returns entirely. The underwriter looks at the lease agreement and the appraisal’s 1007 rent schedule. If the property’s income exceeds the mortgage payment, the loan moves to closing without a deep dive into your business expenses.

International investors contributed $53.3 billion to the US housing market between April 2022 and March 2023. Many of these buyers lack a US Social Security number or established domestic credit history. DSCR programs bridge this gap. By focusing on the US-based asset’s performance, these loans allow foreign nationals to build domestic portfolios using the property’s projected income as the primary qualifying factor.

DSCR for Short-Term Rentals (Airbnb/VRBO)

Short-term rentals (STRs) often generate 2x to 3x the gross revenue of long-term leases. Lenders use data tools like AirDNA or Rabbu to project income potential for vacation properties. Underwriting for STRs requires a 12-month average to account for seasonality. A property in a mountain town might peak in January but dip in June; lenders look for a stabilized 1.0 to 1.2 coverage ratio across the full calendar year to ensure the debt remains serviceable during off-peak months.

Cash-Out Refinance Strategies

The BRRRR method (Buy, Rehab, Rent, Refinance, Repeat) relies on the ability to pull capital back out after a renovation. Most dscr lenders require a 90-day to 180-day seasoning period before allowing a cash-out refinance based on the new, higher appraised value. This allows investors to recoup 75% to 80% of their total cost basis to fund the next acquisition. Request a custom quote to see current cash-out LTV limits for your specific investment strategy.

- Infinite Scalability: No 10-property limit like conventional financing.

- Asset Protection: Close in an LLC to shield personal wealth.

- No Tax Returns: Qualification is based on property cash flow, not personal 1040s.

- Foreign National Friendly: Build a US portfolio without a US credit score.

DSCR Loan Requirements and Qualification Checklist

Qualifying for a dscr loan requires meeting specific asset and credit benchmarks that differ from traditional mortgage underwriting. Lenders prioritize property cash flow over your personal debt-to-income ratio, but your borrower profile still dictates the final rate and leverage. A 620 credit score serves as the minimum entry point for most programs. Borrowers with 720+ scores access 80% LTV and the lowest interest rates available. If your score falls between 620 and 660, expect a 5% to 10% reduction in maximum leverage and a higher interest rate floor.

Eligible assets include single-family residences, 2-4 unit multi-family properties, and warrantable condos. Some specialized programs extend to 5-8 unit small commercial buildings, though these often require a 1.20 ratio or higher to offset the increased risk. Liquidity is another non-negotiable factor. You must demonstrate 3 to 6 months of PITIA reserves in a verified bank account. If your monthly PITIA is $2,500, you need $15,000 in liquid assets remaining after your down payment and closing costs are paid. Lenders verify this through 60 days of consecutive bank statements.

Experience levels categorize borrowers into two distinct tiers. A “Seasoned Landlord” is defined as someone who has owned and managed 3 or more rental properties within the last 36 months. These investors get the most aggressive pricing and higher LTV caps. “First-Time Investors” are eligible for many dscr programs, but they may face a 0.25% rate increase or a 5% reduction in maximum LTV to compensate for a lack of track record. Providing a clear schedule of real estate owned (SREO) is the fastest way to prove your experience level during the initial intake process.

Essential Documentation for DSCR Applications

You don’t need tax returns or W-2s, but you must provide entity and property-level data. For your LLC, provide the Operating Agreement, EIN letter from the IRS, and a Certificate of Good Standing from your Secretary of State. Property-level needs include the current lease agreement if the unit is occupied. If the property is vacant or a purchase, the appraiser will complete a Form 1007 to determine market rent. You also need a homeowners insurance quote that meets the lender’s replacement cost requirements.

Common Pitfalls to Avoid in DSCR Underwriting

Overestimating market rent is the most frequent cause of deal failure. Appraisers use comparable rentals within a 1-mile radius from the last 6 months; they do not use Zillow “Zestimates” or optimistic projections. Expect the 1007 Rent Schedule to come in 5% to 10% lower than your internal projections. Another pitfall is ignoring the impact of rising costs. In markets like Florida or Texas, insurance premiums rose by 20% in 2024. This increase can drop your ratio from a 1.25 to a 1.15, forcing a lower loan amount. Finally, clarify your prepayment penalty structure. A 3-2-1 structure means you pay 3% in year one, 2% in year two, and 1% in year three if you refinance or sell. Missing these details can cost you thousands in exit fees.

Ready to see how your portfolio qualifies? Apply for a DSCR loan quote today to lock in your rate.

Partnering with Icon Capital for Creative Financing

Icon Capital LLC doesn’t just process applications; we engineer deals. Our methodology centers on structuring the transaction before it ever hits an underwriter’s desk. We verify that the dscr aligns with your specific exit strategy and cash flow targets. This proactive approach eliminates the 30 percent fallout rate often seen with traditional lenders who wait until the final stages to flag eligibility issues. By analyzing the property’s performance and your portfolio goals upfront, we ensure the numbers work from day one.

Traditional banks often reject 45 percent of self-employed borrowers because of complex tax returns or non-traditional income streams. We specialize in the Non-QM space, focusing on the asset’s ability to generate revenue rather than personal debt-to-income ratios. Our team handles files involving multiple LLCs, short-term rental income, and complex ownership structures that retail banks can’t process. This expertise allows us to provide leverage up to 80 percent LTV on properties that would otherwise sit idle in a competitive market.

The 2026 real estate market demands a speed that legacy systems can’t match. Investors need to move from offer to close in 14 to 21 days to remain competitive. Our streamlined internal workflow removes the bureaucratic layers that slow down capital deployment. We integrate Bridge and Fix & Flip loans into our product suite, allowing you to transition from a high-leverage acquisition to long-term dscr financing without changing lenders. This full-lifecycle support provides a seamless path for scaling portfolios from a single asset to 50+ units.

The Icon Capital LLC Loan Process

Our three-step process is built for efficiency and clarity. First, we structure the loan based on the property’s current performance and your long-term investment goals. Second, we move to rapid submission with dedicated underwriting support to resolve any conditions immediately. Third, we maintain direct communication through the final funding stage, ensuring no surprises at the closing table. This method reduces the standard closing timeline by an average of 10 business days compared to traditional commercial channels.

Get Started on Your Next Investment

Property cash flow should be the primary driver of your investment, not personal red tape. We offer custom solutions for foreign nationals and business owners who need to bypass standard documentation requirements. Our programs allow for loan amounts up to $3.5 million with no limit on the number of financed properties you can hold. If you’re ready to leverage your next deal, Request a DSCR loan quote today and see how our creative financing can scale your portfolio. We focus on the mechanics of the deal so you can focus on finding the next asset.

Scale Your Real Estate Portfolio in 2026

The 2026 investment landscape requires financing that prioritizes property performance over personal debt-to-income ratios. Utilizing a dscr loan allows you to bypass traditional tax return hurdles and focus on the cash flow of the asset itself. This mechanism is essential for investors looking to expand their footprint without the constraints of conventional lending limits. High-growth portfolios rely on these property-based metrics to maintain liquidity and capture new opportunities as they arise.

Icon Capital acts as a direct specialist in Non-QM and creative financing, offering streamlined solutions for complex scenarios. Our team brings proven experience to foreign national and self-employed borrowers who often face rejection from retail banks. We use data-driven underwriting to ensure faster closings and reliable funding for every deal. By removing the friction from the qualification process, we help you secure the leverage necessary for long term success. It’s time to move past the limitations of standard mortgages and utilize a structure built for professional growth.

Secure your next investment property with Icon Capital’s DSCR programs

Your next acquisition is within reach with the right capital structure.

Frequently Asked Questions

Is a DSCR loan better than a conventional loan for investors?

A dscr loan is better for scaling a portfolio because it bypasses personal debt-to-income (DTI) limits. While conventional loans limit borrowers to 10 financed properties, these programs allow for unlimited acquisitions. This makes them the preferred choice for professional investors who need to move quickly without the constraints of personal income verification or tax return analysis.

What is a good DSCR ratio for a rental property in 2026?

A 1.25 DSCR ratio is the industry benchmark for 2026 to ensure the property generates 25% more income than its monthly debt obligations. Lenders use this specific figure to mitigate risk against rising maintenance costs and property taxes. Ratios at 1.0 allow for break-even, but a 1.25 score unlocks the most competitive interest rates and 80% LTV options.

Can I get a DSCR loan with a 620 credit score?

You can secure a loan with a 620 credit score, though it typically requires a 25% or 30% down payment. Most lenders reserve their highest leverage products for borrowers with scores above 720. At the 620 level, expect interest rates to be 1% to 2% higher and anticipate stricter reserve requirements to offset the increased credit risk.

How much down payment is required for a DSCR loan?

A standard down payment for this product ranges from 20% to 25% of the purchase price. Some specialized programs allow for 15% down for borrowers with 740+ credit scores, while lower scores often require 30% equity. These requirements ensure the investor maintains a significant stake in the asset, which protects the lender’s position if market vacancy rates increase.

Do DSCR loans require personal tax returns or 1099s?

No, dscr loans don’t require personal tax returns, 1099s, or W-2s to qualify for financing. These are Non-QM products that focus entirely on the property’s rental income potential rather than the borrower’s job history. This streamlined documentation process allows self-employed investors to close deals in 21 days or less without the complexity of personal income audits.

Can I use a DSCR loan for a property I intend to live in?

You cannot use this loan type for a primary residence or any property you intend to occupy. These loans are strictly for business purposes and investment properties. Borrowers must sign an occupancy affidavit at closing confirming the property is for investment only, as these products don’t comply with federal consumer protection laws for owner-occupied housing.

What happens if the DSCR ratio is below 1.0?

If the ratio is below 1.0, the property is considered cash-flow negative, but you can still get funding through “no-ratio” programs. These deals typically require 35% to 40% down payments and carry higher interest rates. Lenders approve these based on the asset’s long-term appreciation potential or the borrower’s liquid reserves rather than monthly rental coverage.

Are DSCR loan interest rates fixed or adjustable?

Interest rates are available in both fixed and adjustable formats, with the 30-year fixed being the most common choice. Many investors also utilize 5/1 or 7/1 ARM structures to secure lower initial rates during the first 60 to 84 months of the term. Some products even offer interest-only payment periods for the first 120 months to maximize monthly cash flow.