Traditional bank financing often creates unnecessary bottlenecks for ambitious real estate investors. If you are frustrated by debt-to-income (DTI) hurdles, restrictive tax return scrutiny, or the persistent ambiguity surrounding how short-term rental (STR) income is treated, you need a more efficient capital solution. Success in the current market requires a precise understanding of dscr loan requirements to ensure your assets-not your personal income-drive your growth and portfolio expansion.

This guide outlines the specific financial and property benchmarks mandatory for securing DSCR financing in 2026. You will gain critical insights into evolving seasoning requirements for cash-out refinances, how to effectively leverage STR revenue for qualification, and the mechanics of closing under an LLC to protect your personal privacy. By mastering these benchmarks, you can bypass traditional lending obstacles, secure high-leverage financing quickly, and scale your real estate portfolio using property-level cash flow. This is the comprehensive roadmap for investors who value speed, efficiency, and data-driven results in a competitive lending environment.

Key Takeaways

- Understand why 2026 market shifts have established DSCR as the primary underwriting tool for professional Non-QM borrowers looking to scale.

- Identify the specific dscr loan requirements for credit tiers and debt service ratios, including benchmarks for qualifying with a 1.0 ratio or lower.

- Explore property eligibility across the spectrum, from single-family residences to the 5-8 unit multi-family assets that enable portfolio expansion.

- Streamline your loan submission by clarifying which property-level data replaces traditional personal income documentation in the underwriting process.

- Master complex financing scenarios, including strategies for high-growth markets and navigating cash-out refinance seasoning requirements.

Understanding DSCR Loan Requirements in the 2026 Market

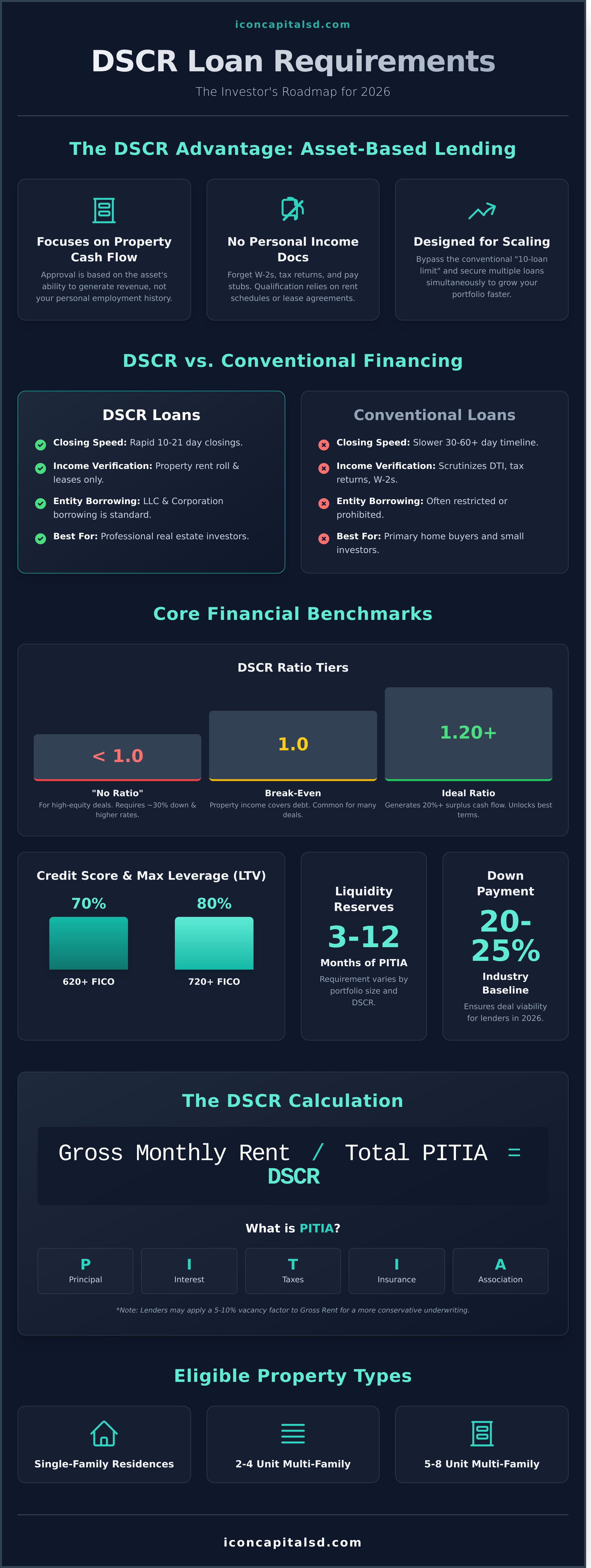

In the 2026 real estate landscape, dscr loan requirements have become the primary benchmark for professional investors seeking to navigate a volatile credit environment. As traditional lending standards have tightened, the Debt Service Coverage Ratio (DSCR) has emerged as the most efficient underwriting tool available for Non-QM borrowers. Rather than scrutinizing a borrower’s personal income, lenders evaluate the property as a self-sustaining business entity. This fundamental shift is driven by the need for pragmatic financing solutions that prioritize property cash flow over personal debt-to-income (DTI) metrics.

The Core Philosophy of DSCR Lending

The primary advantage of DSCR financing is the elimination of personal income verification. Tax returns, W-2s, and pay stubs are discarded in favor of the property’s 1007 rent schedule or existing lease agreements. This approach facilitates rapid portfolio scaling for active investors who may have high paper expenses that disqualify them from traditional bank loans.

- No-Ratio Programs: Specialized options for high-equity deals where the ratio is not the primary factor, allowing for qualification even on vacant or transitionary assets.

- Asset-Based Underwriting: Approval is tied to the property’s ability to generate revenue, not the borrower’s employment history.

- Scalability: Investors can secure multiple loans simultaneously without the “10-loan limit” typically imposed by conventional lenders.

DSCR vs. Conventional Financing Benchmarks

The distinction between DSCR and conventional financing lies in execution and structure. While traditional banks require months of documentation and manual underwriting, dscr loan requirements are designed for speed and efficiency.

- Closing Speed: Most DSCR deals close within 10 to 21 days, providing a competitive edge in fast-moving markets where sellers prioritize certainty of execution.

- Interest Rates: Expect a premium over conventional rates. This trade-off reflects the increased risk profile and the flexibility of the non-recourse or limited-recourse options often available.

- Entity Borrowing: DSCR products are built for professionals. Borrowing as an LLC or Corporation is standard, providing the liability protection and tax advantages that traditional “individual name” financing often restricts.

By focusing on the mechanics of the deal rather than the individual’s financial history, DSCR loans provide a streamlined path to leverage in the current market.

The Financial Benchmarks: Ratio, Credit, and Liquidity

Meeting dscr loan requirements in 2026 hinges on three core pillars: cash flow, credit history, and liquidity. While traditional mortgages focus on personal debt-to-income (DTI) ratios, DSCR underwriting prioritizes the asset’s ability to generate revenue. These benchmarks determine your maximum leverage and the interest rate of the capital.

The “magic number” for most lenders is a 1.20 ratio. This indicates the property generates 20% more income than the total debt obligation. However, the 2026 market offers flexibility; 1.0 ratios-where the property simply breaks even-are common for high-equity deals. Some “no-ratio” programs exist for experienced investors, though these typically require a 30% down payment and higher interest rates to offset the increased risk.

- Credit Tiers: A 720+ score is the benchmark for maximum 80% LTV. Scores near the 620 floor typically cap leverage at 70% and increase the rate by 100-150 basis points.

- Reserves: Expect to show 3 to 12 months of PITIA in liquid reserves. Larger portfolios or lower DSCR ratios often trigger the higher 12-month requirement.

- Down Payment: A 20-25% down payment remains the industry baseline for 2026 to ensure the deal remains viable for the lender.

Calculating Your Debt Service Coverage Ratio

Understanding how to calculate DSCR is vital for structuring a deal. Lenders use the PITIA formula-Principal, Interest, Taxes, Insurance, and HOA dues. Most programs utilize gross monthly rent to determine the ratio. In competitive 2026 rental markets, underwriters may apply a 5-10% vacancy factor to the gross income to ensure the loan remains sustainable during tenant turnover, rather than relying solely on Net Operating Income (NOI).

Credit and Liquidity Standards

To secure maximum leverage, a strong credit profile is non-negotiable. Beyond the score, lenders verify the sourcing and seasoning of down payment funds, typically requiring 60 days of bank statements. While some dscr loan requirements allow for the use of business assets or gift funds, these must be documented with clear paper trails to meet compliance standards. Using business entities (LLCs) for vesting is standard, but the primary guarantor’s liquidity remains the focal point of the risk assessment.

Property Eligibility: From Single-Family to 5-8 Unit Multi-Family

DSCR loans are not limited to standard residential housing. While Single-Family Residences (SFR), 2-4 unit properties, and Planned Unit Developments (PUDs) are the baseline, modern dscr loan requirements have expanded to include 5-8 unit multi-family buildings. This allows investors to bridge the gap between residential and commercial financing using a single debt product.

For condos, the distinction between warrantable and non-warrantable is critical. Non-warrantable condos-those with high commercial space concentration or single-entity ownership-often require specialized DSCR programs with adjusted LTV limits. Short-term rentals (STRs) like AirBnB and VRBO are also eligible, though lenders typically require a 12-month history or a specialized STR appraisal to verify income stability.

Multi-Unit and Small Commercial DSCR

Financing 5-8 unit properties requires a shift from residential to small commercial underwriting standards. Appraisals for these assets focus heavily on the income approach rather than just sales comparables. Because larger properties carry higher operational overhead, lenders may require a slightly higher Debt Service Coverage Ratio (DSCR) to mitigate risk, often targeting 1.20x or higher compared to the 1.0x allowed on smaller assets.

Foreign National Qualification Path

International investors can leverage dscr loan requirements to build a US portfolio without a domestic credit score. Qualification is based on the property’s cash flow and the borrower’s global liquidity. Key requirements include:

- Identification: Valid passport and/or ITIN.

- Asset Verification: 6-12 months of reserves held in a US-based or internationally recognized financial institution.

- Credit: A credit reference letter from a local bank may be substituted for a standard FICO score.

Appraisal and Rent Schedule (Form 1007)

The Form 1007 (for single-family) or Form 1025 (for multi-family) Rent Schedule is the most critical document in the loan file. It establishes the “Market Rent” used to calculate the coverage ratio. For vacant properties or new acquisitions, the appraiser’s estimate of market rent-not the current lease-dictates the loan amount. In emerging markets where appraisals might come in low, providing documented local rent comps is essential to support the valuation and maintain the desired leverage.

The DSCR Loan Documentation Checklist

Efficiency in the underwriting process is driven by the quality of your initial submission. While the industry often refers to these as “no-doc” loans, that label is a misnomer. While personal tax returns and W2s are excluded, they are replaced by comprehensive property data. To meet dscr loan requirements in 2026, your file must focus on the asset’s ability to generate cash flow and your legal capacity to hold title.

Closing in an entity is standard for most investors. Underwriters require clear Articles of Incorporation and an Operating Agreement to verify signing authority. Furthermore, insurance standards have tightened; 2026 requirements typically dictate a policy covering 100% of the replacement cost to account for increased construction and material valuations.

Essential Borrower Documents

- Identification: Valid photo ID and proof of legal residency (Foreign National programs are available with passport verification).

- Liquidity: Two months of consecutive bank statements showing sufficient “cash to close” and required interest reserves.

- SREO: A detailed Schedule of Real Estate Owned to verify your track record and experience level, which can impact LTV tiers.

Property-Specific Documentation

- Income Verification: Executed long-term lease agreements or a 12-month history for Short-Term Rentals (STR).

- Transaction Details: A fully executed purchase contract or a current mortgage statement for refinance transactions.

- Title and Escrow: Preliminary title reports and contact information for the settlement agent.

Accelerating the Approval Process

To ensure an “underwriter-ready” submission, avoid common pitfalls such as undisclosed debt or incomplete entity filings. Delays often occur when bank statements show large, unexplained deposits or when the SREO does not match the credit report. Providing a clean, organized digital file reduces “touches” by the underwriter and moves the loan to clear-to-close faster. To verify your specific deal docs and ensure you meet the latest dscr loan requirements, you can request a custom quote from our team today. For more information on our leverage options, visit iconcapitalsd.com.

Navigating Complex DSCR Scenarios with Icon Capital

Standard lending models often fail to account for the nuances of high-growth real estate markets. In 2026, investors frequently encounter “Low-Ratio” scenarios where property appreciation outpaces rental growth. Icon Capital LLC solves this through specialized no-ratio and low-ratio products, allowing investors to secure financing even when the DSCR falls below 1.00 by emphasizing credit depth and liquidity.

For those looking to recapture equity, our cash-out refinance programs are designed for efficiency. While standard dscr loan requirements often mandate 12 months of ownership, we offer seasoning periods as short as 6 months with LTV caps reaching 75%. This is critical for investors transitioning from a Fix & Flip bridge loan into a long-term hold, effectively executing the BRRRR strategy without capital stagnation.

- High-Growth Strategy: Financing for properties in appreciating markets with lower initial yields.

- Refinance Flexibility: Competitive LTV caps for rapid capital extraction.

- Seamless Transitions: Moving assets from short-term debt to 30-year fixed DSCR products.

Creative Financing and Non-QM Solutions

Icon Capital LLC operates as a direct specialist, providing flexibility that retail banks cannot match. We combine DSCR metrics with asset-based qualification to maximize leverage for complex portfolios. This includes handling properties with minor deferred maintenance or “C4” condition ratings that typically disqualify a deal at a traditional institution. By focusing on the asset’s potential and the borrower’s experience, we structure deals that prioritize speed and certainty of closing.

Next Steps: Structuring Your 2026 Deal

In a competitive market, speed is the ultimate leverage. Meeting dscr loan requirements is only the first step; structuring the deal for maximum ROI requires an expert lens. Our 4-step workflow-Structure, Submission, Underwriting, and Closing-is engineered to move your deal from initial quote to funded status without the friction of traditional mortgage processing.

Ready to scale your portfolio with a partner that understands non-traditional lending? Submit your deal structure today for a rapid expert review and see how Icon Capital LLC provides the creative leverage you need to win in 2026.

Mastering DSCR Loan Requirements for 2026 Success

Navigating the dscr loan requirements in the current market requires a precise understanding of debt coverage ratios, liquidity benchmarks, and property eligibility. From single-family residences to 5-8 unit multi-family assets, securing favorable terms depends on aligning your portfolio with a lender that understands the mechanics of Non-QM creative financing. Icon Capital specializes in bridging the gap for investors who require authoritative guidance and efficient loan structuring.

Our team provides deep transactional expertise, offering dedicated Foreign National loan programs and specialized financing for 5-8 unit properties. We focus on the technical aspects of your deal-leveraging assets and simplifying the documentation process to ensure you meet qualification standards without unnecessary delays. By focusing on data-driven outcomes and pragmatic solutions, we enable you to scale your real estate portfolio with confidence.

Ready to secure your next asset? Request a DSCR Loan Quote from Icon Capital and put our specialized lending expertise to work for your investment strategy. We are committed to helping you achieve your financial objectives with speed and professionalism.

Frequently Asked Questions

What is the minimum credit score for a DSCR loan in 2026?

In 2026, the minimum credit score for most DSCR programs is 620. However, investors seeking the most competitive interest rates and maximum leverage-up to 80% LTV-should aim for a score of 720 or higher. Lower scores typically trigger adjustments to the rate and may require a larger down payment to offset the perceived risk to the lender.

Can I get a DSCR loan with a 1.0 ratio or lower?

Yes, financing is available for properties with a 1.0 ratio or even “no-ratio” structures. While standard dscr loan requirements typically favor a 1.20 DSCR to ensure a safety margin, we offer specialized products for properties with high appreciation potential. These “no-ratio” loans generally require a higher down payment, often 30% to 35%, and a strong borrower liquidity profile.

Do DSCR loans require personal tax returns or 1099s?

DSCR loans do not require personal tax returns, W-2s, or 1099 forms. Qualification is based entirely on the rental income generated by the subject property rather than the borrower’s personal income. This makes the product an ideal solution for self-employed investors or those with significant tax deductions who cannot meet the debt-to-income (DTI) standards of traditional conventional financing.

What are the seasoning requirements for a DSCR cash-out refinance?

Standard seasoning for a DSCR cash-out refinance is typically six months to utilize the new appraised value. If you refinance before the six-month mark, the loan amount is generally restricted to the original purchase price plus documented capital improvements. After 180 days of ownership, investors can leverage the full market appreciation to extract equity for subsequent property acquisitions.

Can foreign nationals qualify for DSCR loans without a US credit score?

Foreign nationals can qualify for DSCR loans without a US credit history. Lenders often utilize international credit reports or approve the file based on the asset’s cash flow and the borrower’s global liquidity. These programs usually cap the LTV at 65-70% and require 12 months of PITI reserves to be held in a US-based financial institution prior to closing.

Are prepayment penalties standard on DSCR investment loans?

Prepayment penalties are standard on the majority of DSCR products, typically structured as a 5-year step-down (5-4-3-2-1). This structure allows lenders to offer more aggressive interest rates. Investors can often negotiate a shorter 1-year or 3-year penalty period or buy out the clause entirely by accepting a slightly higher interest rate at the time of origination.

Can I use a DSCR loan to purchase a 5-8 unit apartment building?

Yes, you can utilize DSCR financing for 5-8 unit multi-family assets. While 1-4 unit properties follow residential-style DSCR guidelines, 5+ units are underwritten as commercial assets. The dscr loan requirements for these buildings may include a more rigorous review of the rent roll and operating expenses (NOI), but the focus remains on the property’s ability to service the debt.

How much cash reserves do I need for a DSCR loan approval?

Most DSCR programs require between 3 and 9 months of PITI (Principal, Interest, Taxes, and Insurance) reserves. The specific requirement depends on the borrower’s credit score and the total number of properties currently financed. These reserves must be verified in a liquid or semi-liquid account, such as a business checking account, personal savings, or a brokerage account, to ensure operational stability.