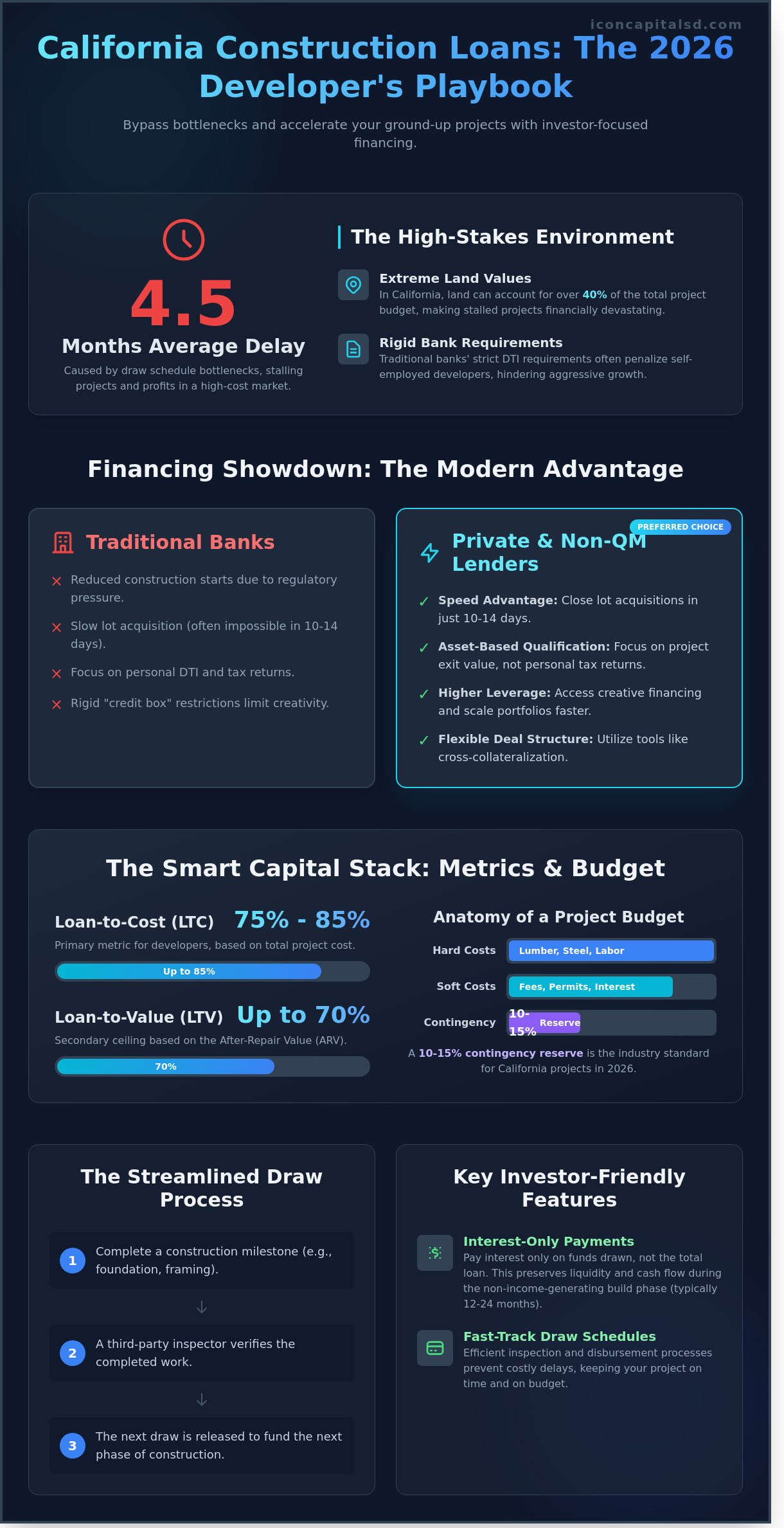

In 2024, the average California construction project faced delays of 4.5 months due to draw schedule bottlenecks alone. You know that in a market with high land costs, a stalled project is a failing investment. Traditional banks often impose rigid DTI requirements that penalize self-employed developers. This makes it difficult to secure the construction loans California developers need for aggressive ground-up growth. You need a financing partner that prioritizes speed and deal structure over bureaucratic red tape.

This guide provides a data-driven breakdown of high LTC and LTV ratios for the 2026 market. We’ll show you how to access creative lending solutions that offer interest-only payments during the build phase and fast-track draw schedules. You’ll learn exactly how to optimize your capital stack to maintain liquidity and scale your portfolio. This analysis covers the essential mechanics of non-traditional financing and the specific criteria used to approve complex, high-leverage development projects.

Key Takeaways

- Understand how California’s unique land values dictate specific equity requirements and loan structures for ground-up development.

- Master the critical metrics of LTC and LTV based on After-Repair Value (ARV) to optimize leverage and capital efficiency.

- Discover how to bypass traditional bank “credit box” restrictions by utilizing creative cross-collateralization and asset-based lending.

- Navigate the specialized approval process for construction loans california by streamlining developer vetting and project feasibility analysis.

- Explore strategies for scaling your real estate portfolio through creative financing for multi-unit and mixed-use development projects.

Understanding Construction Loans in the California Real Estate Market

Construction loans in California function as short-term, interim financing designed specifically for ground-up development. Unlike a standard mortgage, these loans provide capital in draws based on completed construction milestones. In 2026, California’s land values continue to dictate aggressive equity requirements. Investors often face loan-to-cost (LTC) ratios where land value accounts for 40% or more of the total project budget. This environment necessitates a sophisticated project financing structure to manage cash flow during the 12 to 24 month build cycle.

Ground-Up Construction vs. Major Renovation

The line between a renovation and ground-up construction depends on structural integrity. If you’re removing more than 50% of existing exterior walls or replacing the entire foundation, lenders categorize the project as ground-up. Financing for a total scrape involves higher risk and different draw schedules than a standard remodel. Many investors prefer fix and flip loans for projects involving cosmetic updates or minor structural changes because the underwriting is faster. Ground-up projects require fully approved architectural plans and permits before the first dollar is released, making the pre-development phase more capital-intensive.

The Role of Private and Non-QM Lenders

Traditional banks have significantly reduced their California construction starts in 2026. Regulatory pressure and capital reserve requirements have made them cautious. This retreat leaves a gap filled by private and non-QM lenders. Private capital offers a distinct speed advantage. Closing a lot acquisition in 10 to 14 days is often impossible with a retail bank but standard for private firms. Non-QM products allow for asset-based qualification. These loans focus on the project’s projected exit value or the developer’s liquid assets rather than personal tax returns. This flexibility is essential for developers with complex portfolios who need to scale quickly without the friction of traditional debt-to-income hurdles. Using construction loans california through non-traditional channels allows for higher leverage and faster execution in a competitive market.

Key Financial Metrics: LTC, LTV, and the Draw Schedule

Securing construction loans california requires a deep understanding of leverage metrics. Loan-to-Cost (LTC) is the primary tool for developers. It measures the loan amount against the total cost of construction. Lenders typically provide 75% to 85% LTC for qualified sponsors. Loan-to-Value (LTV), based on the After-Repair Value (ARV), acts as the secondary ceiling. Most 2026 programs limit LTV to 70%. Balancing these metrics is vital for building a Smart Capital Stack that minimizes personal capital injection while maintaining project solvency.

Funds are not released in a lump sum at closing. Instead, they follow a strict draw schedule tied to specific construction milestones. Interest-only payments are the standard for construction loans california during the vertical build phase. You only pay interest on the funds that have been disbursed, not the total loan commitment. This preserves liquidity when the project is not yet generating rental or sales income. It’s an essential feature for maintaining cash flow through the duration of the build.

Calculating Your Total Project Cost

Total project cost is divided into hard costs and soft costs. Hard costs include tangible items like lumber, steel, and labor. Soft costs cover architectural fees, permits, and interest carry. For California projects in 2026, a 10% to 15% contingency reserve is the industry standard to account for material price fluctuations. Lenders perform a “cost to complete” analysis at every stage. They ensure that the remaining loan balance is always sufficient to finish the project. If costs exceed the original budget, the developer must cover the gap before the next draw is released.

Managing the Inspection and Draw Process

Third-party inspectors verify progress before any funds are released. They visit the site to confirm that milestones like foundation pouring or framing are 100% complete. Delays in funding often happen because of missing lien waivers or disorganized documentation. To keep your contractor on schedule, maintain a clear paper trail for every line item. Submit draw requests early with all required signatures from subcontractors. Efficient draw management ensures that crews stay on-site and the project remains on track. You can request a quote to see how our structured draw process supports your development timeline.

Investor-Focused Financing vs. Traditional Bank Construction Loans

Traditional retail banks prioritize personal income stability over project viability. This creates the “Credit Box” problem. Most active developers show minimal taxable income due to aggressive depreciation and business expenses. While a bank sees a high Debt-to-Income (DTI) ratio as a risk, a private lender views the underlying asset. Private construction loans california focus on the project’s After Repair Value (ARV) and the developer’s track record rather than personal tax returns.

Efficiency is the primary differentiator in the 2026 market. Retail banks typically require 60 to 90 days for full underwriting and committee approval. Private capital closes in 14 to 21 days. This speed allows investors to secure land and start grading before bank-funded competitors even finish their appraisal reviews.

Flexibility in collateral further separates these options. Investors can use cross-collateralization, leveraging equity in existing rental portfolios to reduce or eliminate the required cash down payment for a new build. Once the project is complete, the standard exit involves transitioning from the construction note to DSCR loans. This move stabilizes the asset for a long-term hold based on the property’s rental income rather than the borrower’s personal earnings.

Non-QM Solutions for Developers

Self-employed general contractors often lack the W-2 documentation banks demand. Non-QM solutions allow for 12 or 24-month bank statement reviews to verify cash flow. P&L-based loans also serve developers who operate through complex corporate structures. For international capital, foreign national programs provide 65% to 70% LTV options for investors without a US credit history, a vital tool in California’s luxury market.

Bridge-to-Construction: The Strategic Play

Speed is critical when land hits the market. A bridge loan secures the dirt in under 10 days, preventing a lost opportunity while permits are finalized. Developers then transition to a construction loan once the project is shovel-ready. In some cases, starting with hard money fix and flip loans provides the necessary leverage for heavy rehabs that evolve into ground-up builds. Single-close construction-to-permanent structures are also available to lock in long-term rates early, reducing interest rate risk during the 12 to 18-month build cycle.

The Step-by-Step Approval Process for California Construction Projects

The approval for construction loans california relies on a methodical evaluation of both the borrower’s history and the project’s financial viability. Lenders in 2026 prioritize the developer’s track record above almost all other factors. To secure the most competitive leverage, you’ll typically need to demonstrate at least three successful ground-up completions within the last five years. Underwriters look for consistency in project scale and asset class to ensure you can manage the complexities of the California building environment.

Project feasibility analysis follows the initial vetting. This involves a granular review of the Pro Forma and the Budget Sworn Statement. Lenders analyze the “as-completed” value against the total cost of construction to determine the loan-to-cost (LTC) and loan-to-value (LTV) ratios. You must include a 10% to 15% contingency reserve in your budget. This buffer is essential for absorbing sudden shifts in material costs or labor shortages that often occur during multi-year builds.

Essential Documentation for a Construction Loan

- Executive Summary: A concise pitch detailing the project’s profitability, target demographic, and exit strategy.

- Detailed Line-Item Budget: A comprehensive breakdown of hard and soft costs, including architecture fees and city impact fees.

- California-Specific Insurance: Proof of Builder’s Risk and General Liability policies that specifically name the lender as the loss payee.

- Construction Timeline: A realistic schedule that accounts for mandatory inspections and potential weather delays.

Navigating California Permits and Entitlements

Ready to move forward with your next development? Request a quote today to see how our creative financing solutions can scale your portfolio.

Leveraging Creative Financing for California Development Projects

Scaling from 1-4 units to the 5-8 unit range represents a significant jump in complexity. Traditional lenders often classify these as commercial projects with grueling documentation requirements. Icon Capital uses specialized underwriting that focuses on the Debt Service Coverage Ratio (DSCR) of the future finished building. This allows you to secure terms based on projected 2026 market rents.

Many of our clients find that types of loans for flipping houses serve as the initial gateway to these larger projects. Once you’ve established a track record of successful exits, transitioning into 5-8 unit ground-up builds becomes the logical step for portfolio growth. We provide the leverage needed to manage these midsize apartment developments without the red tape of a retail bank.

The Icon Capital Advantage: Speed and Scale

We provide direct access to decision-makers and underwriters who understand the specific nuances of the California building code and local zoning laws. You don’t have to wait weeks for a committee to review your file. We customize loan terms to match your development’s lifecycle, ensuring you have the capital you need at every phase of the build.

- Direct communication with specialized CA underwriters.

- Customized draw schedules that align with your construction milestones.

- Loan structures designed for non-traditional borrowers and business owners.

- High LTV and LTC options for experienced developers.

If you’re ready to break ground on your next project, our team is prepared to structure a deal that fits your specific timeline and exit strategy. Request a customized construction loan quote today

Accelerate Your 2026 Development Strategy

Managing a ground-up project requires precise execution of financial metrics. Success depends on balancing LTC ratios and ensuring a seamless draw schedule to keep subcontractors on-site. Investor-focused financing offers a distinct advantage over traditional bank products by prioritizing the project’s viability and your track record. Icon Capital specializes in these complex scenarios. We provide Specialized Non-QM and Investor Programs designed to navigate the specific regulatory requirements of the 2026 market. Our team manages loan amounts up to $2M+ and brings direct experience with California-specific development hurdles. Securing construction loans california through a direct, expert channel ensures you’ve the capital necessary to scale your portfolio without the typical delays of retail lending. We focus on the mechanics of your deal so you can focus on the build. Take the next step toward breaking ground on your next high-value asset. We’re ready to help you structure a winning deal today.

Get a Professional Construction Loan Quote

Frequently Asked Questions

What is the minimum down payment for a construction loan in California?

Minimum down payments for construction loans California typically range from 20% to 30% of the total project cost. Private lenders often require 25% equity to mitigate risk on ground-up developments. Conventional programs might allow for 20% down, but non-QM and hard money options fluctuate based on the borrower’s experience and credit profile. High-leverage options exist for seasoned developers with a proven track record of five or more completed projects.

Can I get a construction loan with a bank statement loan if I am self-employed?

Self-employed borrowers can qualify for construction financing using 12 or 24 months of personal or business bank statements. This Non-QM solution replaces the need for traditional tax returns or W-2s. Lenders analyze average monthly deposits to calculate qualifying income for the loan. You’ll need to provide a profit and loss statement and proof of two years of continuous self-employment in the same industry to meet underwriter guidelines.

How long does the approval process take for a private construction loan?

Private construction loan approvals typically take 10 to 21 business days from submission to funding. This speed is a primary advantage over traditional banks, which often require 45 to 60 days for similar files. The timeline depends on the speed of the appraisal and the completeness of the builder’s budget and plans. Having a shovel-ready project with permits already in place can reduce the underwriting period by 5 to 7 days.

What is the difference between LTC and LTV in construction financing?

LTC represents the percentage of total construction costs the lender will fund, while LTV is the percentage of the completed project’s appraised value. Most construction loans California lenders cap LTC at 80% and LTV at 70% to 75%. For example, if a project costs $1 million to build and will be worth $1.5 million, an 80% LTC loan provides $800,000. Underwriters use both metrics to ensure the project maintains sufficient equity.

Do I need to own the land before applying for a construction loan?

You don’t need to own the land prior to applying because many programs offer land-plus-construction financing. This structure allows you to purchase the lot and fund the build with a single closing. If you already own the land, the equity you’ve built can often serve as your down payment. Lenders require a recorded deed and a clear title report before they’ll release the first draw for site preparation and foundation work.

Are construction loan rates higher than standard mortgage rates?

Construction loan rates are generally 1% to 4% higher than standard 30-year fixed mortgage rates. These loans carry higher risk for the lender since the collateral doesn’t exist yet. Most construction financing uses interest-only payments during the build phase to manage cash flow. Rates vary based on the loan type, with hard money options sitting at the higher end of the spectrum compared to institutional bridge or Non-QM products.

Can foreign nationals apply for construction loans in California?

Foreign nationals can secure construction loans in California through specialized Non-QM programs that don’t require a Social Security number or US credit history. Borrowers must typically provide a valid passport, a visa, and a letter of reference from a foreign financial institution. LTV limits for foreign nationals often cap at 60% to 65% to account for the increased risk profile. These loans focus on the asset’s value and the developer’s liquidity.

What happens if my construction project goes over budget?

Lenders require a built-in contingency reserve of 10% to 15% of the total budget to cover unexpected cost overruns. If expenses exceed this reserve, the borrower is responsible for funding the gap out of pocket before the lender releases further draws. Maintaining a balanced loan is a critical requirement in the loan agreement. Failure to cover overruns can lead to a default or a halt in construction progress until the budget is reconciled.