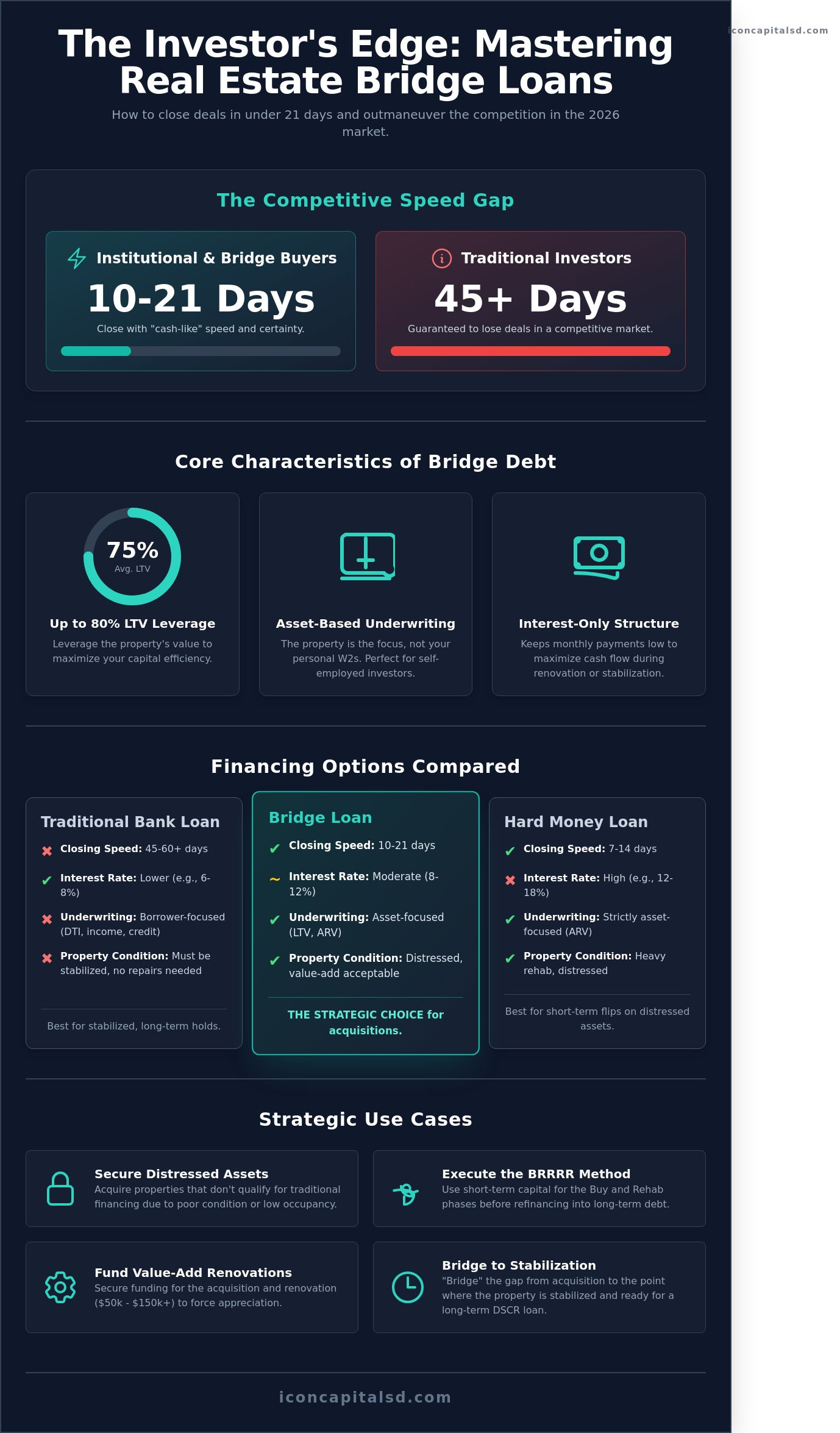

In the 2026 market, waiting for a 45 day bank approval is a guaranteed way to lose a deal. Institutional buyers are closing in 10 days or less, leaving traditional investors behind. A bridge loan for real estate investment is the tactical tool you need to bridge this gap and secure distressed assets before the competition can even run their numbers.

You’ve likely felt the frustration of losing a high-margin property because your financing wasn’t fast enough. High hard money interest rates and the complexity of non-QM loan requirements shouldn’t stop your growth. This guide shows you how to master the mechanics of bridge financing to close deals in under 21 days. We’ll explore how interest-only structures keep your monthly payments low while you prepare for a long-term refinance. You’ll get a clear roadmap to use 75% LTV leverage to scale your portfolio with precision and speed. It’s time to stop reacting to the market and start dictating the terms of your next acquisition.

Key Takeaways

- Master the strategic use of a bridge loan for real estate investment to bridge the gap between immediate acquisition and long-term exit.

- Accelerate your acquisition timeline by leveraging collateralized assets to secure funding in as little as 10–21 days.

- Evaluate the cost of capital across bridge, hard money, and traditional debt to identify the most efficient leverage for your next deal.

- Learn how to deploy bridge financing to execute the BRRRR method and snag distressed assets before traditional buyers can compete.

- Streamline your transition from short-term capital to long-term DSCR loans through a structured, no-nonsense closing process.

What Is a Bridge Loan for Real Estate Investment?

A bridge loan for real estate investment serves as a 12 to 24-month capital solution. It secures the asset while the investor executes a value-add plan or waits for a permanent take-out loan. Understanding what a bridge loan is requires viewing it as a tactical tool rather than a long-term debt burden. It functions as a liquidity bridge, allowing for the immediate acquisition of properties that require rapid closing timelines.

The primary advantage of this financing is its “cash-like” nature. In the competitive 2026 market, sellers often prioritize offers that aren’t contingent on 60-day bank appraisals. A bridge loan allows an investor to close in as little as 10 to 14 days. This speed enables investors to compete directly with all-cash buyers, securing distressed or under-managed assets at a discount. It’s important to distinguish these from residential “swing” loans. While swing loans help homeowners move between primary residences, investment bridge debt is a business-purpose tool designed for scaling portfolios and maximizing ROI.

The Core Characteristics of Investment Bridge Debt

Bridge capital prioritizes asset value and exit strategy over the borrower’s personal income history. This makes it a primary choice for self-employed investors or those with complex tax returns. Key features include:

- LTV Ratios: Most programs provide 70% to 80% loan-to-value, depending on the property type and condition.

- Interest-Only Payments: Loans are structured with interest-only periods. This maximizes monthly cash flow during the critical transition or renovation phase.

- Asset-Based Underwriting: Underwriters focus on the property’s current and future value. They don’t spend weeks verifying every line of a personal W2.

Why Investors Are Deploying Bridge Capital in 2026

The 2026 lending environment demands agility. Investors use a bridge loan for real estate investment to navigate a landscape where traditional banks have tightened their belts. Many properties don’t yet qualify for long-term DSCR or agency loans because they lack 90% occupancy or require structural repairs. Bridge debt fills this gap. It allows an investor to secure the property, complete a $50,000 to $150,000 renovation, and then refinance into a lower-rate product once the value is proven. This strategy preserves the investor’s liquid capital for additional acquisitions rather than tying it up in a single down payment. If you are ready to analyze a specific deal, you can request a quote to see current market rates.

The Mechanics: How Investment Bridge Loans Work

A bridge loan for real estate investment functions as short-term capital to fill the gap between immediate acquisition and long-term financing. Unlike traditional bank loans that focus heavily on borrower debt-to-income ratios, these products prioritize the asset itself. Lenders secure the debt through a first lien on the subject property or by cross-collateralizing other assets within an investor’s portfolio. Understanding how bridge loans work is essential for investors who need to move from application to closing in as little as 10 to 21 days. The cost structure typically involves interest rates ranging from 8% to 12% and origination fees between 1 and 3 points.

The role of the exit strategy is the most critical component of the loan’s mechanics. Lenders require a clear, documented path to repayment before funding. This usually involves selling the renovated property or refinancing into a long-term DSCR loan. Without a viable exit, the risk profile becomes too high for non-QM lenders. Speed and certainty of execution are the primary benefits, allowing investors to secure properties that wouldn’t qualify for 30-year conventional financing due to condition or timelines.

Underwriting Based on Asset Value

Underwriting focuses on the property’s Current Market Value (CMV) or the After Repair Value (ARV). This asset-centric approach allows for significantly reduced documentation requirements. You won’t find the same red tape here that you’d face with a retail bank. Lenders prioritize the property’s location and liquidity. A property in a high-demand market with a 75% loan-to-value (LTV) ratio is often approved faster than a stronger borrower with a weaker asset. This helps investors leverage their capital to scale portfolios quickly without the constraints of personal income verification.

Interest-Only Payments and Balloon Terms

Most bridge structures utilize interest-only payments. This keeps monthly holding costs low during the critical ‘bridge’ period while renovations or leasing activities occur. These loans typically carry a term of 12 to 24 months. At the end of this term, a balloon payment for the full principal balance is due. It’s a standard requirement in the industry. If a project takes longer than the initial 18-month projection, many lenders offer 6-month extension options for an additional fee. This flexibility protects the investor from market shifts or construction delays. If you have a property in mind, you can request a quote to see how these terms apply to your specific deal.

Bridge Loans vs. Hard Money vs. Traditional Mortgages

Success in the 2026 market requires matching the right debt to the specific lifecycle of an asset. A bridge loan for real estate investment occupies the critical space between high-cost private capital and slow-moving institutional bank debt. Speed is the primary differentiator. While a traditional mortgage requires a 45 to 60-day window for processing and appraisal, hard money lenders can fund in as little as 3 days. Bridge financing typically settles in the 14 to 21-day range. This provides enough speed to win competitive bids without the 12% to 15% interest rates associated with hard money.

- Capital Cost: Bridge rates often hover between 8% and 10%, whereas traditional debt remains in the 6% to 7.5% range for investment properties.

- Qualification: Lenders prioritize a 1.20 Debt Service Coverage Ratio (DSCR) and asset value over a borrower’s personal income history.

- Asset Condition: Using a bridge loan for real estate investment allows for the purchase of non-stabilized properties with occupancy rates below 80%. These assets are routinely rejected by conventional underwriters.

When to Choose Bridge Over Hard Money

Bridge financing is the superior choice for “rent-ready” assets or properties needing only light cosmetic work. You benefit from longer terms, usually 12 to 24 months, compared to the rigid 6-month windows found in many hard money contracts. This provides a safety net if market conditions shift or construction permits are delayed. Professional investors also value the institutional-grade reporting and lower origination fees, which typically range from 1% to 2% of the loan amount. For those looking to scale a portfolio, requesting a quote for a bridge product can preserve more equity than hard money alternatives.

Why Traditional Mortgages Often Fail Investors

Conventional financing frequently collapses due to the seasoning requirement. Most banks won’t refinance a property based on its new appraised value until you’ve held the title for at least 6 to 12 months. This delay traps your capital and prevents rapid portfolio growth. Strict DTI limits also disqualify the 30% of investors who are self-employed and utilize legal tax deductions to lower their taxable income. If a property has a damaged roof or lacks a functional HVAC system, it fails the property condition standards required for a traditional loan. Bridge capital ignores these cosmetic flaws to focus on the exit strategy.

Strategic Use Cases: When to Deploy a Bridge Loan

A bridge loan for real estate investment acts as a high-velocity tool for sophisticated players. It isn’t merely a temporary fix; it’s a tactical advantage in markets where speed and asset quality outweigh personal credit profiles. Investors deploy this capital to capture distressed assets, stabilize underperforming portfolios, or bypass the 60-day underwriting cycles of traditional banks. In competitive environments, the ability to move in 10 to 14 days separates top-tier firms from the rest of the field.

- The BRRRR Method: Utilizing a bridge loan for real estate investment serves as the primary engine for the “Buy” and “Rehab” phases. Investors typically secure 75% of the purchase price and 100% of the renovation costs. This allows for rapid execution before refinancing into a long-term DSCR loan once the property is stabilized and appraised at its new value.

- Multi-Unit Stabilization: Bridging the gap for 5-8 unit properties is essential when the current net operating income (NOI) doesn’t support a permanent commercial loan. A 12-month bridge provides the runway to increase occupancy to the 90% threshold required by institutional lenders.

Winning the Deal in Competitive Markets

Speed often carries more weight than the offer price. Using a bridge loan allows you to offer a 14-day close, effectively competing with cash buyers and beating out traditional offers that require 45 days of bank due diligence. This agility is critical for bank-owned REOs or auction-style purchases where the window for funding is narrow. You can also utilize cross-collateralization, leveraging equity in your existing portfolio to cover 100% of a new acquisition’s down payment without liquidating current assets.

Special Considerations for Foreign Nationals

International investors frequently use bridge debt as their primary entry point into the US market. These loans solve the problem of missing social security numbers or domestic tax returns by focusing on the property’s performance. Most programs for foreign nationals require a 30% to 35% down payment but waive the need for a domestic credit score. Asset-based qualification bypasses traditional credit history by prioritizing the property’s debt service coverage ratio and the borrower’s liquid reserves over domestic credit scores.

Securing Your Bridge Loan with Icon Capital

Icon Capital eliminates the friction common in traditional banking by focusing on deal mechanics rather than rigid borrower profiles. Our process is built on three pillars: Structure, Submit, and Close. We bypass the red tape that often stalls 2026 acquisitions, allowing investors to move from initial inquiry to funded status in as few as 10 business days. This speed is essential when utilizing a bridge loan for real estate investment to capture undervalued assets before competitors can secure financing.

- Structure: We tailor the LTV and interest-only periods to your specific project timeline.

- Submit: Our streamlined digital portal accepts your documents without redundant paperwork.

- Close: We fund directly, ensuring the capital is available when your purchase contract demands it.

We provide creative financing solutions for complex deals that don’t fit standard boxes. Whether you are dealing with a short-term vacancy or a heavy value-add project, we focus on the asset’s potential and your track record. Our loan amounts scale up to $50 million, providing the necessary leverage to grow your portfolio quickly. We don’t rely on bureaucratic committees; we rely on data and asset value.

The ‘Bridge-to-DSCR’ Exit Strategy

Most investors utilize a bridge loan for real estate investment as a tactical entry point rather than a long-term solution. Icon Capital facilitates a seamless transition into a 30-year DSCR loan once the property reaches stabilization and is occupied by tenants. This internal handoff eliminates the need to source a new lender, which often saves investors 1.5% to 2.5% in redundant origination and processing fees. By keeping both phases under one roof, you maintain continuity and can execute a cash-out refinance more efficiently after the property value has increased through your capital improvements.

Start Your Application Today

Securing a rapid term sheet is the first step to making a competitive offer. To expedite your request, ensure you have your LLC operating agreement, recent property photos, and a detailed budget for any planned renovations ready for review. We provide clear, data-driven terms that you can include with your purchase contract to demonstrate financial strength to sellers. Our underwriters prioritize transparency, so you know exactly what your leverage looks like before you commit. Request a professional mortgage quote from Icon Capital to see your leverage options and start your next acquisition.

Maximize Your 2026 Acquisition Strategy

Success in the 2026 market requires moving faster than traditional banks allow. A bridge loan for real estate investment provides the 12 to 24 month window needed to acquire, renovate, or stabilize assets before permanent financing becomes viable. These instruments solve the immediate liquidity gap for properties that don’t yet meet conventional standards. By leveraging creative financing, you can secure assets today while competitors wait on 45-day underwriting cycles.

Icon Capital specializes in these high-stakes transitions. We manage specialized Non-QM products for self-employed investors and foreign nationals who often face 30% higher rejection rates at traditional retail banks. Our platform ensures a seamless transition into DSCR long-term financing once your asset’s cash flow is established. This methodical approach minimizes your capital’s downtime and maximizes your leverage across every stage of the deal. You’ve got the vision to spot the opportunity; we’ve got the technical expertise to fund it.

Request a Quote for Your Next Bridge Loan

Frequently Asked Questions

Is it hard to qualify for a bridge loan for real estate investment?

Qualifying for a bridge loan for real estate investment is generally faster and less restrictive than conventional financing. Icon Capital focuses on the property’s Loan-to-Value (LTV) ratio and Debt Service Coverage Ratio (DSCR) rather than just personal debt-to-income. Most deals require a minimum 660 credit score and 25% equity. We prioritize the asset’s potential to generate cash flow or its post-renovation value. This flexibility helps investors close deals that banks often reject.

What are the typical interest rates for bridge loans in 2026?

Interest rates for 2026 typically range between 8.5% and 11.5% depending on the asset class and borrower experience. These rates reflect a 200 to 400 basis point spread over the Secured Overnight Financing Rate (SOFR). Investors with a track record of 5 or more successful exits often secure rates at the lower end of this spectrum. Pricing remains competitive for high-quality multi-family and residential transition projects throughout the fiscal year.

Can I get a bridge loan with a low credit score?

You can secure a bridge loan with a credit score as low as 600 if the deal has strong collateral. Lower scores usually require a reduction in leverage, often capping the LTV at 60% or 65% to offset risk. We look at the liquidation value of the property and your exit strategy. If the asset shows a 1.25 DSCR, the credit score becomes a secondary factor. This allows sub-prime borrowers to leverage high-equity opportunities.

How long does it take to close a bridge loan with Icon Capital?

Icon Capital closes most bridge loans within 7 to 14 business days. We issue a formal term sheet within 48 hours of receiving your initial property data and credit authorization. Our streamlined four-step process eliminates the bureaucratic delays found at traditional banks. This speed allows investors to compete in high-demand markets where sellers require 15-day closing windows to accept an offer. Rapid execution is our primary advantage in the current lending environment.

What is the difference between a bridge loan and a hard money loan?

Bridge loans typically fund properties that are closer to stabilization and offer terms of 12 to 36 months. Hard money loans focus on distressed assets requiring heavy renovation with shorter 6 to 12 month durations. While both use the asset as collateral, bridge financing often carries lower interest rates than traditional hard money. Icon Capital provides both structures based on the specific capital needs of your project. Each product serves a distinct phase of the investment lifecycle.

Do I need to show my personal income tax returns for a bridge loan?

You don’t need to provide personal income tax returns for most of our bridge programs. We utilize Non-QM and DSCR-based underwriting that focuses on the property’s gross rental income or its current market value. This approach is ideal for self-employed investors who show high expenses on their tax filings. We require a simple application, a credit report, and a recent appraisal to move to the funding stage. This documentation style accelerates the approval process significantly.

What happens if I can’t sell or refinance the property before the bridge loan term ends?

Failing to exit the loan by the maturity date results in default interest rates or foreclosure. Most bridge contracts include an option for a 6-month extension if you pay an extension fee, usually ranging from 1% to 2% of the principal balance. You must request this extension 30 days before the loan expires. Proactive communication with our asset management team is vital to restructure the debt. We aim to find solutions that prevent property loss for our clients.

Can foreign nationals apply for an investment bridge loan in the US?

Foreign nationals can apply for a bridge loan for real estate investment with a valid passport and proof of international liquid assets. We typically cap the LTV at 65% for non-resident borrowers to mitigate cross-border risk. You’ll need to provide 12 months of debt service reserves in a US-based bank account. This program allows international investors to scale their US portfolios without a domestic credit history. It remains a popular option for buyers from Canada and Europe.