Why should a $500,000 tax write-off disqualify you from a $4 million property acquisition in 2026? Retail lenders continue to rely on outdated underwriting that penalizes business owners for maximizing their tax efficiency. You’ve likely felt the frustration of an automatic rejection despite having significant liquid capital. A Bank Statement Home Loan bridges this gap by focusing on actual cash flow rather than adjusted gross income.

We agree that traditional mortgage requirements are ill-suited for the modern entrepreneur. You shouldn’t have to choose between a lower tax bill and a new primary residence. This article promises to show you how to leverage 12 or 24 months of business deposits to secure high-balance financing without the intrusive requests for tax transcripts. We’ll break down the specific LTV thresholds, credit requirements, and the streamlined submission process used to close $4M+ loans in under 21 days. You’ll learn exactly how to bypass rigid retail standards and use your business’s real-time liquidity to scale your real estate portfolio.

Key Takeaways

- Identify why maximizing tax deductions creates a qualification gap and how to overcome traditional underwriting hurdles.

- Master the mechanics of the Bank Statement Home Loan to secure financing using 12 to 24 months of verified cash flow.

- Evaluate the strategic advantages of personal versus business bank statement reviews to optimize your loan-to-value (LTV) ratios.

- Implement a professional documentation strategy to segregate expenses and demonstrate the fiscal discipline required for Non-QM approval.

- Navigate Icon Capital’s efficient four-step process to structure and close complex loans tailored to high-net-worth self-employed profiles.

The Self-Employed Mortgage Gap: Why Traditional Underwriting Fails in 2026

Traditional mortgage underwriting relies on a framework built for the 1970s labor market. It prioritizes W-2 employees with predictable, static paychecks. By 2026, the American workforce has shifted significantly. Data shows that over 60 million Americans now participate in the freelance economy. These professionals often earn substantial revenue but don’t fit the narrow checkboxes of conventional lenders. A Bank Statement Home Loan bridges this gap by focusing on liquidity and cash flow rather than taxable income. It’s a premier Non-QM product designed for the modern entrepreneur.

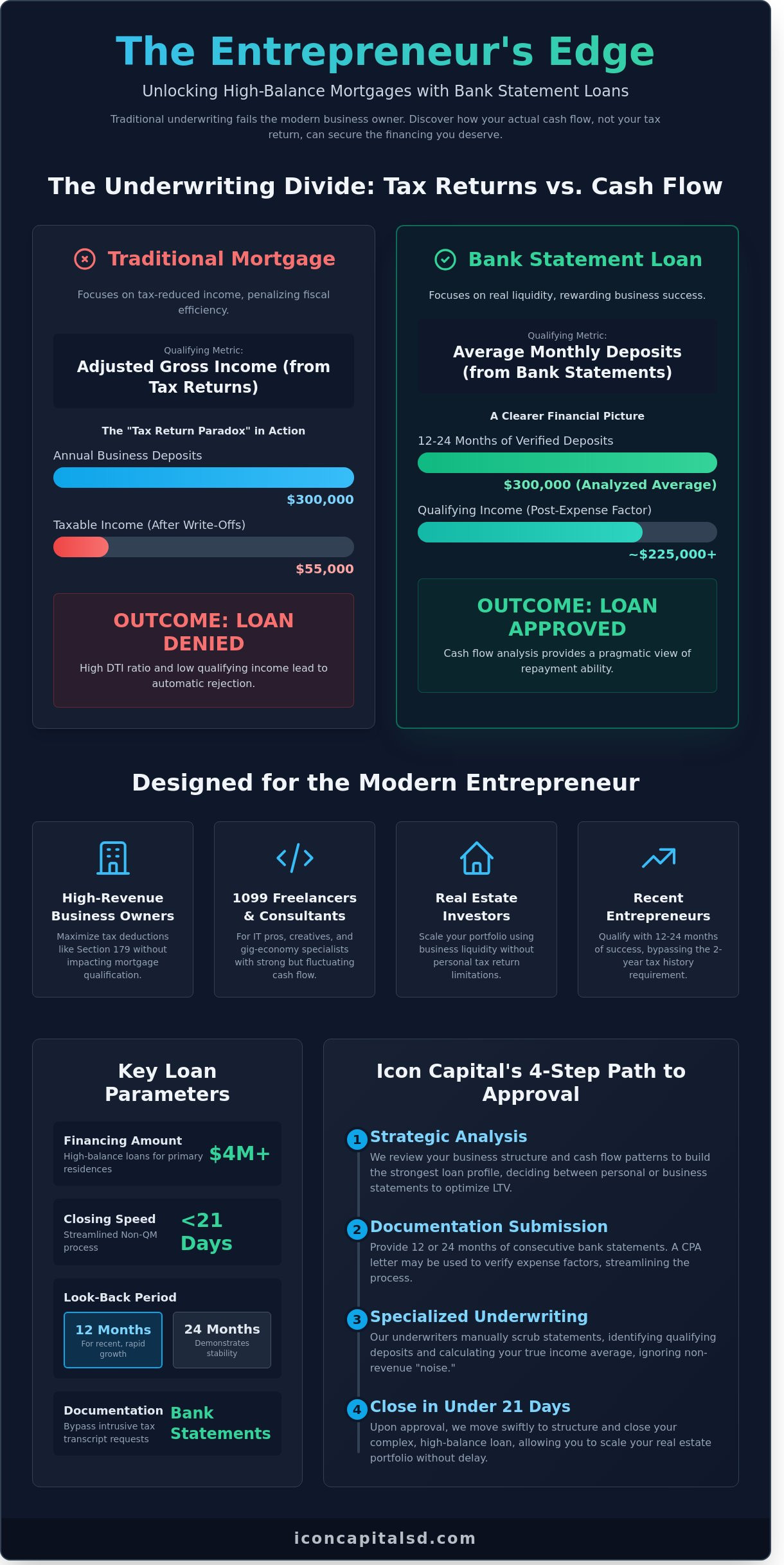

The “Tax Return Paradox” is the primary obstacle for self-employed borrowers. To manage a business efficiently, owners maximize legal deductions like Section 179 depreciation and mileage. While this strategy is fiscally responsible, it reduces the “net income” shown on Page 1 of a Form 1040. A consultant might generate $300,000 in annual deposits, but after aggressive write-offs, their tax return might only show $55,000 in qualifying income. Understanding Self-Employment dynamics is essential because traditional underwriters see the $55,000 figure and reject the loan, ignoring the $245,000 used for business growth and lifestyle.

Market volatility in 2026 requires more agile lending structures. Conventional loans are too slow and rigid to handle the fluctuating income cycles of 1099 contractors or seasonal business owners. We use 12 to 24 months of personal or business bank statements to calculate a true qualifying income average. This provides a pragmatic view of a borrower’s ability to repay without the distortion of tax-motivated accounting.

The Limitations of Conventional Agency Loans

Fannie Mae and Freddie Mac operate under strict government-sponsored enterprise (GSE) guidelines. These agencies typically cap debt-to-income (DTI) ratios at 43% to 45%. When an underwriter uses a tax return that has been heavily depreciated, the DTI often skyrockets past 60%, leading to an immediate denial. Conventional loans also require a two-year history of tax filings. If a business owner had a single “down” year due to capital investment in 2024, that data point drags down their qualifying average for the next 24 months. Non-reimbursed business expenses further erode purchasing power in the eyes of agency lenders, even if the borrower has $200,000 in liquid reserves.

Who Benefits Most from Bank Statement Financing?

This financing model serves specific cohorts who are underserved by retail banks. The Bank Statement Home Loan is the standard for:

- High-Revenue Business Owners: Individuals with $1 million plus in gross receipts who utilize heavy depreciation to offset tax liabilities.

- 1099 Freelancers: Creative professionals, IT consultants, and gig-economy specialists with strong cash flow but no traditional pay stubs.

- Real Estate Investors: Professionals looking to scale portfolios who don’t want their personal tax returns to limit their leverage.

- Recent Entrepreneurs: Business owners with 12 to 24 months of successful operation who cannot yet provide the two-year tax history required by big-box banks.

We focus on the actual capital moving through your accounts. If your business is healthy and your deposits are consistent, you shouldn’t be penalized for having a smart tax preparer. We prioritize the reality of your bank balance over the technicalities of a tax transcript.

Mechanics of Qualifying: How Underwriters Analyze Your Cash Flow

Underwriting for a Bank Statement Home Loan hinges on verifiable cash flow rather than taxable income. Lenders typically request 12 or 24 months of consecutive statements to establish an income average. The 12-month option provides a faster snapshot for businesses with recent growth. A 24-month history often secures more competitive pricing by demonstrating long-term business stability. Underwriters differentiate between personal and business accounts during the initial review. Using personal statements often allows for a 100% deposit credit. Business accounts require an expense factor adjustment to account for operational costs.

Qualifying deposits must represent actual revenue generated by the business. Underwriters manually scrub statements to remove “noise” such as credit line draws, transfers from other owned accounts, or one-time insurance settlements. These loans fall outside standard Qualified Mortgage (QM) rules; this allows for a specialized analysis of bank deposits instead of 1040 forms. A CPA letter serves as a critical verification tool in this process. It confirms the borrower has owned the business for at least 2 years and provides a professional estimate of the business expense ratio. This letter prevents the underwriter from defaulting to the most conservative assumptions during the calculation phase.

Calculating Qualifying Income and Expense Factors

The 50% default is the industry-standard expense factor for business bank statements. If a business generates $50,000 in monthly deposits, the underwriter assumes $25,000 is net income. However, service-based industries like consulting or digital marketing often operate with lower overhead. A third-party P&L statement can override the 50% default. If a CPA verifies a 20% expense ratio, the qualifying income jumps to $40,000. This adjustment significantly increases the maximum loan amount available to the borrower. You can structure your loan based on these specific industry reductions to maximize leverage.

Asset and Credit Requirements for Non-QM Approval

Non-QM programs require specific credit and liquidity benchmarks to offset the lack of traditional documentation. A 720 FICO score generally unlocks 90% LTV options for a Bank Statement Home Loan. Borrowers with scores near 660 usually face a 20% down payment requirement. Reserves are essential for approval. Lenders often require 6 to 12 months of PITIA (Principal, Interest, Taxes, Insurance, and Association dues) in liquid accounts. This “skin in the game” proves the borrower can handle market fluctuations without a W-2 safety net. All down payment funds must be sourced and seasoned in a verifiable account for at least 60 days prior to closing.

- 12-Month Review: Best for businesses with a recent upward trajectory in revenue.

- 24-Month Review: Ideal for established businesses seeking the lowest possible interest rates.

- Excluded Credits: Tax refunds, disaster relief grants, and inter-account transfers are deducted from total deposits.

- Reserve Thresholds: Most programs require at least 6 months of liquid reserves for loans exceeding $1 million.

Evaluating the Deal: Rates, LTV, and Opportunity Cost

Non-QM pricing operates on a different risk scale than agency debt. Expect a Bank Statement Home Loan to carry an interest rate 1% to 2.5% higher than a standard 30-year fixed conventional mortgage. Lenders price these products based on the manual underwriting required to verify cash flow. Loan-to-Value (LTV) ratios typically max out at 90% for primary residences and 80% for investment properties. Lower LTVs, such as 70%, often unlock the most competitive pricing tiers. While a conventional loan focuses on the bottom line of a tax return, Bankrate explains bank statement loans allow for a more expansive view of a borrower’s actual liquidity and gross deposits.

Investors must weigh this against other Non-QM tools. A Profit and Loss (P&L) loan requires a CPA-certified statement and is ideal for businesses with high overhead. Conversely, Debt Service Coverage Ratio (DSCR) loans ignore personal income entirely, focusing only on the property’s rental yield. The bank statement model remains the most popular for self-employed individuals who need to prove personal repayment capacity without sacrificing their tax deductions.

Structuring the Loan for Maximum Leverage

Success with a Bank Statement Home Loan depends on the structure. Interest-only payment options are a powerful tool for business owners. By paying only the interest for the first 10 years, you lower the monthly debt service; this keeps more capital available for business reinvestment or scaling a portfolio. Many borrowers select a 5-year or 7-year Adjustable-Rate Mortgage (ARM). These function as a tactical bridge. Since most homeowners refinance or sell within 6 years, paying a premium for a 30-year fixed rate is often an unnecessary expense. Be aware that investment-purpose loans frequently include prepayment penalties. These usually range from 1% to 3% of the loan balance if you exit the deal within the first 3 years.

Bank Statement Loans vs. Conventional Comparison

The primary advantage of Non-QM is speed and qualifying logic. A complex conventional file for a business owner with multiple K-1s can take 60 to 90 days to clear underwriting. We close bank statement deals in 21 to 30 days because the documentation is streamlined. The income calculation is the biggest differentiator. Conventional lenders use Taxable Net Income, which is your profit after every possible deduction. We use the Bank Statement Average, which looks at your total deposits. This often results in a qualifying income figure that is 40% to 60% higher than what appears on a tax return. This increased paper income allows for higher leverage and the ability to scale a real estate portfolio much faster.

The real metric is opportunity cost. If a $750,000 property is appreciating at 4% annually, waiting two years to clean up tax returns for a lower rate costs you $61,200 in lost equity. Paying an extra 1.5% in interest costs roughly $11,250 over that same period. The math is clear. The cost of the loan is secondary to the cost of missing the deal. Using a Bank Statement Home Loan allows you to secure the asset today and capture the appreciation while your competitors are stuck in the documentation phase.

Documenting Your Cash Flow: A Professional Preparation Checklist

Securing a Bank Statement Home Loan requires a shift from traditional tax-based reporting to granular cash-flow analysis. Underwriters don’t look at your net income after deductions; they focus on the actual liquidity flowing through your accounts. To qualify, your documentation must be surgical in its precision. Preparation begins 3 to 6 months before the application to ensure the data reflects a stable, growing enterprise. Follow these four steps to build a file that meets Non-QM standards.

Lenders require a minimum of 12 months of statements, though 24 months often secures a lower interest rate. These must be 100% consecutive. A single missing month can halt the underwriting process for 14 days while the gap is sourced. Ensure every page of every statement is included, even the blank ones or those containing only marketing text. Underwriters use these to verify that no undisclosed transfers or large withdrawals occurred during the period.

Step 2: Segregating Personal and Business Expenses

Fiscal discipline is a primary metric for risk assessment. If you use your business account to pay for personal groceries or a $3,500 home mortgage, underwriters will struggle to calculate an accurate expense ratio. Aim for a 0% commingling rate. Lenders typically apply a default 50% expense ratio to your total deposits. If your actual business expenses are lower, such as 20% for a consulting firm, you’ll need clear segregation to prove your higher qualifying income.

Step 3: Securing a CPA or Tax Preparer Letter

A formal letter from a licensed professional validates the existence and health of your business. This document must confirm three specific data points: your ownership percentage (usually 25% or more), the length of time the business has been active (minimum 2 years), and that the business is currently in good standing. This letter serves as the bridge between your bank data and the legal reality of your company.

Step 4: Preparing a Business Narrative for Large Deposits

Any deposit exceeding 25% of your average monthly revenue will trigger an inquiry. You must have a narrative ready for these spikes. If you received a $50,000 payment for a completed contract in October, keep the underlying invoice and contract ready. Underwriters need to know these aren’t personal loans or one-time windfalls that won’t recur.

Common Red Flags in Bank Statement Underwriting

NSF occurrences are the fastest path to a loan denial. Most Non-QM programs allow a maximum of 3 NSF events in a 12-month period. If you have 4 or more, you’ll likely need to wait 90 days for the oldest one to fall off the look-back period. Declining deposit trends also cause concern. If your June through August deposits are 15% lower than the previous quarter, be prepared to provide a 12-month P&L statement to prove the dip is seasonal rather than a sign of business failure.

The Submission Package: Speeding Up the Underwriter

Efficiency in the Non-QM space is driven by technology. Submit your statements as 300 DPI, OCR-compatible PDFs rather than scanned images. This allows the underwriter’s software to instantly extract data points, often reducing the initial review time from 72 hours to less than 24. Ensure your business license is current and reflects an “Active” status on the Secretary of State’s website. A Letter of Explanation is the ultimate tool for clarifying complex deposit histories, providing context that raw data cannot convey alone.

Ready to leverage your actual earnings for your next property? View our Bank Statement Home Loan programs to see which documentation path fits your business structure.

Structuring Your Loan with Icon Capital: The 4-Step Process

Icon Capital LLC eliminates the friction inherent in traditional lending by prioritizing liquid cash flow over tax-reported income. We specialize in Non-QM products for high-net-worth individuals who require speed and high leverage. Our process is designed to be transactional and efficient, moving from initial data collection to funding without the typical delays of a retail bank. We focus on the mechanics of the deal to ensure your capital is ready when you need it.

The “Structure Loan” phase involves a deep dive into your liquidity. For a Bank Statement Home Loan, we evaluate 12 or 24 months of business or personal deposits to calculate a realistic debt-to-income ratio. This isn’t a surface-level review; we analyze seasonal fluctuations and expense factors to maximize your borrowing power. By correctly structuring the file at the outset, we ensure the loan meets the specific criteria of our private capital partners, often securing approvals for borrowers with 700+ credit scores at competitive market rates.

Efficiency defines the “Submit Loan” phase. We operate with a direct-to-underwriter pipeline that removes unnecessary intermediaries. When a file moves to submission, it’s already been vetted against rigorous internal standards. This proactive approach leads to a 95% pull-through rate from submission to clear-to-close. We focus on the data that matters: your assets, your credit, and your property’s value. You won’t deal with the automated rejection systems common at big-box banks.

The final stages focus on getting “Cash in hand.” We understand that in competitive markets, a 30-day close is often too slow. Our team works to hit 15 to 21-day closing windows for well-documented files. This allows you to execute your real estate strategy with the certainty that the capital will be there when the deed is ready to transfer. We provide the leverage you need to scale your portfolio without the headache of traditional documentation.

Our Non-Traditional Mortgage Portfolio

Icon Capital LLC provides a comprehensive range of products that go beyond standard agency limits. We integrate our Bank Statement Home Loan options with specialized DSCR programs for investors and Foreign National programs for international buyers. We regularly facilitate loan amounts exceeding $2 million, providing the leverage needed for luxury markets. To understand your specific borrowing capacity based on current market data, Request a Quote to see your specific qualifying numbers today.

Why Investors and Brokers Choose Icon Capital LLC

Professional investors and brokers choose us because we’re solution-oriented. We don’t get bogged down by the complexities of LLCs, S-Corps, or multi-tiered partnerships. While 60% of traditional lenders struggle with non-standard ownership, we treat these structures as the norm. You’ll deal directly with decision-makers who understand how to navigate complex asset distributions. We prioritize the mechanics of the deal, ensuring every stakeholder has the data they need to move forward without unnecessary bureaucracy.

- Direct access to Non-QM underwriters

- Loan amounts up to $2 million and beyond

- Flexible documentation for complex business owners

- Aggressive timelines for fix-and-flip or buy-and-hold strategies

Leverage Your Cash Flow for 2026 Acquisitions

Traditional underwriting models continue to overlook the actual liquidity of high-earning self-employed professionals. In 2026, a Bank Statement Home Loan serves as the primary tool to bridge the gap between tax-optimized returns and real estate acquisition. Icon Capital functions as a specialist in the Non-QM space, providing access to high-balance loans exceeding $2 million. Our 4-step submission-to-close process eliminates the typical roadblocks found in legacy banking systems by focusing on logic-based underwriting rather than rigid checklists.

By analyzing 12 to 24 months of business deposits, we prioritize your actual buying power over bottom-line taxable figures that don’t reflect your true wealth. We’ve refined our internal systems to ensure that complex cash flows are documented accurately and efficiently. It’s time to utilize your business success to secure the high-value assets you need. Our team is ready to structure your next deal with precision and speed. Explore your creative financing options and request a custom quote today to see how we can put your capital to work. We look forward to helping you scale your portfolio.

Frequently Asked Questions

How many months of bank statements are typically required for a home loan?

Lenders typically require 12 or 24 months of consecutive bank statements to verify income for a bank statement home loan. Using 24 months of data often provides a more stable income average, which can lead to better pricing or higher LTV limits. Underwriters review these statements to calculate a monthly average based on total qualifying deposits minus a standard expense factor.

Can I get a bank statement loan with a 10% down payment?

You can secure a bank statement mortgage with a 10% down payment if you have a credit score of 720 or higher. Most Non-QM programs cap the Loan-to-Value (LTV) at 90% for primary residences. If your credit score falls below 680, expect the down payment requirement to increase to 20% or 25% to offset the lender’s risk.

Is the interest rate significantly higher for a bank statement mortgage?

Interest rates for a bank statement home loan are generally 1.00% to 2.00% higher than standard 30-year fixed conventional rates. This premium accounts for the manual underwriting and increased risk profile of self-employed borrowers. Your final rate depends on your specific credit score and the chosen LTV, with 80% LTV often triggering the most competitive pricing tiers.

What is a qualifying deposit in the eyes of a Non-QM underwriter?

A qualifying deposit is any credit to the account that represents legitimate business revenue or earned income. Underwriters exclude non-revenue items like credit line draws, transfers between accounts, or tax refunds to ensure the income calculation is accurate. In a typical 12-month review, 100% of personal deposits or 50% of business deposits are counted as qualifying income.

Do I still need to provide my tax returns if I use the bank statement program?

You don’t need to provide any federal or state tax returns when applying for this specific Non-QM program. The bank statement home loan is designed specifically for borrowers who have legal deductions that reduce their taxable income. The underwriter relies solely on your bank statements and a Profit and Loss statement to determine your ability to repay.

Can I use business bank statements if I only own 25% of the company?

Most lenders require at least 50% ownership to use business bank statements, but some programs allow 25% ownership with a CPA letter. The CPA must verify your ownership percentage and confirm that your personal use of business funds won’t negatively impact the company’s operations. If you own less than 25% of the entity, you’ll likely need to use personal bank statements instead.

What industries are typically subject to higher expense factors?

Industries with physical inventory or heavy equipment, such as construction or retail, often face a 70% to 80% expense factor. Conversely, service-based professionals like consultants or software developers might qualify for a 20% expense factor. Underwriters apply these percentages to your total deposits to estimate net income unless you provide a detailed, CPA-prepared P&L.

How long does it take to close a bank statement home loan compared to a conventional one?

Closing a bank statement loan typically takes 21 to 30 days, which is comparable to the 25-day average for conventional financing. The primary delay usually stems from the initial income analysis phase. Providing clear, PDF-format statements for all 12 or 24 months during the first 48 hours of the application can accelerate the process and help meet tight closing deadlines.