A $5 million liquidity position should carry more weight than a standard W-2, yet traditional lenders still prioritize debt to income ratios over actual net worth. For high net worth individuals and business owners, the standard 43% DTI threshold often acts as a barrier rather than a benchmark. You’ve likely found that your tax strategy, while efficient for wealth preservation, makes it nearly impossible to prove qualifying income to a conventional underwriter. It’s a common paradox where high liquidity leads to loan denials because of low taxable earnings. Asset Qualification Home Loans solve this by focusing on your balance sheet instead of your paystub.

We’ll show you how to leverage your existing capital to secure high balance financing without invasive employment verification. This article details the specific mechanics of asset depletion and the 1:1 asset to loan coverage ratios required for qualification. You’ll learn how to use this Non-QM solution to acquire real estate quickly. It’s time to convert your liquid wealth into a powerful financing tool that bypasses the constraints of traditional mortgage underwriting.

Key Takeaways

- Learn how to secure high-balance financing by leveraging liquid net worth in place of traditional employment or income documentation.

- Understand the mechanics of Asset Qualification Home Loans and how they replace standard DTI ratios with an asset-to-debt coverage model.

- Compare asset qualification against asset depletion strategies to select the most efficient financing path for your specific financial profile.

- Identify the essential eligibility benchmarks, including minimum FICO scores and post-closing liquidity requirements for high-asset programs.

- Discover how to accelerate your timeline by utilizing Icon Capital LLC’s expertise in structuring and submitting complex non-QM loans within days.

What is an Asset Qualification Home Loan?

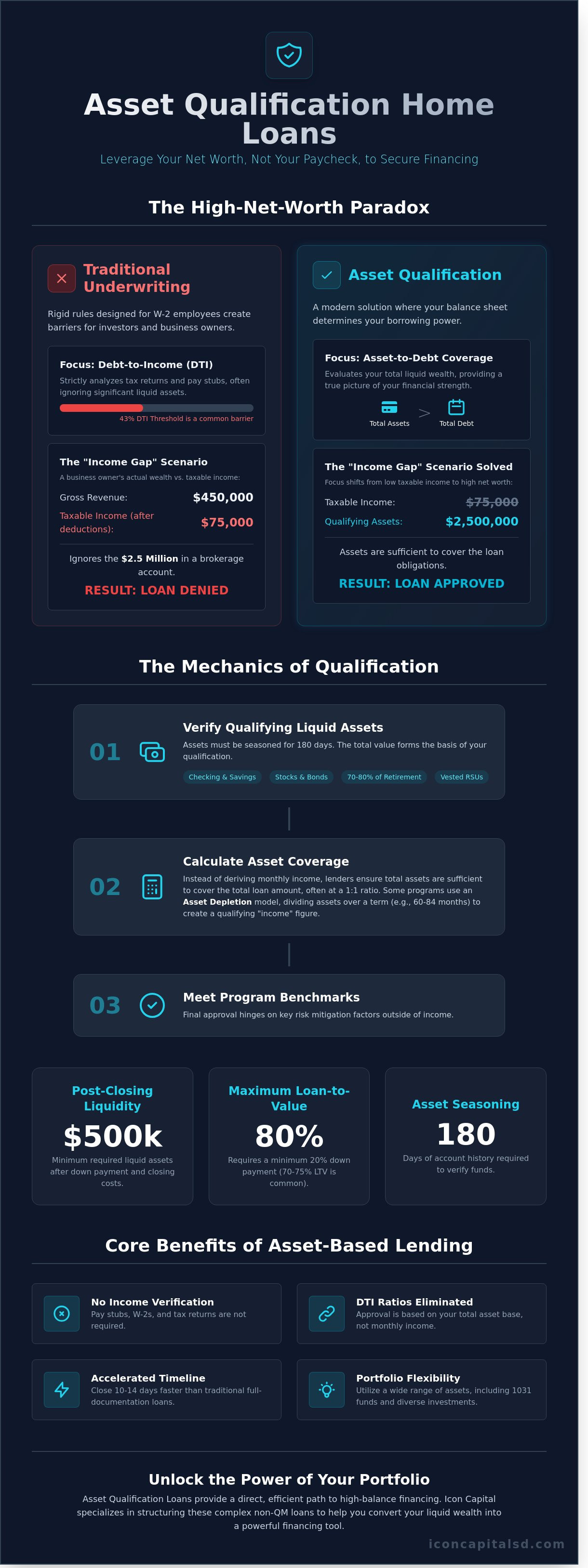

Asset Qualification Home Loans represent a specialized Non-QM financing category where a borrower’s eligibility is determined by their total liquid wealth rather than traditional monthly paychecks. This program allows high-net-worth individuals to leverage their existing capital to secure a mortgage without providing tax returns or W-2 forms. As of January 2026, market data indicates that approximately 12% of luxury home buyers now opt for asset-based structures to avoid the complexities of traditional income verification. These loans operate on the principle of asset-based lending, where the strength of your portfolio serves as the primary security for the credit extension.

The primary shift in this model is the replacement of the standard Debt-to-Income (DTI) ratio with an asset-to-debt coverage calculation. Instead of looking for a stable salary, underwriters analyze the total value of qualifying assets such as checking accounts, savings, stocks, bonds, and 70% to 80% of retirement account balances. They then divide this total by a specific timeframe, typically 60 or 84 months, to derive a “qualifying income” figure. This approach is specifically designed for the 2026 economic environment, where asset appreciation often outpaces fixed salary growth for the top 5% of earners. It’s a pragmatic solution for retirees, venture-backed entrepreneurs, and investors who maintain millions in securities but show minimal taxable income on paper.

The Problem with Traditional Underwriting

Standard Fannie Mae and Freddie Mac guidelines are built for the W-2 employee. This rigid framework excludes roughly 18% of qualified borrowers who don’t fit the traditional mold. Business owners often face the “Income Gap” where legal tax strategies and heavy deductions reduce their reported taxable income to levels that don’t reflect their actual purchasing power. For instance, a consultant might generate $450,000 in gross revenue but report only $75,000 after expenses. A traditional bank would deny this loan immediately, ignoring the $2.5 million sitting in the borrower’s brokerage account. Traditional lenders simply don’t have the internal protocols to evaluate complex, multi-layered portfolios or non-traditional liquidity sources.

Core Benefits of Asset-Based Qualification

Asset-based lending removes the friction points common in conventional mortgage applications. By focusing on what you own rather than what you earn, the process becomes significantly more transparent and objective.

- No Income Verification: You don’t need to provide pay stubs, 1099s, or tax returns to prove your ability to repay.

- DTI Elimination: The approval hinges on your total liquid reserves. Your monthly debt obligations are weighed against your total asset base, not a fluctuating monthly income stream.

- Accelerated Timeline: Documentation requirements are minimal. By removing the need for 24 months of income history and employer verifications, we typically close these loans 10 to 14 days faster than full-doc alternatives.

- Flexibility: We accept a wide range of asset classes, including 1031 exchange funds, vested RSUs, and diverse investment portfolios that traditional underwriters often ignore.

This streamlined methodology ensures that liquidity is the only metric that matters. It’s a direct, efficient way to secure high-balance financing without the administrative burden of traditional banking requirements.

How Asset Qualification Works: The Mechanics of Liquidity

Traditional mortgage underwriting relies on tax returns and W-2s to prove repayment ability. Asset Qualification Home Loans pivot this requirement toward verified liquidity. Non-QM lenders follow the Ability to Repay (ATR) rule established by the Dodd-Frank Act, but they use a borrower’s balance sheet instead of a paystub to satisfy it. While the official definition of a mortgage focuses on the property as collateral, asset-based lending focuses on the borrower’s total capital as the primary source of security.

Institutional non-QM investors typically set a $500,000 minimum threshold for post-closing liquidity. This benchmark ensures the borrower maintains a substantial cash cushion after the down payment and closing costs are paid. Risk mitigation is further managed through the Loan-to-Value (LTV) ratio. Most asset-based programs cap the LTV at 80%, though 70% or 75% is more common for high-balance loans. This 20% to 30% equity position protects the lender against market volatility while reducing the borrower’s monthly debt obligation.

Fund verification requires strict seasoning. Underwriters demand 180 days of account history to confirm the stability of the assets. Large deposits appearing within the last 60 days must be sourced and documented to ensure they aren’t “gifted” funds or temporary loans used solely for qualification. This six-month lookback period provides a clear picture of the borrower’s average daily balance and financial habits.

Accepted Asset Types and “Haircut” Rules

Lenders don’t value all assets equally. Underwriters apply “haircuts” to certain accounts to account for market fluctuations and withdrawal penalties. Checking and savings accounts are the gold standard; they receive 100% valuation because the cash is immediately accessible and stable. Brokerage accounts, including stocks, bonds, and mutual funds, usually receive a 70% to 80% valuation. This discount protects the lender if the stock market drops during the loan term.

Retirement accounts like 401ks and IRAs are subject to stricter rules. If the borrower is under age 59.5, lenders typically only count 60% to 70% of the balance. This reduction accounts for the 10% federal early withdrawal penalty and potential tax liabilities. For borrowers over age 59.5, the valuation may increase to 80% because the penalty no longer applies. You can review specific asset guidelines to see how your portfolio measures up.

Calculating the Asset Coverage

Determining eligibility involves a specific coverage formula. The underwriter takes the total qualified assets, applies the necessary haircuts, and compares the result to the total loan amount plus 60 months of recurring debt. Recurring debt includes the new mortgage payment, property taxes, insurance, and any personal liabilities like car loans or credit cards. If the net assets exceed this sum, the borrower qualifies.

Primary residence loans often require additional reserves. Underwriters look for 6 to 12 months of PITI (Principal, Interest, Taxes, and Insurance) to remain in the account after the deal closes. This ensures the borrower isn’t “house poor” and has sufficient runway to manage the property. The 2026 asset coverage ratio is defined as the total value of qualified liquid assets divided by the aggregate of the loan amount and 60 months of all recurring debt obligations.

Asset Qualification vs. Asset Depletion: Choosing Your Strategy

Borrowers often confuse asset depletion with asset qualification. These strategies serve different financial profiles. Asset depletion acts as a bridge for those who almost meet conventional Debt-to-Income (DTI) standards. It converts liquid wealth into a theoretical monthly paycheck to satisfy traditional underwriting. Asset qualification is a total departure from income-based metrics. It focuses on your total liquid net worth to determine your ability to repay the debt without ever calculating a DTI ratio.

When to Use Asset Depletion

Asset depletion works best for retirees or self-employed individuals who show low taxable income but maintain high cash reserves. Lenders use a specific formula to create “income” from your assets. They take the total value of eligible accounts and divide them by a set term, usually 360 months for a 30-year loan. If you hold $1,500,000 in a brokerage account, the lender adds $4,166 to your monthly qualifying income. This strategy is ideal for:

- Borrowers who are just a few hundred dollars short of meeting a 43% DTI limit.

- Conforming loan products where the borrower wants to stay within Fannie Mae or Freddie Mac guidelines.

- Individuals with significant 401(k) or IRA balances who don’t want to trigger early withdrawal penalties.

The Superiority of Asset Qualification

For high-net-worth investors, Asset Qualification Home Loans provide a more direct path to capital. This method eliminates the need for employment history, tax returns, or 1099s. Icon Capital evaluates your liquidity rather than your cash flow. We verify that your total liquid assets exceed the loan amount, closing costs, and 60 months of debt service reserves. This approach allows for significantly higher leverage than traditional methods.

Icon Capital supports loan amounts up to $4,000,000 through this program. We provide flexibility that retail banks cannot match, including financing for non-warrantable condos and primary residences. The process is streamlined because the underwriter doesn’t have to verify business P&L statements or corporate structures. We look at the bank statements, verify the source of funds, and move to closing.

Choosing Asset Qualification Home Loans often results in a faster closing timeline. Since the documentation requirements are minimal, the “processing” phase of the loan is cut by 50% compared to a full-documentation jumbo loan. Investors who need to move quickly on a property to beat out cash buyers find this speed essential for winning bids in competitive markets.

Interest rates for these products reflect the specialized nature of the risk. You can expect a rate spread of 0.75% to 1.25% above standard conforming rates. While the monthly cost is higher, the long-term financing benefit comes from the ability to keep your capital invested in the market. If your portfolio returns 8% annually, paying a 7.5% mortgage rate while keeping your $2,000,000 invested is more profitable than liquidating assets to buy a home with cash. This strategy maximizes your internal rate of return while providing the liquidity needed for future acquisitions.

For investors focused on maximizing their portfolio’s rate of return, exploring avenues beyond public stocks can be crucial. Platforms like Pre-IPO Hype offer a way to connect with high-growth private companies, providing another potential strategy for wealth appreciation.

Eligibility Checklist for Asset Qualification Home Loans

Qualifying for Asset Qualification Home Loans requires a shift from income-based metrics to balance-sheet strength. To secure these terms, you must meet specific liquidity and credit benchmarks that protect the lender’s interest. A 700 FICO score is the standard floor for high-asset programs. This number isn’t arbitrary; it signals to underwriters that you have a consistent history of debt management. While traditional loans might flex down to a 620 score, asset-based lending requires higher credit confidence because the primary repayment source is a finite pool of capital rather than a recurring salary. If your score sits at 690, you might face higher interest rates or be required to increase your down payment by an additional 10% to offset the perceived risk.

Post-closing liquidity is the second pillar of eligibility. You must maintain a safety net after the down payment and closing costs are paid. Most programs require 6 to 12 months of reserves. For example, on a $1.2 million loan with a $7,500 monthly payment, you should expect to show at least $90,000 in liquid accounts remaining after the deal closes. This ensures the mortgage stays current even during market fluctuations or personal transitions. Lenders want to see that the transaction doesn’t leave you “house poor” or unable to manage emergency expenses.

Sourcing and seasoning are non-negotiable. Lenders typically look back 60 to 90 days to verify the origin of your funds. Large deposits that don’t match your typical financial activity must be documented with a clear paper trail. This prevents the use of “gifted” funds that are actually undisclosed loans. These Asset Qualification Home Loans are available for a variety of property types, provided they meet specific LTV (Loan-to-Value) caps:

- Primary Residences: 1-4 unit properties with LTVs up to 80% for well-qualified borrowers.

- Second Homes: Vacation properties in established markets, often requiring a 75% LTV.

- Investment Properties: Non-owner occupied units where the focus is on portfolio growth and long-term equity.

Credit and Financial History Standards

Lenders enforce a 5-year seasoning rule for major credit events. If you’ve experienced a bankruptcy, foreclosure, or short sale, 60 months must have passed before you’re eligible for these specialized programs. Your 12-month housing history must be pristine, meaning zero 30-day late payments. Current debt obligations, such as an $800 monthly auto lease or a $3,000 secondary mortgage, will be subtracted from the monthly asset depletion calculation, which directly impacts your total borrowing power.

Documentation Requirements

You’ll need to provide 180 days of consecutive bank and brokerage statements. Underwriters review every page to ensure consistency and identify any undisclosed liabilities. Non-liquid assets like 401(k)s or IRAs are often utilized for secondary qualification, though they’re usually valued at 70% of their current market balance to account for potential tax hits and market volatility. To get an accurate assessment of your portfolio’s qualifying value, contact Icon Capital to verify your specific asset mix. Our team analyzes your holdings to structure a loan that leverages your wealth efficiently.

Ready to leverage your assets for your next purchase? Request a custom quote from Icon Capital today.

Leveraging Asset Qualification with Icon Capital

Icon Capital specializes in structuring Asset Qualification Home Loans for borrowers who possess substantial liquidity but lack standard W-2 documentation. Traditional lenders often reject 1099 professionals or retirees because their tax returns show heavy deductions or complex corporate structures. We focus on the current market value of your brokerage accounts, retirement funds, and cash reserves. Our team understands that for a high-net-worth individual, a tax return is a strategy for efficiency, not a definitive measure of wealth. We prioritize your liquid net worth to determine your ability to repay, bypassing the restrictive debt-to-income ratios that stall most bank applications.

Speed is a core metric at Icon Capital. We move from the initial deal structure to submission in 48 to 72 hours. While 85% of retail banks take 45 days or longer to process a standard mortgage, our internal workflow is built for the 2024 real estate market where timing is everything. Our specialists analyze your asset statements immediately; we don’t wait for a third-party processor to flag issues weeks into the transaction. This aggressive timeline allows our clients to compete with cash buyers by offering a guaranteed, rapid closing window.

Our investor-first mindset dictates how we handle every file. We recognize that liquidity is the ultimate proof of financial stability. If you have $2 million in a managed account, that capital is more reliable than a paycheck that could disappear tomorrow. We don’t ask for two years of tax history or profit and loss statements. Instead, we use a clear asset depletion formula to calculate a qualifying monthly income. This pragmatic approach ensures that your capital works for you, allowing you to secure a primary residence or investment property without liquidating your portfolio and triggering unnecessary capital gains taxes.

The Icon Capital Loan Process

The process begins with a specialized asset review. Your dedicated specialist examines your liquid net worth, including stocks, bonds, and 401k accounts, to determine the optimal loan structure. Within 24 hours, we provide a rapid pre-approval based on these verified figures. The final stage involves efficient underwriting where we clear conditions based on asset verification rather than income-based delays. Most of our Asset Qualification Home Loans close in 15 to 21 days.

Scaling Your Portfolio

Utilizing asset-based lending is a strategic move for portfolio growth. It allows you to keep your primary income sources off the application, which preserves your borrowing capacity for other ventures. You can achieve maximum leverage by following these strategies:

- Free up cash flow by using assets to qualify for lower rates than hard money alternatives.

- Combine asset-based qualification with DSCR programs to maximize leverage on a 75% or 80% LTV basis across multiple properties.

- Maintain your investment positions while using your portfolio’s value to secure real estate.

Icon Capital provides the expertise needed to navigate these non-traditional paths. We focus on the mechanics of the deal to ensure you get the leverage you need without the paperwork you don’t. Ready to explore your options? Request a quote today.

Maximize Your Borrowing Power with Icon Capital

Traditional lending models often fail to account for the financial reality of high-net-worth individuals and self-employed professionals. Asset Qualification Home Loans solve this by focusing on your balance sheet rather than tax returns or pay stubs. This strategy prioritizes liquidity and verified assets to determine borrowing power; it provides a streamlined path for those with significant capital but non-traditional income streams. Icon Capital specializes in these Non-QM solutions, offering direct, expert-led underwriting that cuts through standard bureaucratic delays. We facilitate loan amounts up to $4 million, ensuring your capital works as hard as you do. Our team understands the mechanics of creative financing and the specific requirements of complex portfolios. You don’t need to fit into a traditional box to secure competitive terms on your next investment or primary residence. Take the next step in scaling your real estate portfolio with a partner who values your actual net worth. We’re ready to help you secure the funding you need based on the wealth you’ve already built.

Get a custom Asset Qualification Loan quote from Icon Capital

Frequently Asked Questions

Can I get an asset qualification loan if I am currently unemployed?

Yes, you can qualify for an asset-based loan while unemployed. Icon Capital evaluates your total liquid assets rather than your current employment status or W-2 income history. Typically, you must demonstrate enough liquidity to cover 100% of the loan amount or show assets that cover all monthly debt obligations for 60 months. This makes it a viable solution for retirees or high-net-worth individuals between professional ventures.

What is the minimum amount of assets required for this program?

Minimum asset requirements vary by program, but most lenders require at least $500,000 in qualifying liquid assets. For a standard asset depletion model, we look for enough liquidity to cover the new mortgage, all existing debts, and 6 to 12 months of cash reserves. Asset qualification home loans prioritize the total value of your portfolio over monthly cash flow statements or traditional pay stubs.

Do retirement accounts like a 401k count toward qualification?

Retirement accounts like 401ks and IRAs count toward your total qualification, though they’re subject to a specific valuation haircut. Most underwriters value these accounts at 60% to 80% of their current balance to account for potential tax penalties and market volatility. If your 401k has a balance of $1,000,000, we generally credit $700,000 toward your qualifying asset total to ensure conservative risk management.

Is a down payment still required for an asset-based home loan?

A down payment is required, typically ranging from 20% to 30% of the purchase price. While you’re using assets to qualify for the monthly payments, the LTV ratio must remain within non-QM guidelines. For a $1,000,000 property, expect to bring at least $200,000 to the closing table to secure the most competitive terms available in the current 2024 lending market.

How do interest rates for asset qualification loans compare to traditional mortgages?

Interest rates for asset qualification home loans are generally 1.00% to 2.00% higher than traditional Fannie Mae or Freddie Mac products. This premium accounts for the increased risk associated with non-documented income. If a standard 30-year fixed rate is 6.5%, an asset-based loan might start at 7.5% or 8.5% depending on your credit score and the total LTV of the deal.

Can I use this program for an investment property or just a primary residence?

You can use this program for primary residences, second homes, and 1 to 4 unit investment properties. For investment deals, we often pivot to DSCR models, but asset qualification remains a powerful tool for investors with high liquidity but low taxable income. Most borrowers use this for properties valued between $500,000 and $5,000,000 to maximize their leverage without providing tax returns.

What does “seasoning” mean in the context of asset-based lending?

Seasoning refers to the amount of time your funds have been held in a verified account, usually requiring a 60 to 90 day history. Underwriters review two to three months of consecutive statements to ensure the funds didn’t appear as a sudden, unexplained deposit. Large deposits must be sourced with clear documentation to be included in your total qualifying balance for the loan.

Are there any maximum loan limits for asset-qualified borrowers?

Maximum loan limits typically reach $3,000,000, though larger amounts are possible for exceptionally well-capitalized borrowers. These limits far exceed standard conforming loan caps, which sit at $766,550 for single-family homes in most 2024 markets. High-net-worth individuals often use these larger limits to acquire luxury real estate without liquidating their entire investment portfolio, allowing their capital to remain invested in the market.