In the 2026 real estate market, the difference between a 22% annualized return and a forfeited deposit isn’t your renovation budget; it’s your speed to close. Traditional lenders often require 40 days to process a loan, frequently rejecting the distressed assets that offer the highest margins. You’ve likely seen deals fall through because a bank wouldn’t clear a property with a damaged foundation or outdated electrical. Successfully flipping houses with hard money requires a shift from viewing interest rates as a cost to viewing leverage as a tool for scale. Speed is your primary competitive advantage against cash buyers.

This guide will show you how to master the mechanics of private capital to fund your fix and flip projects faster and more profitably. You’ll learn the exact liquidity benchmarks required for a 90% LTC loan and how to navigate draw schedules to keep your contractors on site. We provide a clear framework for calculating deal profitability with 12% interest rates and 2 points, ensuring you maintain a healthy spread. We’ll move straight into the technical requirements for securing fast funding and managing construction holdbacks in the current market.

Key Takeaways

- Identify why asset-based bridge financing is the essential tool for securing distressed properties that traditional lenders typically decline.

- Master the mechanics of LTV versus LTC and draw schedules to maximize your leverage when flipping houses with hard money.

- Analyze the opportunity cost of “cheap money” to understand how higher-rate financing can actually yield a higher total annual profit.

- Utilize the 2026 underwriting checklist to ensure your deal math aligns with the updated 70% rule and current liquidity standards.

- Learn how to scale your investment portfolio by leveraging creative financing solutions and transitioning from fix-and-flip projects to long-term wealth.

What is Hard Money and Why is it Essential for Flipping Houses?

Hard money is asset-based financing secured by real property. It functions as a short-term bridge loan, typically with a duration of 12 to 18 months. Unlike conventional bank loans, hard money focuses on the collateral value rather than the borrower’s personal income. Investors use this capital to acquire and renovate distressed assets quickly. Understanding Hard money loan basics is the first step for any serious investor looking to scale their portfolio.

Traditional FHA and conventional mortgages are incompatible with distressed properties. Most retail lenders require a certificate of occupancy and a functional kitchen or roof before funding. If a property requires a $50,000 gut renovation, a bank will reject the application immediately. Flipping houses with hard money bypasses these bureaucratic hurdles. It allows you to purchase properties that don’t meet strict secondary market guidelines, such as those with structural issues or outdated electrical systems.

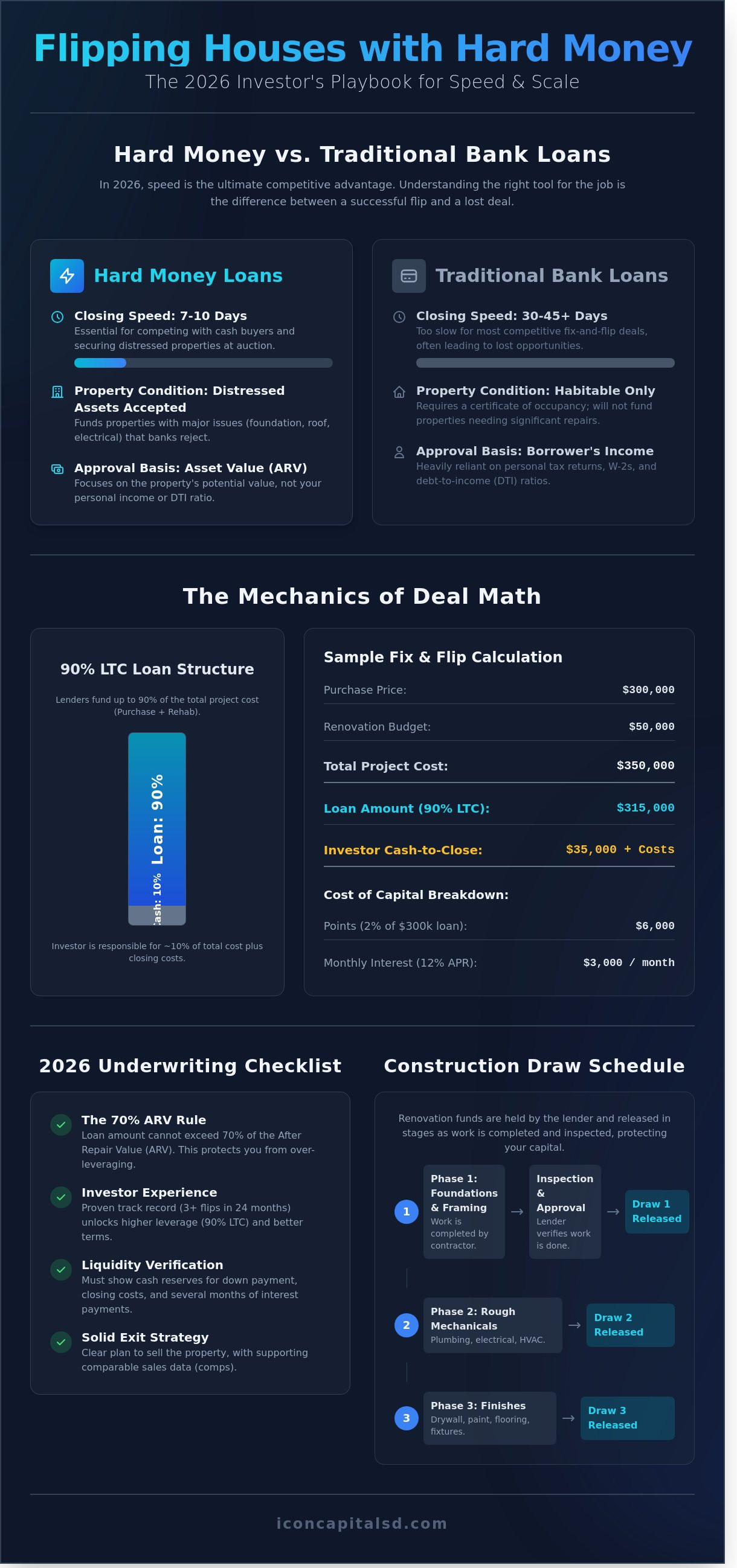

In the competitive 2026 real estate market, speed is the primary currency. Traditional mortgage processing takes 30 to 45 days, which is far too slow for distressed property auctions or short sales. Hard money lenders can often close in 7 to 10 business days. This speed allows investors to compete with cash buyers and secure off-market deals that would otherwise be lost to slower competitors. Closing fast gives you the leverage to negotiate lower purchase prices from motivated sellers.

Hard money underwriting also serves as a secondary layer of deal protection. A professional lender won’t fund a project if the numbers don’t work. We analyze the renovation budget and projected exit strategy to ensure the deal remains profitable. If the loan to value (LTV) or after repair value (ARV) doesn’t align with current market data, the lender provides a necessary reality check. This oversight protects the investor from over-leveraging on a bad asset.

Hard Money vs. Private Money: Key Differences

Hard money comes from institutional firms with standardized processes. Private money usually originates from individual acquaintances or family members. Institutional hard money offers professional draw schedules and clear legal term sheets. This structure ensures that renovation funds are released on time. Private individuals often lack the liquidity or professional oversight required for a 6 month project. Standardized draws protect the project timeline by ensuring contractors are paid only after specific milestones are met.

The Asset-Based Lending Philosophy

Asset-based lending prioritizes the property’s ARV over the borrower’s debt-to-income ratio. In 2026, the industry has shifted toward experience-based lending. Investors with 3 successful exits in 24 months often receive 90% of the purchase price. This enables scaling without providing tax returns or income verification. Flipping houses with hard money ensures your borrowing capacity isn’t limited by your personal paycheck. Your credit score matters less than your track record and the quality of the asset.

The Mechanics of Hard Money: Deal Math and Draw Schedules

Success in flipping houses with hard money starts with a precise understanding of the capital stack. In 2026, most private lenders evaluate deals using two primary ratios: Loan-to-Value (LTV) and Loan-to-Cost (LTC). While LTV measures the loan against the final value, LTC focuses on the total project cost, including purchase price and renovation. Most institutional hard money products currently cap at 90% LTC or 75% of the After Repair Value (ARV). If a property costs $300,000 to buy and $50,000 to fix, a 90% LTC loan provides $315,000, requiring the investor to bring $35,000 plus closing costs to the table.

Flippers must focus on the total cost of capital over a 6 to 9-month window. APR is a misleading metric in this niche because it annualizes costs that are only carried for a fraction of the year. Instead, calculate the points and monthly interest. If you pay 2 points on a $300,000 loan, that is $6,000 paid at closing. At a 12% interest rate, your monthly interest-only payment is $3,000. These are fixed transaction costs that must be factored into your exit strategy. For a deeper dive into these structures, check out Hard Money for Fix and Flips to see how professional investors weigh these costs against potential profits.

Your “Cash-in-Deal” requirement isn’t just the down payment. It includes the 10% to 20% equity injection, closing costs which usually range from 2% to 5%, and the liquidity needed to fund the first phase of construction. Lenders often require 6 to 12 months of interest reserves in your bank account before they clear a file for closing. This ensures the project doesn’t stall if your personal cash flow dips during the renovation phase.

The construction holdback is the portion of the loan reserved specifically for repairs. This money isn’t handed over at the closing table. It stays in an escrow account managed by the lender. You only gain access to these funds through a structured draw process as specific milestones are met. This protects the lender’s collateral and ensures the renovation actually happens according to the submitted scope of work.

Mastering the Draw Schedule

Most lenders use a 100% reimbursement model for renovations. You must pay your contractors for the first $15,000 or $20,000 of work out of your own pocket. Once that phase is complete, you request a draw. An inspector verifies the work, and the lender releases the funds to reimburse you. Project stalls happen when investors lack the “float” money to bridge the gap between paying a crew and receiving the draw. Keep at least 15% of your total renovation budget in liquid cash to maintain momentum while waiting for inspections to clear.

Calculating ARV (After Repair Value)

ARV is the projected market value of a property after all renovations are completed. Lenders use a “Subject-To” appraisal to determine this number, which differs from an “As-Is” appraisal that only looks at the current distressed state. This valuation relies on 2026 market comps within a 0.5-mile radius of the subject property. If the neighborhood median price for a renovated home is $450,000, your ARV cannot be $550,000 without significant justification. You can structure your loan based on these specific valuation metrics to maximize your leverage and ensure the deal remains profitable.

Hard Money vs. Traditional Financing: An Opportunity Cost Analysis

Traditional financing creates significant liquidity constraints. Most conventional lenders only provide 80% LTV on the purchase price and zero capital for renovations. This leaves the investor out of pocket for 100% of the repair costs. If a project requires $65,000 in structural and cosmetic upgrades, that capital is locked in the asset for the duration of the flip. Flipping houses with hard money changes the math. Specialized lenders often fund 90% of the purchase and 100% of the construction budget via a draw schedule. This preserves your cash reserves and allows you to maintain a safety net for unexpected permit delays or material price spikes.

- Closing Speed: 7-10 days (Hard Money) vs. 45-60 days (Conventional)

- Down Payment: 10-20% of total project cost vs. 20-25% of purchase only

- Documentation: Asset-based focus vs. intensive personal income verification

- Renovation Funding: Included in the loan wrap vs. out-of-pocket cash

The Velocity of Capital

When NOT to Use Hard Money

Efficiency is the hallmark of a professional flipper. You aren’t just buying real estate; you’re buying time and access. Traditional banks focus on your past tax returns, while hard money lenders focus on the future value of the deal. When you prioritize total deal volume over interest percentages, you move from being a hobbyist to a high-volume operator.

The 2026 Hard Money Underwriting Checklist

Underwriting in 2026 requires a data-heavy approach that prioritizes equity protection. Successful investors flipping houses with hard money still rely on the 70% rule as a baseline. This formula dictates that your maximum purchase price should be 70% of the After Repair Value (ARV) minus the total renovation costs. In the current high-cost environment, this 30% margin is necessary to absorb the 12% to 14% cost of capital and the 6% in commissions during the eventual sale. If your acquisition price exceeds this threshold, the deal likely lacks the safety cushion required for an 80% Loan to Cost (LTC) approval.

Borrower liquidity is the second pillar of the checklist. You must prove you have “skin in the game” before a lender will issue a commitment letter. Most hard money programs require 15% to 25% of the total project cost to be held in liquid reserves. These funds aren’t just for the down payment; they ensure you can cover the first renovation draw out of pocket. Lenders typically verify these assets through 60 days of bank statements to ensure the capital is seasoned and not sourced from another high-interest loan.

The Scope of Work (SOW) has become a primary focus for 2026 underwriters. A vague budget is a fast way to get a rejection. Your SOW must be a line-item breakdown with specific quotes for major systems like HVAC, roofing, and structural foundations. Lenders now look for a 10% to 12% contingency fund built into the SOW to handle fluctuating material prices. They also verify that your contractor is licensed and insured in the specific jurisdiction where the property is located.

Your exit strategy must be dual-pathed to satisfy modern risk assessments. While the primary goal is usually a retail sale on the MLS within 180 days, you must also demonstrate a viable “Plan B.” This involves showing the property can refinance into a long-term Debt Service Coverage Ratio (DSCR) loan. If the projected market rent doesn’t cover the new mortgage payment at a 1.20x ratio, the deal is considered high-risk. Underwriters will check if local inventory exceeds a 4-month supply before approving a flip-only strategy.

Preparing Your Loan Application Package

When flipping houses with hard money, your track record serves as your primary negotiating tool. Investors with 5 or more successful exits in the last 24 months often see interest rates 1.5% lower than novices. Your package must include the executed purchase contract, the detailed SOW, and entity documents like your LLC Operating Agreement or Corporate Bylaws. Providing a clear “Experience Resume” with photos and HUD-1 statements from previous deals will accelerate the process. Request a professional quote to see your specific eligibility based on your current portfolio and experience level.

Common Red Flags for Hard Money Lenders

Lenders flag deals with unrealistic ARV projections that ignore 2026 market realities. If your comparable sales are older than 90 days or located more than 0.5 miles from the subject property, the valuation will be challenged. Another red flag is an incomplete budget that ignores “soft costs.” These expenses, including builder’s risk insurance, city permits, and property taxes, can account for 7% of your total project cost. Finally, a lack of a secondary exit strategy suggests a lack of market awareness. If the property cannot cash flow as a rental, the lender sees no way to get paid if the retail market shifts.

Ready to secure funding for your next project? Apply for a hard money loan with Icon Capital today.

Scaling Your Portfolio with Icon Capital Solutions

Scaling a real estate business requires more than just finding the next property; it requires a structural partner capable of providing consistent liquidity. While beginners often start by flipping houses with hard money from local private individuals, professional investors reach a ceiling with those “country club” lenders. Local individuals often lack the capital depth to fund five or ten concurrent projects. Icon Capital LLC provides the institutional leverage necessary to move past single-deal limitations. We offer up to 90% Loan-to-Cost (LTC) and 100% of renovation funding, allowing you to keep your liquid reserves for new acquisitions rather than sinking them into a single job site.

Professional investors choose institutional debt because it offers standardized underwriting and predictable timelines. You don’t have to wait for a private lender to “check their bank account” before a closing. In Q1 2025, data indicated that 68% of high-volume flippers transitioned to institutional partners to secure 10-day closing cycles. This speed is a competitive advantage in markets where sellers prioritize certainty of execution. Icon Capital LLC focuses on the asset’s exit strategy and your track record, utilizing creative financing and Non-QM products that traditional banks won’t touch. We prioritize the mechanics of the deal, ensuring your leverage is optimized for maximum cash-on-cash returns.

- High Leverage: Access up to 90% LTC to minimize your initial capital outlay.

- Predictable Draws: Faster inspection turnarounds mean your contractors stay on schedule.

- Portfolio Cross-Collateralization: Use equity in existing assets to fund new down payments.

- Non-QM Flexibility: We don’t require the tax returns or debt-to-income ratios that stymie traditional bank loans.

Beyond the Flip: DSCR and Bridge Loans

The most successful investors don’t just flip; they pivot. Transitioning from a fix-and-flip model to a long-term wealth strategy involves moving equity into a DSCR long-term rental. A bridge loan provides the initial 12-month window to acquire and stabilize a property. Once the renovation is complete, you can refinance into a 30-year fixed loan based on the property’s rental income rather than your personal salary. Icon Capital LLC supports this transition by offering 5-8 unit multi-family financing, filling the gap between residential and large-scale commercial lending. This allows you to scale from single-family homes to small apartment buildings without changing lenders.

Your Next Move in the 2026 Market

Anticipated market shifts in 2026 suggest that inventory turns will hover around 42 days in high-growth corridors. To stay profitable, you must move from deal identification to final funding with surgical precision. Reliability is the ultimate currency. When you’re flipping houses with hard money, your reputation with wholesalers and agents depends on your ability to close. Icon Capital LLC streamlines this by providing a clear, four-step process: structure the loan, submit documentation, underwrite the asset, and fund the deal. We eliminate the narrative-driven delays common in the mortgage industry, focusing instead on the 1.20x DSCR or the 75% After-Repair Value (ARV) that makes the deal work. Don’t let a slow lender cap your growth. Get your deal funded with Icon Capital LLC and secure the leverage you need to dominate your local market.

Scale Your 2026 Real Estate Portfolio

Success in the 2026 market requires more than just finding the right property; it demands a sophisticated approach to leverage. Mastering the 70% ARV rule and managing technical draw schedules ensures your liquidity stays intact across multiple projects. Flipping houses with hard money is the primary vehicle for investors to outpace traditional financing and secure high-margin deals quickly. Icon Capital Solutions provides the specialized infrastructure needed to grow, offering distinct programs for 1-4 and 5-8 unit properties. Our underwriting team focuses on the deal’s fundamentals rather than personal debt-to-income ratios. We offer no-income verification options specifically for self-employed investors who need fast, professional execution. Whether you’re targeting a single-family renovation or a multi-unit conversion, we provide the capital and expertise to close your deal. Get a custom Fix & Flip loan quote for your next deal today. Your next successful exit starts with the right capital partner.

Frequently Asked Questions

Is hard money a good idea for a first-time house flipper?

Hard money is an effective tool for first-time investors because it prioritizes asset value over borrower experience. While traditional banks often require a 2-year history of successful flips, hard money lenders focus on the 70% After Repair Value (ARV) threshold. Flipping houses with hard money allows new flippers to secure properties that don’t meet conventional habitability standards. This focus on the deal’s potential rather than the borrower’s resume is vital for entry-level investors.

What are the typical interest rates for hard money in 2026?

Interest rates for hard money in 2026 are projected to fluctuate between 10% and 13% based on current market liquidity. Most deals also include 2 to 4 points paid at the time of closing. These rates reflect the short-term, high-risk nature of bridge financing used for rapid acquisition and renovation. Investors should budget for these costs to ensure their net profit margins remain above 15% on every project.

How much cash do I need to flip a house with a hard money loan?

You generally need 10% to 25% of the purchase price in liquid cash to close the deal. Lenders typically fund 75% to 90% of the acquisition cost and 100% of the renovation budget. For a $300,000 purchase, expect to bring $30,000 to $75,000 plus an additional 3% to 5% for closing costs and reserves. This liquidity ensures you can cover interest payments during the 6 to 12-month hold period.

Do hard money lenders check my personal credit score?

Lenders typically require a minimum FICO score of 620 to 660 to ensure financial responsibility. While the property’s value is the primary collateral, your credit history impacts the LTV and interest rate. Borrowers with scores above 740 often secure the most competitive 10% interest rates and lower point structures. If your score is below 600, you’ll likely need a larger down payment or a partner with stronger credit.

What happens if I cannot sell the house before the hard money loan is due?

If the term expires, you can typically negotiate a 3-month or 6-month extension for a fee of 1% to 2% of the loan balance. Another option is transitioning into a 30-year DSCR loan if you decide to hold the property as a rental. Failure to pay or extend results in default interest rates often exceeding 18%. It’s essential to communicate with your lender 30 days before the maturity date.

Can I use hard money to buy a house I plan to live in?

You cannot use hard money to buy a primary residence because these loans are strictly for non-owner-occupied, business-purpose investments. Federal regulations like the Dodd-Frank Act impose strict consumer protection requirements on primary residence loans that hard money products don’t meet. These loans are designed for flipping houses with hard money or purchasing rental units. Using these funds for a home you live in violates the loan’s legal structure.

How fast can I get a hard money loan approved?

Hard money loans typically reach approval within 24 to 48 hours of receiving a complete application. Funding usually occurs within 7 to 10 days once the title work and appraisal are finalized. This speed is 4 times faster than traditional mortgage timelines, which often exceed 45 days. Rapid funding allows investors to beat out competitors who rely on slow, conventional financing for their acquisitions.

What is a draw schedule and how does it work?

A draw schedule is a pre-negotiated timeline that releases renovation funds in 4 to 6 stages as work is completed. After finishing a specific phase, such as rough-in plumbing or roofing, you request an inspection. The lender then releases the funds within 3 to 5 business days, minus a $150 to $250 inspection fee. This process ensures the renovation stays on track and the lender’s collateral is protected throughout the project.