Your tax professional’s success in reducing your 2025 liability is exactly what’s killing your mortgage application at a retail bank. While traditional underwriters see a $250,000 write-off as a lack of income, we recognize it as strategic capital management. It’s a frustrating reality for the 16 million self-employed Americans who have the liquidity for a $3 million property but fail a standard debt-to-income ratio check. Finding Self-employed Home Loans shouldn’t mean compromising on your growth strategy. You shouldn’t have to wait 60 days for a generic rejection letter.

You deserve a financing partner who understands that business P&L statements tell a more accurate story than a 1040 form. This guide breaks down how to master the complexities of non-traditional mortgages and leverage your business assets to secure high-value financing without traditional tax returns. We’ll examine specific Non-QM structures and the streamlined documentation process that gets you to the closing table in 21 days or less. You’ll gain the technical knowledge needed to navigate 2026’s lending environment and secure the property your business success has earned.

Key Takeaways

- Identify why traditional tax returns restrict borrowing power and how bank statements or P&L programs reflect your true qualifying income.

- Leverage asset depletion models to convert business liquidity into monthly income for high-value financing without standard earnings proof.

- Navigate the 2026 underwriting roadmap to secure Self-employed Home Loans through specialized Non-QM and 1099 loan programs.

- Master the “Structure Phase” of the lending process to align your specific business entity with the most favorable loan terms and LTV ratios.

- Scale your real estate portfolio by utilizing DSCR loans that prioritize property cash flow over personal debt-to-income metrics.

The Tax Return Trap: Why Traditional Mortgages Fail the Self-Employed

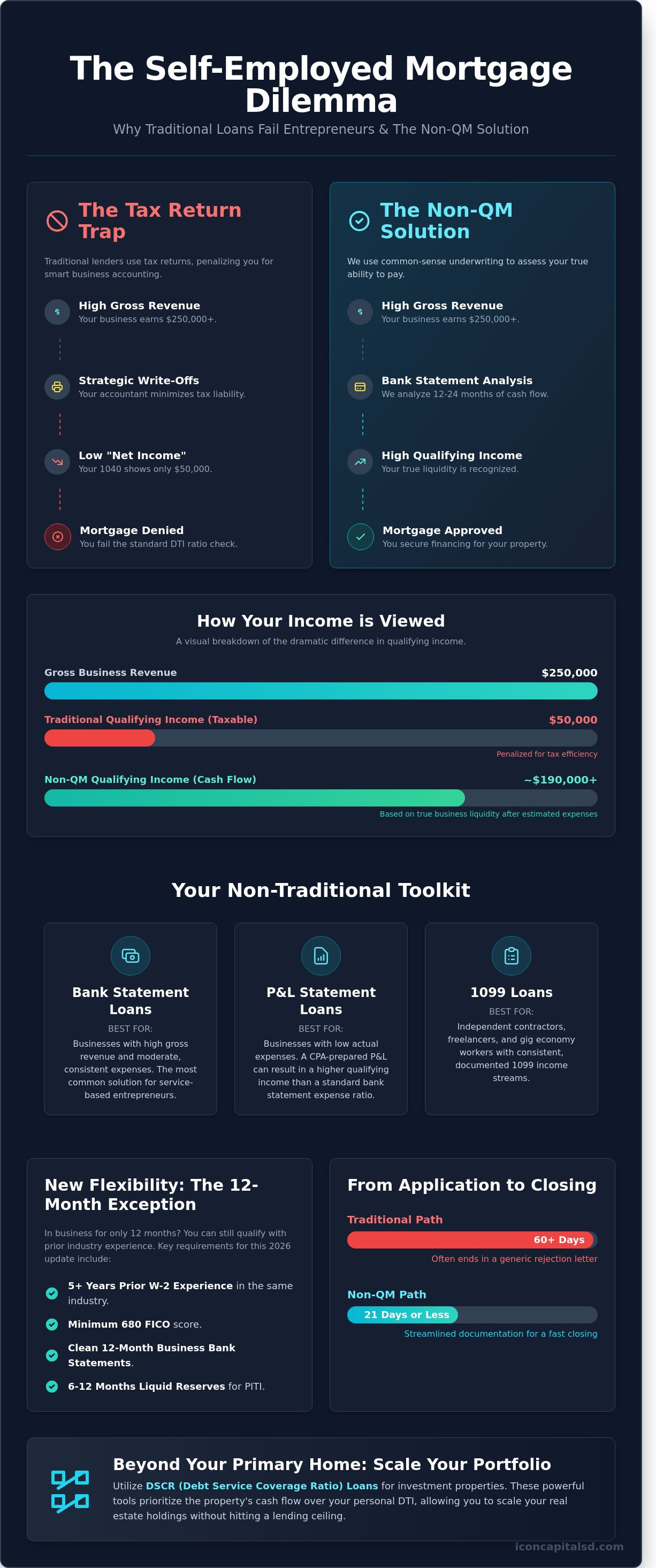

Tax optimization is the cornerstone of a successful business strategy. Entrepreneurs use legal deductions to minimize their taxable income, which preserves capital for growth and operations. However, this efficiency creates a direct conflict when applying for a mortgage. Traditional lenders use net income figures from tax returns to calculate debt-to-income (DTI) ratios. If your business earns $250,000 but your accountant reduces that to $50,000 in taxable income, a standard bank treats you as a low-earner. This disconnect makes Self-employed Home Loans a necessity for those who don’t fit the W-2 mold.

The standard mortgage underwriting process relies on three pillars: credit, capacity, and collateral. For capacity, Fannie Mae and Freddie Mac guidelines prioritize stable, predictable income streams. Even in 2026, these standards remain rigid. They’re designed for salaried employees with consistent paychecks, not for business owners with seasonal fluctuations or aggressive reinvestment strategies. This outdated framework ignores the entrepreneurial agility that defines the modern economy.

Current market conditions exacerbate these challenges. With average interest rates hovering around 7.2% in early 2026, borrowing power is already compressed. When you combine high rates with a deflated net income figure on a tax return, your maximum loan amount drops significantly. Non-QM (Non-Qualified Mortgage) products solve this by looking at cash flow rather than tax filings. These loans allow business owners to leverage their true gross income, ensuring they aren’t penalized for their financial sophistication.

Understanding the Non-QM Advantage

Non-QM loans are the primary vehicle for Self-employed Home Loans. These products exist outside the restrictive boundaries of government-backed lending. Because they’re funded by private capital, underwriters use common sense to evaluate a borrower’s ability to repay. Instead of tax returns, we analyze 12 or 24 months of bank statements to verify liquid cash flow. This shift from rigid documentation to logical asset evaluation allows for loan amounts up to $2 million or more, regardless of what your 1040 says.

The 2-Year Rule and Recent Exceptions

Lenders typically require a 24-month history of self-employment to prove income stability. However, 2026 market shifts have introduced more flexibility for newer business owners. If you’ve been in business for 12 months but have five years of prior experience in the same industry as a W-2 employee, many Non-QM programs will now accept your application. This industry-continuity rule recognizes that your earning potential didn’t reset just because you changed your tax status. Key requirements for these exceptions include:

- A minimum FICO score of 680 or higher.

- Documented prior experience in the same field.

- A clean 12-month business bank statement history.

- Sufficient liquid reserves to cover 6-12 months of mortgage payments.

By moving away from tax-dependent underwriting, Icon Capital LLC provides the leverage needed to secure high-value property. We focus on the reality of your business success, not the numbers your accountant prepares for the IRS. These creative financing solutions ensure that your path to homeownership isn’t blocked by the very strategies that make your business profitable.

The Non-Traditional Toolkit: Bank Statement, P&L, and 1099 Loans

Standard mortgage underwriting relies on taxable income, which creates a hurdle for the 16 million self-employed individuals in the United States who maximize legal tax deductions. Alt-Doc programs solve this by using actual cash flow to calculate qualifying income. Choosing the right pathway depends on your business structure and how you manage your revenue. Self-employed Home Loans through these channels prioritize liquidity over tax filings, allowing for a more accurate representation of your ability to repay.

Determining the highest qualifying income requires a side-by-side analysis of your gross receipts versus your net profit. Underwriters apply an “Expense Ratio” to bank statement applications to estimate business costs. For service-based businesses, this ratio might sit at 20%; however, for product-based businesses, it can climb to 50% or higher. If your actual expenses are lower than the industry standard, a P&L or 1099 program often yields a higher loan amount.

- Bank Statements: Best for businesses with high gross revenue and moderate expenses.

- P&L Statements: Ideal for businesses with low overhead or those that experienced a significant revenue spike in the last 6 months.

- 1099 Loans: The most efficient route for independent contractors, freelancers, and consultants who receive a steady stream of 1099-NEC forms.

Bank Statement Loans: Cash Flow as King

Lenders typically offer 12-month or 24-month bank statement programs. Opting for a 24-month look-back period can sometimes secure a lower interest rate or a higher LTV (Loan-to-Value) ratio, as it demonstrates long-term stability. When using business statements, underwriters often default to a 50% expense ratio. If you use personal statements, you can often qualify with 100% of your deposits, provided you can prove the business has a separate account for its expenses.

Watch out for common triggers that stall an approval. Most programs allow no more than 3 non-sufficient funds (NSF) occurrences in a 12-month period. Large, unexplained deposits that don’t align with your typical business activity will be backed out of the qualifying average unless you provide a clear paper trail. You can review specific qualifying criteria to see which statement type fits your current financial profile.

P&L Statement Mortgages: For Complex Business Structures

A Profit and Loss (P&L) statement mortgage allows you to bypass the granular scrutiny of 12 months of bank statements. Instead, a CPA or a licensed tax preparer provides a statement covering the last 12 to 24 months of business activity. This is particularly beneficial for seasonal businesses, such as landscaping companies or retail shops, where cash flow fluctuates wildly between January and July. It allows the underwriter to see the annualized health of the company rather than focusing on a single slow month.

The documentation requirements for these Self-employed Home Loans are specific. You must provide a CPA-signed P&L, a letter from your accountant verifying you’ve been in business for at least 2 years, and a valid business license. This program effectively “flattens” the volatility of your bank deposits, focusing instead on the net bottom line as verified by a third-party professional.

For consultants and 1099 earners, the 1099 loan is the cleanest path. Lenders simply take the gross amount from your 1099 forms and apply a flat expense factor, usually 10%. This removes the need for P&L statements or month-by-month bank analysis, making it the fastest closing option in the Non-QM space.

Asset Qualification: High-Net-Worth Solutions Without Income Proof

Asset Qualification is a method to leverage 100% of liquid reserves to offset zero-income tax filings. This financing strategy bridges the gap for individuals with substantial liquidity but minimal taxable income on their recent returns. For high-net-worth borrowers, traditional debt-to-income (DTI) calculations often fail to reflect true financial strength. The asset depletion model solves this by converting a liquid portfolio into a qualifying monthly salary. It’s a critical tool for retirees, venture-backed founders, and professional investors who maintain $500,000 or more in accessible funds.

Traditional banks focus on the bottom line of a 1040 tax return. If you’ve utilized legal deductions to minimize tax liability, your DTI ratio might look weak to a conventional underwriter. Asset-based lending ignores the tax return and prioritizes the balance sheet. This approach is essential for self-employed home loans because it values immediate liquidity over temporary cash flow fluctuations. Lenders recognize that a borrower with $2.5 million in brokerage accounts represents a low default risk, regardless of whether they receive a recurring paycheck.

Eligible assets for this program include:

- Personal checking and savings accounts, valued at 100% of the balance.

- Publicly traded stocks, bonds, and mutual funds, typically valued at 70% to 80% of their current market price.

- Vested retirement accounts like 401(k)s or IRAs, valued at 60% to 70% for borrowers over age 59.5.

- Business funds, provided the borrower owns 100% of the entity and can prove the withdrawal won’t impact operations.

Many clients ask why they must show a salary when they have millions in the bank. The answer lies in federal “Ability to Repay” (ATR) rules. Lenders must document a consistent source of funds to satisfy these regulations. By using the asset depletion model, the lender creates a “phantom” income stream that satisfies ATR requirements without forcing the borrower to liquidate their portfolio or change their tax strategy.

Calculating Your Asset-Based Income

The standard math involves taking your total qualifying assets, subtracting the down payment and six to twelve months of reserves, and dividing the remainder by 360 months. For example, if a borrower has $1.8 million in cash after the down payment, the lender credits them with $5,000 in monthly income. Equities receive a haircut to account for market volatility; a $1 million stock portfolio is often valued at $700,000 for qualification purposes. You can combine this calculated income with other revenue streams, such as 1099 earnings or rental profits, to maximize your leverage for self-employed home loans.

The Role of Credit Scores in Asset-Based Lending

A 700 FICO score functions as the gatekeeper for the most competitive asset-based programs. While specific Non-QM products allow scores as low as 660, the Loan-to-Value (LTV) ratios tighten significantly as scores decrease. At a 720 score, you can typically secure an 80% LTV. If the score drops to 680, the lender might require a 35% down payment to offset the perceived risk. These loans rely on the stability of the assets, but the credit score remains the primary indicator of a borrower’s financial character. Using assets as the primary driver allows for loan amounts up to $3.5 million without the need for a single paystub.

The 2026 Underwriting Roadmap: From Application to Closing

Securing Self-employed Home Loans in 2026 requires a methodical approach to data presentation. The process begins with pre-qualification, which utilizes a soft credit pull to evaluate your baseline eligibility without impacting your credit score. During this phase, an initial document review identifies the most viable income verification path. Most entrepreneurs fail here because they lack a cohesive summary of their business structure. By providing 12 to 24 months of bank statements or a preliminary tax transcript early, you allow the underwriter to calculate a qualifying income figure before you commit to a property contract.

The Structure Phase follows. This is where your specific business entity, whether it is a Single-Member LLC or a C-Corp, is matched with a specific loan product. In Q1 2026, data from the National Association of Realtors indicated that 38% of self-employed applications required a pivot from traditional Fannie Mae guidelines to Non-QM products to achieve the necessary leverage. This phase ensures your debt-to-income (DTI) ratio remains within the 43% to 50% threshold required for approval.

Processing and underwriting occur behind the scenes. The underwriter scrutinizes your year-to-date Profit and Loss (P&L) statement against your historical filings. If your 2025 revenue shows a variance exceeding 25% compared to your 2026 projections, you must provide a signed letter of explanation. The goal is to prove income stability. Once the underwriter satisfies all conditions, you receive the Clear to Close. Final verifications, including a verbal confirmation that your business is still active, typically happen within 48 hours of the scheduled funding date. This ensures the capital is deployed only when the risk profile remains unchanged from the initial application.

Preparing Your Financial ‘Story’

Your financial history is a data set that must remain consistent. Underwriters in 2026 prioritize a clean digital paper trail for every business transaction. Commingling personal and business funds is a primary reason for delays, often adding 10 to 14 days to the approval timeline. You should avoid major business equipment purchases or signing new 60-month vehicle leases within 6 months of your application. These new liabilities can drastically reduce your qualifying power. You can request a quote to see which ‘story’ fits your data and determine your maximum loan amount based on current liquid assets.

Navigating Appraisals and LTVs

Property type significantly dictates your required down payment and leverage. For a primary residence, you can often access a 90% Loan-to-Value (LTV). Investment properties are more restrictive, typically capping at 75% or 80% LTV. Creative financing strategies, such as utilizing interest-only periods or 40-year amortizations, will impact your final interest rate by 0.375% to 0.85% depending on your credit tier. In the volatile real estate market of March 2026, appraisals are conservative. If a valuation comes in 4% below the contract price, you must be prepared to bridge the gap with cash or renegotiate the purchase price. Managing the appraisal process requires proactive communication between your broker and the appraiser to ensure all business-use-of-home deductions are correctly accounted for in the property’s utility profile.

Scaling with Icon Capital: Specialized Loans for the Modern Entrepreneur

Icon Capital prioritizes the mechanics of the deal over the traditional profile of the borrower. Standard banks often stall when reviewing complex tax returns or fluctuating annual profits. We pivot away from these hurdles by focusing on asset performance and project viability. This approach is essential for high-growth business owners who utilize legal deductions that lower their taxable income. While a retail bank might see a high-risk applicant, we see a viable investment opportunity backed by tangible real estate value.

Our Debt Service Coverage Ratio (DSCR) programs allow you to scale your investment portfolio without presenting personal pay stubs. We typically look for a ratio of 1.20 or higher, meaning the property’s rental income covers 120% of the debt obligations. This metric empowers you to acquire multiple properties simultaneously because your personal debt-to-income ratio is no longer the primary bottleneck. We specialize in 5 to 8 unit properties and multi-family buildings. These assets fall into a niche that many residential lenders won’t touch and commercial banks over-complicate with excessive paperwork.

The Icon Capital advantage is built on direct communication and technical precision. You won’t deal with a generic call center. You work with specialists who understand the nuances of Non-QM lending and private capital. We analyze the numbers quickly to provide a clear path to funding. If you have been searching for Self-employed Home Loans that recognize your true financial strength, our asset-based logic provides the necessary leverage.

Beyond the Single-Family Home

Transitioning from a primary residence to a diversified portfolio requires specialized capital. Self-employed borrowers often use our Fix and Flip programs to capitalize on distressed inventory. We provide up to 90% Loan-to-Cost (LTC) and 100% of renovation funds, allowing you to preserve your business’s liquid cash for operations. Bridge loans serve as another critical tool; they offer short-term liquidity to seize market opportunities before permanent financing is secured. For international entrepreneurs, our Foreign National programs allow for U.S. property acquisition with as little as 30% down. These options require no U.S. credit history or domestic tax documentation, making the U.S. market accessible to global business owners. This flexibility ensures that your growth isn’t limited by your residency status or the complexity of your corporate structure.

Simplified Submission and Rapid Funding

We’ve stripped away the bureaucracy of the mortgage industry to create an efficient, 4-step pipeline designed for busy professionals. Our process is built for speed, often closing deals in 15 to 25 days, which is significantly faster than the 45-day industry average for traditional Self-employed Home Loans. You get direct access to decision-makers who speak your language, ensuring that “Non-QM jargon” never stands in the way of your progress.

- Structure: We analyze your specific scenario and select the optimal loan product based on your goals.

- Submit: You provide the minimal required documentation through our secure digital portal.

- Underwrite: Our technical team evaluates the asset and the deal structure for rapid approval.

- Close: Funds are disbursed, allowing you to move on to your next business objective.

Stop letting traditional lending constraints dictate your growth. We provide the technical expertise and the capital necessary to treat your real estate acquisitions like the business ventures they are. Ready to leverage your business success? Get your custom mortgage quote here.

Secure Your 2026 Property Assets

Traditional tax returns don’t reflect the actual liquidity of a modern business owner. By 2026, the industry shift toward Non-QM solutions allows entrepreneurs to bypass outdated requirements using bank statements, P&L statements, or 1099 records. Self-employed Home Loans now prioritize actual cash flow; enabling you to qualify for loan amounts up to $2 million based on your real-world assets rather than net taxable income. Icon Capital specializes in these creative financing structures, including DSCR and multi-unit investment loans for complex portfolios.

Our team uses a streamlined 4-step professional loan process to move your deal from initial structure to final closing. We provide the technical expertise needed to leverage high-net-worth solutions without the standard income proof required by retail banks. We focus on the mechanics of the deal to ensure your capital works as hard as your business does. It’s time to utilize the leverage your success has already earned.

Request a Creative Financing Quote to see how our data-driven approach can secure your next acquisition. You’ve built the business; let us provide the roadmap to your next home.

Frequently Asked Questions

Can I get a home loan if I’ve been self-employed for less than two years?

Yes, you can qualify with 12 months of self-employment history through specific Non-QM programs. While traditional lenders require 24 months, Icon Capital provides options for borrowers with a 1 year track record if they have 2 years of previous experience in the same industry. This flexibility allows entrepreneurs to secure self-employed home loans without waiting for a second tax filing or 1040 cycle.

What is the minimum credit score for a bank statement loan in 2026?

The minimum credit score for a bank statement loan in 2026 is 620. Most Non-QM lenders require a 660 score to access the highest LTV ratios of 80% or 90%. Scores below 620 typically trigger higher down payment requirements or lower debt-to-income limits. Maintaining a 720 score ensures you receive the most competitive pricing available in the current financial market.

Are interest rates significantly higher for self-employed home loans?

Interest rates for self-employed home loans are typically 0.5% to 1.5% higher than standard conventional rates. This premium accounts for the manual underwriting and increased risk associated with non-traditional income verification. Borrowers with a 25% down payment and a 740 credit score often see the smallest rate spread. These rates remain competitive compared to hard money alternatives and reflect 2026 market volatility.

Do I need to provide tax returns for an Asset Qualification loan?

You don’t need to provide tax returns for an Asset Qualification loan. These programs verify ability to repay based on liquid assets like cash, stocks, and retirement accounts rather than monthly income. We require a 100% coverage ratio where your total qualifying assets exceed the loan amount plus 6 months of reserves. This structure simplifies the process for high net worth individuals and business owners.

How much down payment is required for a Non-QM self-employed mortgage?

A 10% down payment is the minimum requirement for most Non-QM self-employed mortgage products. Most borrowers should prepare for a 20% down payment to avoid private mortgage insurance and secure better interest rates. If your credit score is below 680, lenders often mandate a 25% equity stake. This ensures the loan meets LTV requirements for non-traditional financing structures and reduces lender risk.

Can I use a P&L statement from my own software, or does it need a CPA?

Most lenders require a P&L statement signed by a CPA or a licensed tax preparer. Software-generated reports from platforms like QuickBooks are acceptable for internal review, but final approval usually hinges on a third party verifying the data. A 12 month P&L must match the deposits shown on your bank statements within a 5% margin of error to be considered valid for qualification.

What happens if my business income has declined in the last six months?

A 10% or greater decline in business income over the last 6 months can lead to a loan denial or a reduced loan amount. Underwriters compare your recent bank statements to your previous year’s average to identify negative trends. If income has dropped by 20%, you must provide a written explanation and evidence that the business has stabilized to proceed with the underwriting process.

Is it possible to get a self-employed loan for an investment property?

You can obtain a self-employed loan for an investment property using a DSCR program. This loan type focuses on the property’s rental income rather than your personal tax returns. If the rental income covers the mortgage payment with a 1.20x coverage ratio, you qualify regardless of your personal employment status. This is a primary tool for scaling real estate portfolios quickly without tax documentation.