In the 2026 real estate market, waiting 60 days for a traditional bank to verify tax returns is a recipe for lost deals. For the non-W2 investor, the primary barrier to growth isn’t finding the property-it’s securing capital that moves as fast as the market. High down payment requirements and rigid income verification often stall expansion, leaving profitable opportunities on the table for competitors. Accessing specialized fix and flip funding is the critical lever required to bypass these hurdles and maintain the liquidity necessary for rapid scaling.

This guide details the mechanics of high-leverage financing built specifically for professional investors. You will learn how to secure up to 90% of the purchase price and 100% of the rehab costs, allowing you to transition from single projects to multi-unit portfolios. By prioritizing After Repair Value (ARV) and closing in under 10 days, you can outmaneuver the competition and maximize your ROI without the constraints of traditional lending boxes. It is time to treat your financing as a strategic asset rather than a bureaucratic obstacle.

Key Takeaways

- Scale your real estate portfolio by shifting focus from personal income to the property’s After Repair Value (ARV) and asset potential.

- Master the technical mechanics of LTC and LTV to secure higher leverage and optimize cash flow for distressed assets.

- Understand why professional investors view fix and flip funding as a strategic “smart money” tool for speed and efficiency over traditional bank financing.

- Navigate specialized loan programs designed for foreign nationals and business owners using non-traditional documentation like P&L statements.

- Learn the step-by-step process for structuring a deal that aligns your rehab budget with specific high-leverage financing goals.

What is Fix and Flip Funding and How Does It Work in 2026?

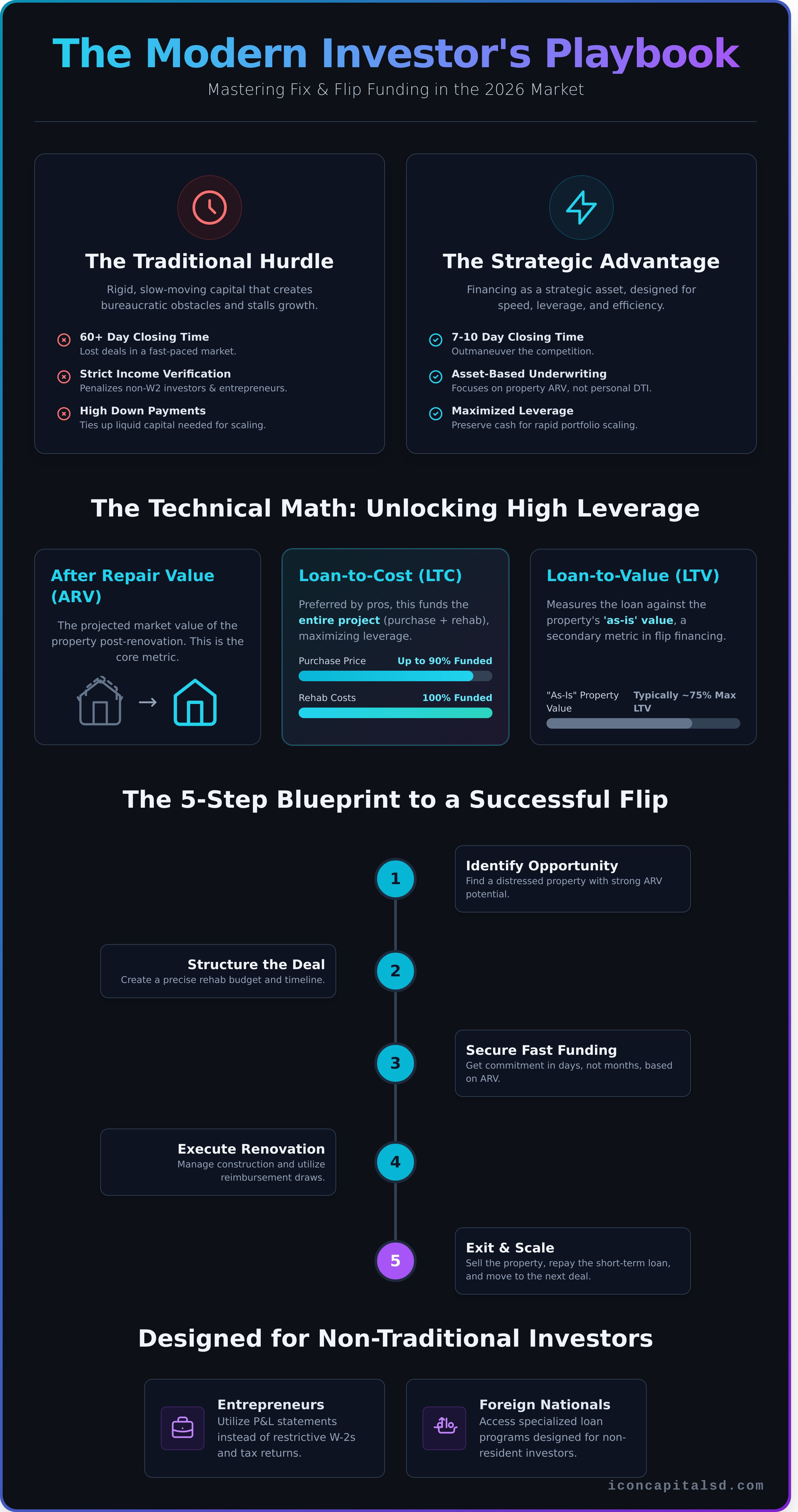

Fix and flip funding is a specialized form of short-term, asset-based financing designed specifically for the purchase and renovation of distressed real estate. In the 2026 market, professional investors have largely moved away from traditional banks in favor of creative capital providers. The primary driver of this shift is the “speed premium.” In a highly competitive environment, the ability to secure a commitment and close a deal in 7 to 10 days is a critical competitive advantage that traditional depository institutions cannot match.

The core mechanism of these loans relies on the property itself as collateral. Unlike conventional mortgages that focus on the borrower’s historical earnings, fix and flip underwriters prioritize the After Repair Value (ARV). By focusing on the projected value of the asset post-renovation, lenders can provide the leverage necessary to transform neglected properties into market-ready homes.

Asset-Based vs. Income-Based Lending

Asset-based underwriting represents a fundamental shift in how risk is assessed. By ignoring strict debt-to-income (DTI) ratios, this model allows for greater flexibility. The property’s condition and the feasibility of the renovation budget are the primary metrics for loan eligibility. This makes it the go-to solution for entrepreneurs and self-employed flippers who may have complex tax returns but possess high-value real estate opportunities. Understanding What is Fix and Flip investing involves recognizing that the asset’s potential, rather than personal income, drives the qualification process.

The Short-Term Nature of Flip Capital

Capital for fix and flip funding is structured to align with the project lifecycle, typically featuring loan durations of 6 to 18 months. This timeframe provides ample room for acquisition, construction, and disposition. To ensure the investor maintains maximum monthly cash flow during the heavy lift of renovation, these loans often utilize interest-only payment structures.

- Duration: 6 to 18 months to match project milestones.

- Payments: Interest-only to preserve working capital.

- Leverage: Focused on ARV to minimize out-of-pocket costs.

A bridge loan serves as the functional link between the initial acquisition of a property and the eventual permanent financing or sale. This ensures that the investor has the liquidity needed to scale their portfolio without being tied to long-term debt obligations during the construction phase.

The Technical Math: LTC, LTV, and ARV Explained

Securing fix and flip funding requires a shift from the consumer-centric metrics of Traditional Mortgages to asset-based evaluations. Lenders prioritize the deal’s profitability, using three core metrics: Loan-to-Cost (LTC), Loan-to-Value (LTV), and After Repair Value (ARV). While LTV measures the loan against the current “as-is” value, LTC focuses on the total project budget, providing a clearer picture of the investment’s leverage.

The “70% Rule” has long been the industry benchmark-stating an investor should pay no more than 70% of the ARV minus renovation costs. However, in today’s high-appreciation markets, many experienced flippers successfully leverage up to 75% or 80% if the margins remain robust. Your “skin in the game” typically depends on your track record: first-time flippers may need a 20-25% down payment, while seasoned pros can often secure funding with as little as 10% down.

Decoding Loan-to-Cost (LTC)

LTC is the preferred metric for professional investors because it accounts for the entire project scope. A common structure includes funding 90% of the purchase price and 100% of the renovation costs. It is important to understand that rehab funds are typically released via a reimbursement model. You complete a specific phase of work, an inspection is performed, and the lender releases a “draw” to cover those costs. Precise budget management is mandatory to ensure you maintain enough liquidity to bridge the gap between draws.

Mastering After Repair Value (ARV)

ARV is the projected market value of the property once all renovations are finalized. Lenders determine this using an “As-Completed” appraisal, which relies heavily on comparable sales (comps) of renovated homes in the immediate vicinity. Accurate renovation estimates are the foundation of your application; if your budget is unrealistic, your ARV-and your funding-will be compromised. Icon Capital leverages deep market expertise to provide creative financing solutions based on realistic ARV projections, ensuring your fix and flip funding aligns with the actual profit potential of the deal.

Fix and Flip vs. Hard Money vs. Traditional Mortgages

Professional investors distinguish between “hard money” and “smart money.” While the terms are often used interchangeably, fix and flip funding is a strategic tool used to maximize leverage and speed. A common misconception is that these loans are a last resort for those with poor credit. In reality, high-net-worth investors utilize this capital to maintain liquidity while scaling multiple projects simultaneously. It is an efficiency play, not a credit play.

When comparing lending tiers, the trade-offs involve speed, documentation, and cost:

- Traditional Mortgages: Lowest interest rates, but requires 30-45 days to close and strict “as-is” property conditions.

- Fix and Flip/Hard Money: Higher interest rates (typically 9-12%), but closes in 5-10 days with funding based on the asset’s potential.

The “Opportunity Cost” calculation is what drives professional decision-making. Paying 10% interest on a short-term bridge loan is a minor line item when compared to losing a deal with a $50,000 profit margin because a traditional bank couldn’t meet a closing deadline. Understanding technical metrics like LTC, LTV, and ARV Explained is essential; by leveraging high LTC (Loan-to-Cost), you preserve your own cash for the next acquisition.

The Downside of Traditional Bank Loans

Traditional banks are structurally ill-equipped for the pace of the flip market. Their 30-day closing windows and rigid appraisal processes often kill deals in competitive environments. Furthermore, banks typically enforce a “seasoning” requirement, preventing investors from cashing out or selling for 6-12 months. Icon Capital’s fix and flip funding eliminates this documentation fatigue by focusing on the deal’s merit rather than the borrower’s personal tax returns.

Transitioning to Long-Term Holds (The BRRRR Method)

For investors utilizing the Buy, Rehab, Rent, Refinance, Repeat (BRRRR) strategy, bridge financing is the essential first step. The goal is to exit the high-interest flip loan into a 30-year DSCR loan once the property is stabilized. Working with a lender that offers both bridge and permanent financing ensures a seamless transition, reduces redundant closing costs, and allows you to scale your portfolio with a single, reliable capital partner.

Specialized Funding for Non-Traditional and Foreign Investors

Traditional lenders often reject high-potential investors who lack standard W-2 documentation or US citizenship. Icon Capital LLC specializes in these complex scenarios, providing fix and flip funding tailored to unique financial profiles. We prioritize asset value and liquidity, ensuring that non-traditional borrowers can secure capital without the hurdles of conventional underwriting.

Foreign National Flip Programs

Non-US citizens frequently struggle with domestic credit requirements and the lack of a Social Security Number. We bridge this gap through specialized Foreign National Loans designed for real estate investment. Our programs focus on the strength of the deal rather than domestic credit history.

- Entity Structure: Borrowers typically close under a US-based LLC.

- Identification: Qualification is available via ITIN or valid foreign passport.

- Credit Navigation: We utilize international credit reports or focus on asset-based qualifying metrics to bypass traditional US credit scores.

Self-Employed and P&L Funding Solutions

Business owners often utilize legal deductions that reduce “reported” income on tax returns, leading to automatic denials from big banks. Icon Capital LLC provides creative fix and flip funding solutions that look at the actual health of your business.

- P&L Loans: Use a CPA-prepared Profit & Loss statement to verify income, replacing the need for two years of tax returns.

- Bank Statement Programs: We analyze 12 to 24 months of deposits to determine true cash flow and debt-to-income ratios.

- 1099 Loans: A streamlined tool for independent contractors to qualify based on gross earnings.

For investors with high liquidity but low reported income, we utilize asset-based qualification. By leveraging your existing portfolio and cash reserves, we can structure high-LTV loans that focus on the property’s exit strategy. This pragmatic approach allows seasoned investors and business owners to scale their portfolios efficiently. To explore your specific deal structure, contact Icon Capital LLC today.

How to Secure Fix and Flip Funding with Icon Capital

Securing fix and flip funding shouldn’t be a bottleneck for your investment strategy. At Icon Capital, we utilize a streamlined four-step process designed to move your project from application to “cash in hand” with maximum efficiency and professional precision.

- Step 1: The Initial Deal Review – Submit your property address and a detailed rehab budget for an immediate preliminary assessment.

- Step 2: Structuring the Loan – We align Loan-to-Value (LTV) and Loan-to-Cost (LTC) ratios to match your specific cash flow requirements and project scope.

- Step 3: Underwriting and Appraisal – Our fast-track process prioritizes After Repair Value (ARV) verification to ensure the asset supports your investment goals.

- Step 4: Closing and Funding – By bypassing traditional banking delays, we provide the capital you need in as little as 7 days.

Preparing Your ‘Flip File’ for Instant Approval

Speed is the primary currency in real estate. To expedite your fix and flip funding request, ensure your “Flip File” is complete with these three essential documents: the Purchase Contract, Entity Docs (LLC or Corporation), and a comprehensive Scope of Work. The Scope of Work serves as the detailed roadmap for your rehab draws, outlining every renovation phase from demolition to finish. Additionally, highlighting your experience level with a list of previous successful exits can help you secure lower origination fees and higher leverage.

The Icon Capital Advantage

We provide more than just capital; we offer a partnership built on transactional transparency and expertise. Our clients benefit from direct access to underwriters who understand creative financing, allowing us to approve complex deals that traditional lenders often overlook. We maintain a strict policy of no “junk fees,” focusing instead on the long-term scalability of your portfolio.

Ready to scale? Request a custom mortgage quote for your next project today. For investors looking to build a sustainable pipeline, Icon Capital is the specialist enabler you need to move from acquisition to profitable exit. Explore our full range of creative financing solutions at iconcapitalsd.com.

Leveraging Fix and Flip Funding for Scalable Growth

Navigating the real estate market in 2026 requires more than just finding the right property; it demands a sophisticated approach to leverage and technical analysis. Understanding the interplay between LTC, LTV, and ARV is essential for any investor looking to maximize returns while minimizing out-of-pocket capital. By utilizing creative financing over traditional mortgages, you gain the agility needed to secure distressed assets and execute renovations without the constraints of rigid banking standards.

Securing reliable fix and flip funding is the final step in transitioning from a single project to a scalable investment business. Icon Capital specializes in these high-performance structures, offering up to 90% LTC and 100% Rehab Funding. Our streamlined process allows investors to close in as little as 7 days, with specialized programs specifically designed for foreign nationals and self-employed professionals. We focus on the mechanics of the deal, providing the liquidity and speed necessary to outperform the competition.

Scale your portfolio with Icon Capital’s creative flip funding-Get a Quote Now

Take the next step in optimizing your investment strategy and securing the capital your portfolio deserves.

Frequently Asked Questions

How do fix and flip loans work for beginners with no experience?

Beginners can secure fix and flip funding by leveraging the property’s After Repair Value (ARV). While experienced flippers often receive more favorable terms, Icon Capital provides bridge loans to new investors based on asset potential and a detailed renovation budget. You typically need a larger down payment, often 20-25%, and a clear exit strategy, such as a property sale or a DSCR refinance, to qualify for the loan.

What is the minimum credit score required for fix and flip funding?

Most private lenders require a minimum credit score of 620 to 660. While these are asset-based loans, the borrower’s credit score influences the interest rate and maximum LTV. High-leverage options usually require a score of 700 or above. For those with lower scores, providing additional liquidity or a more significant equity stake in the property can help secure approval from the underwriter.

Can I get 100% financing for a fix and flip project?

True 100% financing is rare and reserved for experienced investors with a proven track record. Most fix and flip funding structures cover up to 90% of the purchase price and 100% of the renovation costs, provided the total loan does not exceed 75% of the ARV. Borrowers should expect to bring at least 10% of the acquisition price as “skin in the game” to close the deal.

What is the typical interest rate for a fix and flip loan in 2026?

In 2026, interest rates for fix and flip loans generally range between 9% and 13%, depending on the borrower’s experience and the project’s risk profile. These are short-term, interest-only bridge loans designed for rapid execution. Rates are higher than traditional mortgages because they prioritize speed and flexible underwriting. Market conditions and Federal Reserve policies will dictate the exact floor for these non-QM products.

How long does it take to get funded for a property flip?

Speed is the primary advantage of private lending. Icon Capital typically funds a property flip within 7 to 10 business days. Traditional banks may take 45 days or more, but our streamlined process focuses on the property’s valuation and the contractor’s scope of work. Once the appraisal and title work are cleared, we move quickly to the closing table to ensure investors meet their contract deadlines.

Is an appraisal required for an asset-based flip loan?

Yes, a specialized “as-is” and “as-completed” appraisal is required for most asset-based loans. This valuation confirms the current market price and the projected After Repair Value (ARV) based on your renovation budget. The appraiser reviews the scope of work to ensure the proposed improvements justify the loan amount. This data is critical for underwriters to calculate the Loan-to-Value (LTV) and mitigate investment risk.

What happens if my renovation goes over budget or past the loan term?

If a renovation exceeds the budget, the investor must cover the shortfall with personal capital, as loan draws are capped at the original approved amount. If the project exceeds the typical 12-month term, you may request a loan extension. Extensions usually involve an additional fee and interest rate adjustment. It is vital to communicate with your lender early to avoid default or potential foreclosure proceedings.

Can foreign nationals get funding for flips in the United States?

Yes, foreign nationals can access funding for U.S. real estate investments. These programs typically require a larger down payment-often 30% to 40%-and proof of liquidity in a U.S.-based bank account. While a domestic credit score isn’t always required, lenders will evaluate the asset’s viability and the borrower’s global financial standing. Icon Capital specializes in these creative financing solutions for international investors seeking to scale their portfolios.