In the fast-paced world of real estate investing, securing the right financing quickly is non-negotiable. A delay in funding can mean the difference between closing a profitable deal and losing it to a competitor who can move faster. Traditional lenders often fail to meet the speed and flexibility required for a successful flip, leaving investors without the necessary capital for both acquisition and renovation. This forces you to navigate a complex landscape of financial jargon and unconventional funding sources alone.

This guide provides a direct analysis of the primary types of loans for flipping houses. We will dissect the most effective financing instruments-from hard money and private loans to HELOCs and conventional options-to provide a clear framework for your investment strategy. You will gain a functional understanding of critical terms, evaluate the pros and cons of each funding vehicle, and learn how to secure capital that covers your entire project scope. The objective is to equip you to partner with a lender who operates at the speed of your business and funds deals efficiently.

Key Takeaways

- Leverage the equity in your current properties through HELOCs or cash-out refinances to secure capital for your first investment flip.

- Compare specialized types of loans for flipping houses, including hard money and fix-and-flip products, to access capital faster than traditional banks allow.

- Select the optimal loan by matching key deal metrics-like timeline and ARV-with the specific terms and structure of each financing option.

- Your choice of lender is as crucial as the loan product; partner with a specialist who understands the pace required for fix-and-flip deals.

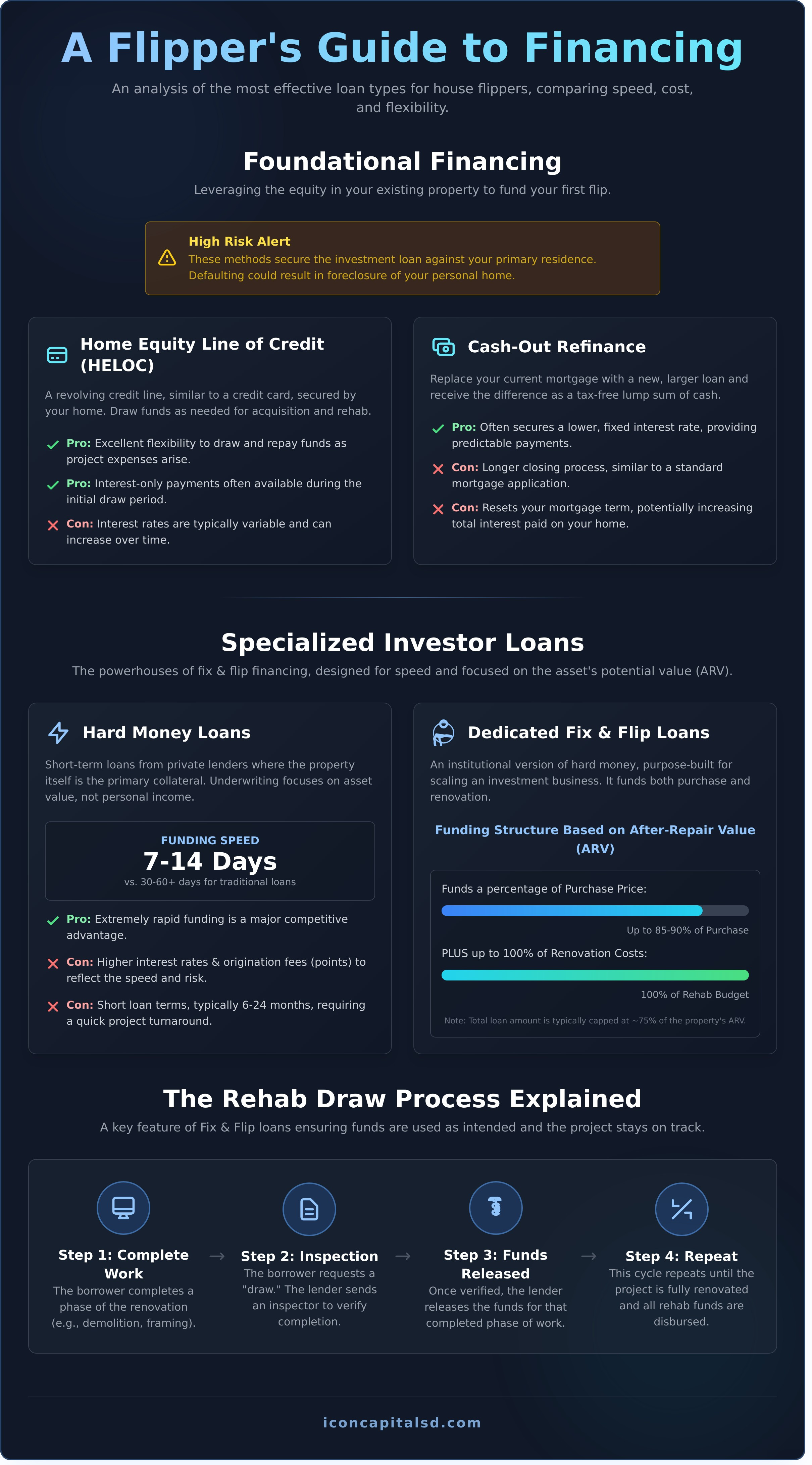

Foundational Financing: Using Your Existing Property Equity

For new real estate investors, the most direct path to securing capital often involves leveraging an existing asset: their primary residence. When exploring the various types of loans for flipping houses, these foundational financing options use the equity you’ve built in your own home to fund your first project. This strategy is popular because it can provide access to lower interest rates than many investment-specific loans. However, it’s critical to understand the mechanics of what is house flipping and weigh the significant risk of securing an investment loan with your personal home.

Two primary instruments allow investors to tap into their home equity. Each offers a distinct structure, with unique advantages and disadvantages for a fix-and-flip project.

Home Equity Line of Credit (HELOC)

A HELOC functions like a revolving line of credit-similar to a credit card-secured by your home’s equity. This structure allows you to draw funds as needed for property acquisition and subsequent renovation costs, providing significant financial control throughout the project’s lifecycle.

- Pro: Excellent flexibility to draw and repay funds as project expenses arise.

- Pro: Interest-only payments are common during the initial draw period, improving cash flow.

- Con: Interest rates are typically variable and can increase over the loan term.

- Con: Defaulting on the loan places your primary residence at risk of foreclosure.

Cash-Out Refinance

A cash-out refinance involves replacing your existing mortgage with a new, larger loan. You receive the difference between the two loan amounts as a tax-free, lump-sum cash payment. This capital can then be deployed directly for your fix-and-flip investment.

- Pro: Often secures a lower, fixed interest rate compared to a HELOC, providing predictable payments.

- Con: The closing process is longer and more involved, similar to a standard mortgage application.

- Con: It completely resets your mortgage term, potentially increasing the total interest paid over time on your primary residence.

Specialized Investor Loans: The Fix & Flip Powerhouses

To succeed in the fast-paced house flipping market, investors must move beyond traditional banking. Specialized investor loans are structured for speed, flexibility, and the unique financial realities of a flip. Unlike conventional mortgages that scrutinize personal income and debt-to-income ratios, these products focus on the asset’s potential. Lenders underwrite the deal based on the property’s After-Repair Value (ARV), funding both the acquisition and the necessary renovation costs. When evaluating the different types of loans for flipping houses, these asset-based options are the primary tools for serious investors.

Hard Money Loans

Hard money loans are short-term financing solutions provided by private investors or companies rather than traditional banks. The primary underwriting criterion is the value of the real estate asset securing the loan. This asset-focused approach allows for significantly faster closing times, which is a critical advantage in competitive markets.

- Pros: Extremely rapid funding, often closing in just 7-14 days. Flexible underwriting criteria compared to conventional loans.

- Cons: Higher interest rates and origination fees (points) reflect the increased risk and speed. Loan terms are typically short, usually 6-24 months.

Dedicated Fix & Flip Loans

Functioning as a more institutional version of hard money, dedicated fix and flip loans are designed specifically for scaling an investment business. These financial products typically finance a percentage of the purchase price and up to 100% of the planned renovation budget. The loan amount is calculated based on the property’s ARV. These structured Fix-and-flip loans provide the leverage needed to manage multiple projects simultaneously, making them a cornerstone for professional flippers.

Understanding the Rehab Draw Process

A key feature of fix and flip financing is the rehab draw process. Renovation funds are not disbursed as a single lump sum at closing. Instead, the capital is released in stages, or “draws,” as specific phases of the project are completed. A lender-approved inspector verifies the progress against the agreed-upon scope of work before releasing the next draw. This methodical process mitigates risk for the lender and ensures the borrower uses the funds as intended, keeping the project on track and on budget.

Alternative & Situational Funding Options

While hard money and conventional financing cover many scenarios, seasoned investors understand the need for a diverse toolkit. Certain projects or market conditions demand more creative solutions. Evaluating these alternative types of loans for flipping houses provides a strategic advantage, enabling you to seize opportunities that others cannot. These options often involve different trade-offs in cost, risk, and complexity, but offer unparalleled flexibility in the right situation.

Bridge Loans

A bridge loan is a short-term financing instrument designed to ‘bridge’ the gap between two real estate transactions. Its most common use case is for an active investor who needs to secure a new flip property before the sale of a current project is finalized. Secured by the borrower’s existing property equity, a bridge loan provides rapid access to capital, making it an essential tool for scaling a real estate portfolio and managing multiple projects simultaneously.

Unsecured Personal Loans

Unlike most real estate financing, an unsecured personal loan is not secured by a physical asset. Instead, qualification is based entirely on your personal creditworthiness and financial history. While not typically used to purchase a property outright due to lower loan limits, they are an excellent source of quick capital for smaller project needs like renovation materials, staging costs, or covering unexpected expenses.

- Pros: Extremely fast funding process and no lien is placed on the investment property.

- Cons: Loan amounts are generally smaller, and interest rates are significantly higher than secured loans.

Seller Financing & Private Money

For investors with a strong professional network, seller financing and private money are two of the most flexible types of loans for flipping houses available. With seller financing, the property owner essentially acts as the lender, and you negotiate terms directly. Private money involves sourcing a loan from an individual investor in your network. Both routes bypass traditional underwriting, offering highly negotiable terms on everything from interest rates to repayment schedules. As platforms like Forbes often highlight, building relationships with hard money and private money lenders is critical, as these deals are built on mutual trust and a proven track record.

Decision Matrix: How to Choose the Right Loan for Your Flip

There is no single ‘best’ loan for a house flip. The optimal financing solution is determined by the specific parameters of your deal and your individual financial position. This decision matrix provides a clear framework for evaluating the different types of loans for flipping houses against the factors that matter most: speed, project scope, and your investor profile. Use this structure to confidently select the right capital for your next investment.

Factor 1: Speed to Close

In competitive real estate markets, speed is a critical advantage. When securing a property at auction or against multiple cash offers, you need capital fast. Hard money and dedicated fix & flip loans are designed for rapid closing, often funding in as little as 7-14 days. In contrast, traditional options like HELOCs or cash-out refinances involve a lengthy underwriting process and can take 30-60 days to close, putting your deal at risk.

Factor 2: Project Scope & Rehab Budget

The scale of your renovation dictates your financing needs. For substantial projects involving structural changes or complete remodels, you require a loan that funds both the acquisition and the rehab budget. Fix & flip loans are structured specifically for this, releasing construction funds in draws as work is completed. A personal loan, conversely, may only be sufficient for minor cosmetic updates and lacks the necessary capital for a full-scale flip.

Factor 3: Your Experience & Financial Profile

Your track record and financial standing are key determinants. New investors often leverage personal assets, using home equity to fund their first project. Seasoned investors, however, typically utilize hard money or fix & flip loans to scale their portfolio without tying up personal capital, allowing them to pursue multiple deals simultaneously. Unsure which option fits your deal? Request a free quote to discuss your project.

By analyzing your project through these three lenses, you can effectively narrow your choices. The following table provides a side-by-side comparison of the key metrics for each loan type, further simplifying your selection process. For a detailed analysis of your specific scenario, contact the experts at Icon Capital LLC.

Why Your Lender Matters: Partnering with a Specialist

Understanding the different types of loans for flipping houses is a critical first step, but your success often hinges on the financial partner you choose. In the time-sensitive world of real estate investment, the lender is more than a source of capital-they are a strategic partner. A slow, inexperienced lender can cause you to lose a profitable deal, while a specialist can provide the leverage and speed needed to scale your portfolio.

The right partner provides expertise alongside funding. They understand the nuances of a fix-and-flip project, from acquisition costs to renovation budgets and the final sale. This expertise translates into a smoother, more efficient process that aligns with your investment goals.

Traditional Banks vs. Private Lenders

The underwriting process for a traditional bank versus a private lender is fundamentally different. Banks are risk-averse and prioritize a borrower’s personal financial history. Their decision is based heavily on:

- Personal income and W-2s

- Debt-to-income (DTI) ratios

- Extensive credit history reviews

In contrast, private and hard money lenders like Icon Capital focus on the viability of the asset itself. We underwrite the deal based on its potential, primarily looking at the property’s After Repair Value (ARV). This asset-based approach allows for faster approvals and funding, which is essential when competing for in-demand properties.

The Icon Capital Advantage for Flippers

Choosing a specialist means partnering with a team that is built for real estate investors. At Icon Capital, we provide creative financing solutions designed specifically for the pace and structure of a flip. Our process is engineered for efficiency, removing the bureaucratic delays common with conventional lending.

We evaluate your project on its merits and potential profitability. Our advantage is clear:

- Asset-Based Underwriting: We focus on the ARV of your project, not just your personal income statements.

- Speed to Close: Our streamlined process is designed to fund deals quickly, giving you a competitive edge in the market.

- Investor Expertise: We are not generalists. We are specialists who understand the metrics that define a successful flip.

When your success depends on speed and reliable capital, working with a specialist is the only logical choice. Ready to partner with a lender who understands your business? Get a personalized quote today.

Finalizing Your Funding Strategy: The Path to Profitability

Choosing the right financing is as critical as choosing the right property. Your decision must be guided by the project’s timeline, renovation scope, and your personal financial position. Navigating the various types of loans for flipping houses, from hard money to specialized fix-and-flip products, requires a clear strategy and an expert partner who understands the market’s velocity.

The right lender simplifies this complex landscape. At Icon Capital, we are specialists in Non-QM and investor loans, providing the creative financing solutions and fast, asset-based underwriting that serious investors demand. We structure deals designed for profitability and speed, ensuring you can capitalize on opportunities as they arise.

Ready to execute your next project with confidence? Get pre-approved for your next flip with Icon Capital. Partner with a specialist and turn your investment opportunity into a profitable reality.

Frequently Asked Questions

Can I get a loan for flipping a house with no money down?

While 100% financing is uncommon, some lenders offer high-leverage options. Typically, a fix and flip loan will cover up to 90% of the purchase price and 100% of the renovation budget. This structure requires the borrower to fund the down payment, closing costs, and maintain liquid reserves. A true no-money-down scenario is not standard practice, as lenders require borrowers to have a direct financial stake in the project’s success.

What are the typical interest rates and fees for a fix and flip loan?

Interest rates for fix and flip loans generally range from 9% to 14%, depending on the lender, borrower experience, and perceived project risk. In addition to interest, borrowers should expect to pay origination fees of 1 to 3 points (where 1 point equals 1% of the loan amount). These costs are directly influenced by factors such as your credit profile, investment history, and the loan-to-value (LTV) ratio of the deal.

How do lenders calculate the After-Repair Value (ARV) of a property?

Lenders determine the After-Repair Value (ARV) through a formal appraisal conducted by a licensed third-party appraiser. The appraiser analyzes recent sales of comparable properties (comps) in the immediate area that are similar in size, style, and condition to your property’s planned final state. Adjustments are made for any differences, and the appraiser provides a detailed report projecting the property’s market value once all proposed renovations are complete.

What is the minimum credit score needed for a house flipping loan?

While these types of loans for flipping houses are primarily asset-based, most lenders still have a minimum credit score requirement. The typical minimum FICO score is between 620 and 660, though some may go lower for experienced investors with a strong deal. A higher credit score demonstrates financial responsibility and can help you secure more favorable terms, including lower interest rates and origination fees. The strength of the asset remains the most critical factor.

Can I use a fix and flip loan to renovate a property I plan to live in?

No, fix and flip loans are strictly for business purposes and can only be used on non-owner-occupied investment properties. These are commercial financial instruments, not consumer mortgages. If you intend to purchase and renovate a property to use as your primary residence, you must seek consumer-focused financing such as an FHA 203(k) loan or a conventional renovation mortgage. Lenders must verify the property is for investment to comply with regulations.

How long are the terms for most hard money or fix and flip loans?

The terms for hard money and fix and flip loans are short-term by design, aligning with a project’s rapid lifecycle. Most loans have terms ranging from 6 to 18 months, with 12 months being the most common. This provides sufficient time to acquire the property, complete renovations, and execute a sale. The loan is intended as a bridge solution to be paid off upon the sale of the asset, not as long-term financing.