In the high-stakes world of property flipping, the difference between a significant profit and a costly mistake often comes down to one critical element. Understanding how to finance a property flip correctly is the foundation of a successful project. Choosing the wrong loan can mean losing a deal to slow funding or watching high interest rates and points erode your returns before you even list the property. The complexity of options and industry jargon can be a barrier, but it doesn’t have to be.

This guide is designed to eliminate that uncertainty and provide a clear, step-by-step framework for mastering the financing process. We will break down the most effective loan options available to investors-from hard money to conventional products-and demystify key terms like LTV and ARV. By the end, you will have the strategic knowledge to calculate costs, project profitability, and confidently secure the right funding to maximize your next investment’s potential.

Key Takeaways

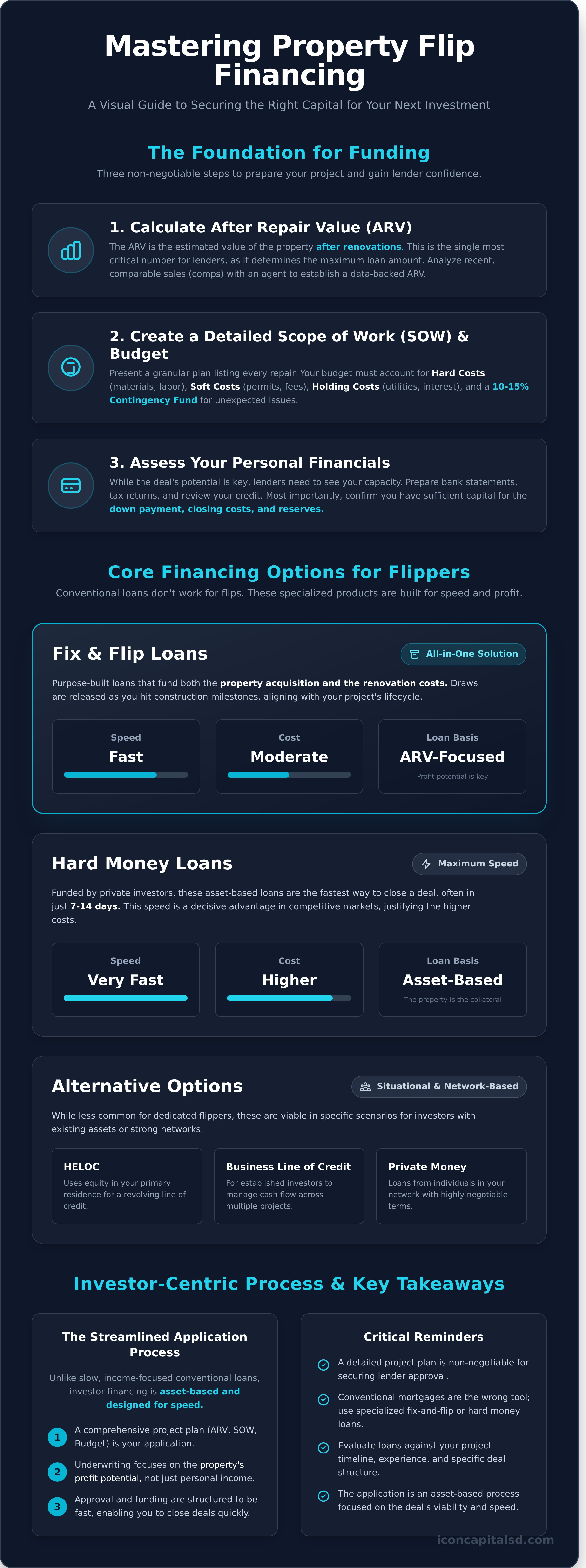

- A comprehensive project plan, including a detailed budget and scope of work, is a non-negotiable first step for securing lender approval.

- Conventional mortgages are not designed for investment flips; investors must leverage specialized financing like hard money or fix-and-flip loans for speed and flexibility.

- Mastering how to finance a property flip requires evaluating loan options against your specific project timeline, experience level, and deal structure.

- The application for an investment loan is a streamlined, asset-based process designed for speed and focused on the property’s profit potential, not just personal income.

First Steps: Preparing Your Flip for Financing

Before exploring how to finance a property flip, you must first construct a bulletproof business plan. Lenders prioritize strong deals over strong borrowers alone; your preparation is what demonstrates the project’s viability and your expertise as an investor. The practice of real estate flipping-purchasing, renovating, and selling an asset for profit-is fundamentally a data-driven transaction. For a foundational overview, you can explore this resource on what is property flipping? A detailed and realistic plan minimizes perceived risk for the lender and is the most critical step toward securing capital and streamlining the entire funding process.

Calculate the ‘After Repair Value’ (ARV)

The After Repair Value (ARV) is an estimate of what the property will be worth after all renovations are complete. This is arguably the most critical number for any private or hard money lender, as loan amounts are calculated as a percentage of the ARV. To determine an accurate ARV, analyze recent comparable sales (comps) of similar, updated properties in the immediate vicinity. Partnering with an experienced real estate agent or appraiser is essential for a credible and data-backed valuation.

A reliable local agent is your best resource for pulling accurate comps and understanding neighborhood trends. If you’re investing in Southern California, for example, you can check out County Properties for this kind of specialized support.

Create a Detailed Scope of Work (SOW) and Budget

A comprehensive Scope of Work (SOW) and budget shows lenders you have performed thorough due diligence. The SOW should list every planned repair, from foundation work to final fixtures. Your budget must be equally granular and account for all project costs, including:

- Hard Costs: All materials and labor for the physical renovation.

- Soft Costs: Expenses like permits, insurance, architectural fees, and property taxes.

- Holding Costs: Utilities, loan interest, and other expenses incurred during the project timeline.

- Contingency Fund: A reserve of 10-15% of the total budget to cover unforeseen issues.

Assess Your Personal Financials

While the deal’s strength is paramount, lenders must also verify your capacity to execute the project. Before applying for a loan, gather all necessary documentation, including recent bank statements, tax returns, and any business entity information. Review your credit score and history, as this impacts qualification and terms. Most importantly, determine the capital you have available for the down payment, closing costs, and reserves. Lenders require you to have “skin in the game” to ensure you are as committed to the project’s success as they are.

Core Financing Options for House Flippers

Conventional mortgages are not engineered for the velocity required in real estate investing. Their lengthy underwriting processes and owner-occupancy clauses make them impractical for short-term projects. Investors determining how to finance a property flip effectively must look to specialized products designed for speed, flexibility, and leveraging an asset’s potential value. Companies like Icon Capital LLC offer such solutions. The following are the core financing tools used by professional flippers to acquire and renovate properties.

Fix and Flip Loans

These are purpose-built financial instruments that fund both the acquisition and the renovation of an investment property. Lenders typically structure these with an initial draw for the purchase and subsequent draws to fund construction milestones. With short terms, usually 12-24 months, and interest-only payments, these specialized fix and flip loans are designed to align with a project’s lifecycle. Critically, approval is heavily weighted on the deal’s After-Repair Value (ARV), not solely on the borrower’s personal income.

Hard Money Loans

Funded by private investors rather than traditional banks, hard money loans are the industry’s solution for rapid execution. These asset-based loans can often be funded in as little as 7-14 days, a decisive advantage in competitive real estate markets. This speed comes at the cost of higher interest rates and origination points compared to other options. However, for experienced investors who need to close quickly and confidently, the cost is often justified by the opportunity secured.

Alternative (But Less Common) Options

While less common for dedicated flipping, other financing vehicles can be effective in specific scenarios. These solutions are most relevant for investors who already possess a significant asset base or a strong personal network.

- Home Equity Line of Credit (HELOC): Utilizes the available equity in your primary residence or another investment property to provide a revolving line of credit for your project.

- Business Lines of Credit: A viable tool for seasoned real estate investors with an established business entity and a proven track record to manage cash flow across multiple concurrent projects.

- Private Money Lenders: Loans sourced from individuals in your network. Terms are highly negotiable and based on the relationship between the borrower and lender.

Comparing Your Options: Which Loan Is Right for Your Project?

The optimal financing for your property flip is determined by three core factors: your experience level, the project timeline, and the specific structure of the deal. There is no universal solution; the right loan is the one that aligns with your strategic goals. To effectively decide how to finance a property flip, you must compare your options across a clear framework of cost, speed, and qualification requirements.

Speed vs. Cost

In real estate investing, speed and cost often have an inverse relationship. Your choice depends on market conditions and deal urgency.

- Hard Money Loans: Offer maximum speed, often closing in 7-10 days. This velocity comes at a higher cost through origination points and interest rates, but it can be the key to securing a competitive deal.

- Fix and Flip Loans: Provide a balance, with faster closing times than conventional loans but more moderate, structured costs than traditional hard money.

- Conventional Options (HELOCs/Cash-Out Refi): These are the slowest, taking 30-60+ days to fund. In exchange, they offer the lowest interest rates. In a hot market, this delay can mean losing the property to a faster-moving investor.

Loan-to-Value (LTV) and Down Payment

Leverage is critical for scaling your flipping business. Understanding how lenders structure their offers is essential. Fix and Flip loans are typically based on Loan-to-Cost (LTC), often funding up to 90% of the purchase price and 100% of the renovation budget. In contrast, Hard Money loans are often structured around the property’s After-Repair Value (ARV), lending up to 75% of that future value. Higher leverage means less cash out-of-pocket per deal, allowing you to deploy capital across multiple projects simultaneously.

Qualification and Experience

Unlike conventional mortgages that heavily scrutinize personal income, asset-based lenders focus on the viability of the investment property itself. Both Hard Money and Fix & Flip lenders prioritize the deal’s potential profit. While a strong track record is always beneficial, many programs are designed to be accessible for newer investors with a solid project plan. The process of getting approved for a flip loan centers on the asset’s numbers-the purchase price, rehab budget, and ARV. The most effective way to determine how to finance a property flip for your specific situation is to see a direct comparison. Get a personalized quote to compare your exact loan options.

The Application Process: How to Get Approved for a Flip Loan

Securing a loan for a property flip is a different experience than applying for a conventional mortgage. The process is streamlined, focusing on the asset’s potential and the investor’s plan rather than long-term personal income verification. For investors who need to know how to finance a property flip quickly, being prepared is the most critical factor for a fast and successful closing. Follow these steps to navigate the application process efficiently.

Step 1: Lender Selection and Initial Quote

Begin by researching private lenders that specialize in investment properties. A partner like Icon Capital LLC understands the urgency and unique structure of flip deals. Submit an initial inquiry with basic deal information, including the purchase price, estimated rehab budget, and projected After-Repair Value (ARV). You will typically receive a preliminary term sheet outlining proposed rates, terms, and fees. This is a non-binding offer that allows you to assess the loan structure before committing.

Step 2: Submitting Your Full Loan Package

Once you accept the preliminary terms, the lender will provide a checklist of required documents. A complete and organized loan package is essential to prevent delays in underwriting. Key items include:

- Your detailed Scope of Work (SOW) and renovation budget

- The fully executed purchase and sale agreement

- Entity documents (e.g., LLC Operating Agreement, Articles of Organization)

- Personal financial statements and proof of funds for the down payment, closing costs, and reserves

Step 3: Underwriting and Appraisal

The lender’s underwriting team will conduct a thorough review of your file to assess risk and verify the deal’s viability. A crucial part of this stage is the property appraisal, which is ordered to validate the ARV. Unlike a standard appraisal, this focuses heavily on the property’s value after your planned renovations are complete. Be prepared to answer questions and provide any additional information promptly. This phase typically takes 5-10 business days.

Step 4: Closing and Funding

After your loan receives final approval from underwriting, you will be issued closing documents for review and signature. The closing is managed by a neutral third party, such as a title company or real estate attorney, who ensures all conditions are met. Once the documents are signed, the lender wires the funds to close the purchase, and you can begin your renovation project. This final step in how to finance a property flip is what moves your investment from plan to reality.

Ready to start? Request a quote to begin the process.

Finalizing Your Flip Financing Strategy

Mastering how to finance a property flip hinges on meticulous preparation and selecting the ideal loan product for your project. By understanding the core financing options available and preparing a thorough application, you can strategically position your deal for approval and maximize your potential return on investment.

When speed and leverage are critical, the right financial partner is essential. Icon Capital provides creative financing solutions designed for real estate investors. We enable clients to secure competitive deals with fast closings and can finance up to 90% of the purchase and 100% of rehab costs. With proven solutions for both new and experienced investors, we are equipped to fund your next deal. Explore Icon Capital’s Fix & Flip loan programs today.

With the right capital partner, your next profitable project is within reach.

Frequently Asked Questions

Can I finance a property flip with no money down?

Securing 100% financing for a property flip is uncommon. Most hard money and private lenders require the borrower to contribute capital, typically 10-20% of the total project cost (purchase price plus renovation budget). Lenders view this “skin in the game” as a critical risk mitigator. While some programs may finance 100% of the renovation costs, the borrower is almost always expected to provide a down payment for the property acquisition itself.

What is the typical interest rate for a fix and flip loan?

Interest rates for fix and flip loans are higher than conventional mortgages, generally ranging from 9% to 12% or more. The final rate is determined by several factors, including the borrower’s experience level, credit profile, the property’s location, and the lender’s risk assessment. These are short-term, interest-only loans structured to maximize investor leverage and are priced according to the increased risk and speed of funding compared to traditional bank loans.

What credit score do I need to finance a house flip?

While requirements vary by lender, a minimum credit score of 620 to 660 is a common benchmark for fix and flip financing. However, unlike conventional lending, the primary focus is on the asset’s viability-specifically, its After Repair Value (ARV). A strong deal with a high potential ROI can often compensate for a lower credit score, though a higher score will typically secure more favorable terms and lower interest rates.

How quickly can I get funding for a flip project?

Speed is a primary advantage of private and hard money lending. A key part of understanding how to finance a property flip is recognizing the need to close quickly. While a traditional mortgage can take 30-60 days, funding for a flip can often be secured in as little as 7 to 14 business days. A prepared borrower with all necessary documentation-including the purchase contract, scope of work, and entity documents-can significantly expedite this timeline.

Do I need an LLC to get a fix and flip loan?

Yes, the vast majority of private and hard money lenders require borrowers to close in the name of a business entity, such as a Limited Liability Company (LLC) or a corporation. These are considered business-purpose loans, not consumer mortgages. Using an entity protects both the borrower from personal liability and the lender from consumer lending regulations. Individual or personal name closings are extremely rare in this financing sector.

What are ‘points’ on a hard money or fix and flip loan?

Points are an upfront loan origination fee paid to the lender at closing. One point is equal to one percent of the total loan amount. For example, a loan of $400,000 with a 2-point fee would require a $8,000 payment at closing. This fee compensates the lender for underwriting and processing the short-term loan. The number of points charged, typically between 1 and 3, depends on the loan’s risk and complexity.

Can I use a fix and flip loan to pay myself for labor?

Generally, you cannot use loan funds to pay yourself for “sweat equity.” The renovation portion of the loan is disbursed in draws to cover verified, third-party costs for materials and licensed labor. Lenders release funds after inspections confirm that work has been completed according to the approved budget. This process ensures the loan proceeds are directly used to increase the property’s value as collateral, rather than for personal compensation.