Your tax strategy shouldn’t be the reason you can’t buy a home. For many independent contractors, a $150,000 gross income often becomes a $45,000 net profit after deductions, which leads to immediate rejection from conventional banks. A 1099 income mortgage loan solves this by qualifying you based on your gross earnings rather than your taxable income. This approach prioritizes your actual cash flow over the figures reported to the IRS, allowing your business success to work for you rather than against you.

It’s frustrating when traditional lenders ignore your real-world buying power and focus solely on your tax returns. You’ve optimized your business for tax efficiency, and you shouldn’t be penalized for it. This guide explains how to secure a home or investment property using your 1099 earnings without changing your business expense strategy. You’ll learn the specific qualification process for 2026, including why a 10% to 20% down payment is standard and how to use 12 months of 1099 forms to prove your income. We will break down the mechanics of non-QM lending and show you how to bypass the debt-to-income hurdles that stop most self-employed applications.

Key Takeaways

- Understand how a 1099 income mortgage loan bypasses traditional tax return hurdles by qualifying you based on gross earnings instead of net profit.

- Learn the specific documentation requirements, including how underwriters apply standard expense factors to your 1099-NEC and 1099-MISC forms.

- Compare 1099 programs against bank statement loans to determine which Non-QM solution provides the most leverage for your unique income structure.

- Identify the core eligibility milestones, such as verifying two years of continuous self-employment in your current field.

- Discover Icon Capital’s approach to creative financing, featuring high loan amounts and flexible LTV options designed for independent contractors.

What Is a 1099 Income Mortgage Loan?

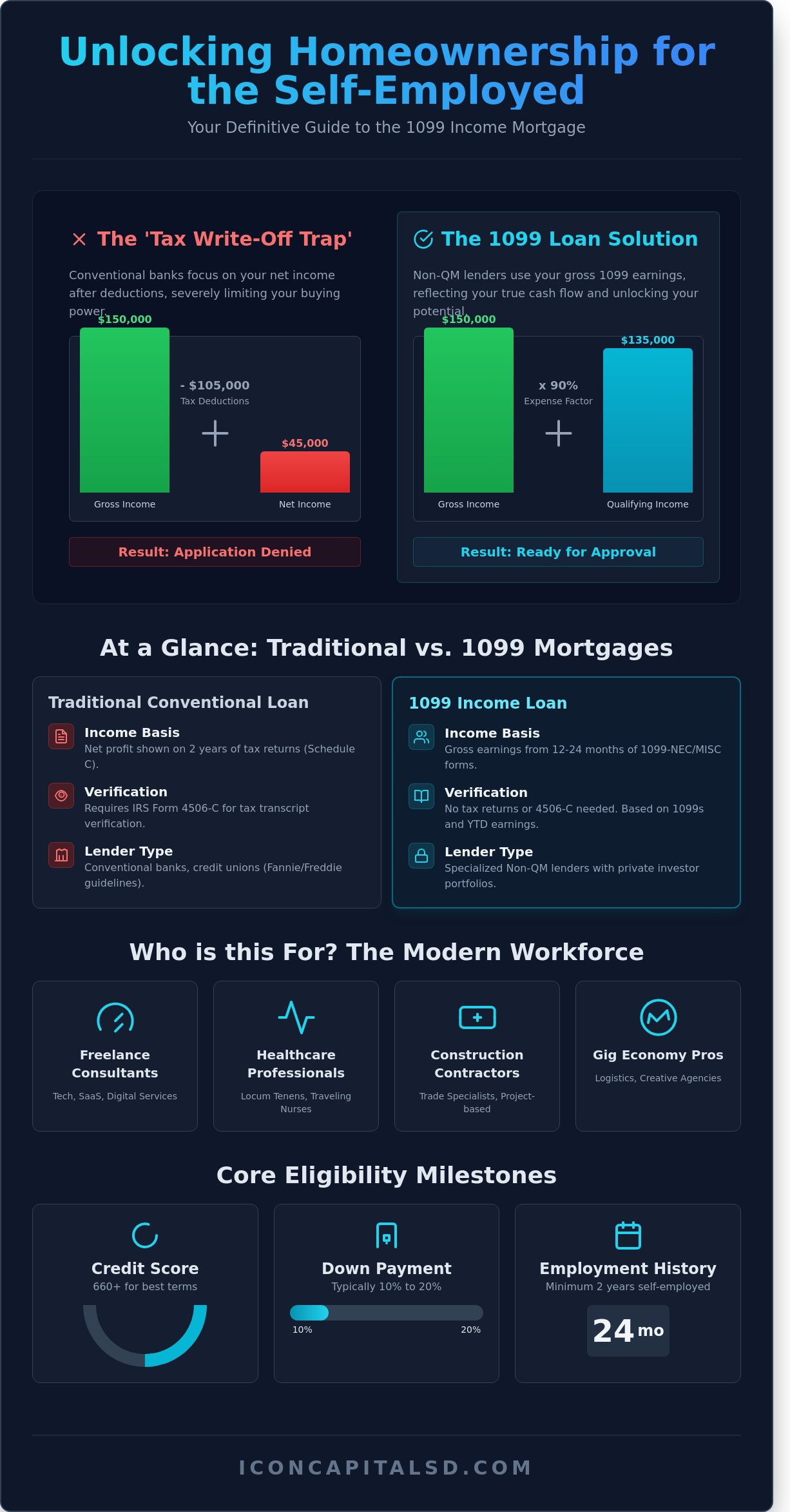

A 1099 income mortgage loan is a specialized Non-QM (Non-Qualified Mortgage) product designed for the 51% of the US workforce expected to engage in independent work by 2027. Unlike traditional conventional loans that rely on net taxable income, this program evaluates gross earnings reported on IRS Form 1099. Standard lenders typically require two years of tax returns and focus on the bottom line of a Schedule C. This approach penalizes successful entrepreneurs who use legal tax strategies to reduce their liability. If you’re ready to see how your gross earnings translate to buying power, you can request a quote to view current rates.

The primary shift occurs in the evaluation process. How 1099 Mortgages Work: The Underwriting Difference involves using a set percentage of the 1099 gross income, often 90% for service-based businesses, to determine Debt-to-Income (DTI) ratios. This bypasses the heavy depreciation and business expenses that usually disqualify self-employed applicants at big-box banks. By focusing on the 1099-NEC or 1099-MISC forms, underwriters provide a more accurate reflection of a borrower’s actual cash flow and ability to repay the debt.

The ‘Tax Write-off Trap’ for Self-Employed Borrowers

Traditional underwriting standards were built for W-2 employees with fixed salaries. For a contractor earning $180,000 gross but claiming $70,000 in legitimate business expenses, a standard bank sees only $110,000 in qualifying income. In the 2026 economy, this tax write-off trap prevents high-earners from accessing competitive leverage. The 1099 income mortgage loan decouples your tax strategy from your borrowing capacity. You can maximize your deductions to lower your tax bill without sacrificing your ability to secure a primary residence or investment property.

Who Qualifies as a 1099 Earner in 2026?

Eligibility focuses on individuals who receive 1099 forms as their primary source of compensation. This includes a broad range of modern professionals:

- Freelance consultants and technology developers in the software-as-a-service sector.

- Healthcare professionals, specifically locum tenens physicians and specialized traveling nurses.

- Construction contractors and trade specialists working on a per-project basis with multiple developers.

- Gig economy professionals in high-demand logistics, creative agencies, or specialized digital services.

Most programs require a minimum of 12 to 24 months of history as a 1099 earner in the same industry to establish stability. This ensures the borrower has a consistent track record of generating income outside of a traditional employer-employee relationship.

How 1099 Mortgages Work: The Underwriting Difference

Underwriting for a 1099 income mortgage loan differs significantly from standard W-2 processing. Traditional lenders focus on net taxable income after business deductions. This often disqualifies self-employed borrowers who utilize legal write-offs to reduce their tax liability. Non-QM underwriters prioritize gross earnings instead, allowing for a higher debt-to-income (DTI) capacity.

Calculating Your Qualifying Income

Lenders typically average your total 1099 earnings over a 24-month period. If your 2024 earnings were $120,000 and 2025 reached $140,000, the lender calculates a monthly average of $10,833. If income declines by more than 10% year-over-year, underwriters usually default to the lower, most recent figure to mitigate risk. Lenders apply a flat expense factor to your gross earnings to calculate qualifying income, effectively bypassing the need for tax returns and complex schedule C deductions. Understanding What Is a 1099 Income Mortgage Loan? helps clarify why these specific documentation requirements exist for independent contractors.

Non-QM vs. Traditional Qualified Mortgages

Non-QM products don’t follow Fannie Mae or Freddie Mac guidelines. Private investors hold these loans in their own portfolios, which grants them the authority to set flexible income verification standards. You won’t need to provide tax transcripts or 4506-C forms. In exchange for this flexibility, expect interest rates approximately 0.75% to 1.5% higher than conventional prime rates. Most 1099 programs require a minimum down payment of 10% to 20%, resulting in a maximum 80% to 90% loan-to-value (LTV) ratio.

Documentation and Property Types

You’ll need your 1099 forms from the last two years and a year-to-date (YTD) earnings statement to prove income stability. While some programs accept scores as low as 620, securing the most competitive terms requires a credit score of 660 or higher. These loans apply to primary residences, second homes, and investment properties. If you’re ready to see how your specific earnings translate into a loan amount, you can request a quote to get precise figures for your scenario.

1099 Loans vs. Bank Statement Loans: Which Is Right for You?

Documentation defines the deal. A 1099 income mortgage loan simplifies the process by focusing on gross earnings rather than net profit after deductions. Lenders typically require the most recent one or two years of 1099 forms to calculate qualifying income. In contrast, bank statement loans require 12 or 24 months of complete personal or business records to track cash flow. The choice depends entirely on how you receive payments.

1099 programs are the primary choice for consultants, software engineers, or medical contractors who have one or two steady clients. If your income is concentrated in a few large annual forms, the 1099 route is faster. Business owners with high transaction volumes, such as e-commerce sellers or restaurant owners, usually find bank statement loans more effective. These programs capture the daily liquidity that a single tax form cannot reflect.

The expense ratio is the deciding factor for many borrowers. 1099 loans often apply a standardized expense factor, typically ranging from 10% to 25%. This provides significantly higher leverage than a P&L loan if your actual business overhead exceeds 50%. By using a lower default expense ratio, lenders can qualify you for a higher loan amount based on a larger portion of your gross 1099 earnings.

Choosing Based on Your Business Structure

Solo-preneurs with minimal overhead benefit most from 1099 verification. This structure keeps the process transactional and avoids the scrutiny of line-item business expenses. If your business employs a staff of 10 or maintains a high-cost physical office, bank statement or P&L loans are necessary to prove stability. Request a quote to see which program fits your specific income structure and maximizes your purchasing power.

Interest Rates and Down Payment Expectations

Non-QM lenders price a 1099 income mortgage loan with a risk premium because these files don’t meet secondary market standards. Expect interest rates to sit 0.75% to 1.5% higher than traditional GSE products. Lenders often require a 10% to 20% down payment to offset this risk. You can lower your rate by maintaining a FICO score above 720 or increasing your equity position. Most borrowers treat these loans as a two-year bridge. They secure the property now and refinance into a conventional product once their tax returns are adjusted to show higher net income.

Self-Employed Mortgage Requirements for 1099 Earners

Securing a 1099 income mortgage loan requires a methodical approach to financial verification. Unlike traditional Fannie Mae or Freddie Mac loans, these programs focus on gross earnings reflected on your tax forms rather than net taxable income after deductions. It’s essential to follow these five steps to prepare your application for a successful close.

- Step 1: Confirm 24 months of continuous self-employment in your current industry. Lenders look for stability in your professional field.

- Step 2: Aggregate all 1099-MISC and 1099-NEC forms for the 2024 and 2025 tax years to establish an average monthly income.

- Step 3: Generate a year-to-date (YTD) profit and loss statement that covers the period from January 1st to the current month-end. This doesn’t always need to be audited by a CPA but must be accurate.

- Step 4: Conduct a credit audit to identify high revolving debt. Reducing credit card balances below 25% utilization improves your Debt-to-Income (DTI) ratio and overall qualification.

- Step 5: Document your down payment. Funds must be seasoned in a personal or business account for at least 60 days to satisfy anti-money laundering requirements.

The Two-Year Rule: Exceptions and Nuance

Standard guidelines usually require two years of self-employment, but exceptions exist for experienced professionals. If you transitioned from a W-2 role to a 1099 contractor within the last 12 months, you can qualify if the work remains in the same specific field. Lenders scrutinize gaps in earnings; any hiatus longer than 45 days will require a detailed explanation. Continuity of income for Non-QM underwriting is the formal determination that a borrower’s self-employment earnings are stable and likely to continue for at least 36 months.

Documentation Checklist for a Smooth Approval

Data accuracy prevents delays in the underwriting queue. Ensure your file includes 1099s, a signed 4506-C form for IRS verification, and copies of any required professional licenses. A Letter of Explanation (LOE) is mandatory if your income decreased by 15% or more between 2024 and 2025. Icon Capital simplifies the submission process by utilizing an integrated digital platform. This allows borrowers to upload documents and receive feedback on their 1099 income mortgage loan application within 24 to 48 hours.

Ready to see how your 1099 income translates to buying power? Request a quote from Icon Capital today.

How to Secure Your 1099 Mortgage with Icon Capital

Icon Capital provides creative financing solutions that look beyond the standard tax return. Traditional lenders often disqualify self-employed borrowers because of high business write-offs. We focus on your gross earnings instead. Our 1099 income mortgage loan program is designed for contractors and consultants who need significant leverage without the restrictions of retail banking math.

Speed is a critical factor for real estate investors and busy professionals. Our streamlined underwriting process removes the red tape associated with conventional loans. We offer loan amounts up to $3 million and LTV options reaching 80% for qualified borrowers. Our internal team handles the complexities of non-traditional documentation to ensure a smooth closing.

We simplify the journey through a methodical 4-step process:

- Structure: We analyze your 1099 forms and credit profile to determine the best program fit.

- Submit: You provide the necessary documentation through our secure portal.

- Underwrite: Our specialists review your cash flow and assets with a focus on approval.

- Fund: We move to the closing table, often in as little as 15 days.

Why Experience in Non-QM Matters

Retail banks typically don’t understand 1099 math. They rely on Schedule C net income, which often doesn’t reflect your actual buying power. This leads to 45% of self-employed applicants facing unnecessary denials. Icon Capital specializes in Non-QM products. We structure loans to maximize your leverage and minimize out-of-pocket costs. Request a custom quote for your 1099 loan today to see how we calculate your qualifying income differently.

Beyond 1099: Scaling Your Portfolio

You can use a 1099 income mortgage loan to secure your primary residence while simultaneously using DSCR loans for investment properties. This dual approach allows you to scale your real estate portfolio without the limitations of debt-to-income ratios on every deal. The Icon Capital Advantage provides a clear path for long-term growth by treating you as a business entity rather than just a W-2 employee. Our team is ready to help you navigate the 2026 market with precision. Please give us a call or shoot an email to explore your financing options.

Leverage Your Self-Employed Earnings in 2026

Navigating the 2026 mortgage market as a self-employed professional requires a shift from traditional lending standards. A 1099 income mortgage loan provides the flexibility you need by utilizing your gross 1099 earnings rather than the net income shown after tax deductions. This approach ensures your hard work is reflected in your actual buying power. Icon Capital specializes in these Non-QM products, offering high-leverage options for borrowers who don’t fit the standard bank profile.

Our team focuses on efficiency and tangible results. We offer loan amounts reaching $2 million or more, tailored specifically for the complex financial profiles of modern contractors and freelancers. You won’t deal with the typical red tape found at retail banks. Instead, you’ll benefit from our streamlined 4-step funding process designed to get you to the closing table faster. Whether you’re purchasing a primary residence or expanding an investment portfolio, we have the specialized expertise to structure your deal effectively. Secure your 1099 mortgage quote from Icon Capital today and take the next step toward your property goals. Your business success deserves a financing partner that understands how to value your true income.

Frequently Asked Questions

Can I get a mortgage with only one year of 1099 income?

Yes, you can qualify for a mortgage with 12 months of 1099 history through specific Non-QM programs. While traditional Fannie Mae guidelines usually require a 24-month history, our 1099 income mortgage loan options allow for a shorter track record if you have a 20% down payment. You’ll also need to show 6 months of cash reserves to prove financial stability.

How much higher are 1099 mortgage rates compared to traditional loans?

Expect interest rates for 1099 loans to be 1.5% to 2.5% higher than standard 30-year fixed conforming rates. If the current market rate for a W-2 borrower is 6.5%, a 1099 borrower typically sees rates between 8.0% and 9.0%. This premium covers the manual underwriting and increased risk associated with non-traditional income documentation.

Do I need to provide tax returns for a 1099 income loan?

No, you don’t need to provide full tax returns for this specific program. Lenders qualify you based on the gross amount shown on your 1099 forms from the last 1 or 2 years. We apply a fixed expense factor, usually between 10% and 25%, to calculate your qualifying net income without reviewing your IRS filings or deductions.

What is the minimum credit score for a 1099 mortgage in 2026?

The minimum credit score required for a 1099 mortgage is 620 as of January 2026. Borrowers with scores above 720 access the highest LTV ratios and the most competitive pricing. If your score is below 660, expect to provide a 25% down payment and 12 months of liquid assets to secure an approval.

Can I use 1099 income to buy an investment property?

Yes, you can use 1099 income to purchase 1-4 unit investment properties. While many investors choose DSCR loans, a 1099 income mortgage loan is ideal when your personal earnings are stronger than the property’s projected rental income. These investment deals typically require a minimum 20% down payment and 680 credit score.

How do lenders verify 1099 income if the year isn’t over yet?

Lenders verify current earnings using a Year-to-Date (YTD) profit and loss statement or the last 3 months of bank statements. If you earned $140,000 in 2025 and your 2026 YTD statements show $70,000 through June, the underwriter confirms your income is stable. This process ensures your current trajectory matches the 1099s provided for previous years.

Is a 1099 loan the same as a ‘No Doc’ loan?

No, a 1099 loan isn’t a “No Doc” loan because it requires verified proof of earnings. True “No Doc” loans don’t require any income disclosure, whereas 1099 programs use your 1099 forms and bank records to establish your ability to repay. It’s a “Reduced Doc” solution that bypasses the complexities of tax return analysis.

What down payment is required for a 1099 mortgage?

A 10% down payment is the minimum requirement for borrowers with a credit score of 700 or higher. If your credit score falls between 620 and 699, the required down payment usually increases to 20%. These equity requirements protect the lender and vary based on the total loan amount and your overall credit profile.